Start Here

The newest article is the worst place to start. This is the reading order: eight pillars, over three hundred articles, plus an advanced stream, each walking you out of a specific trap.

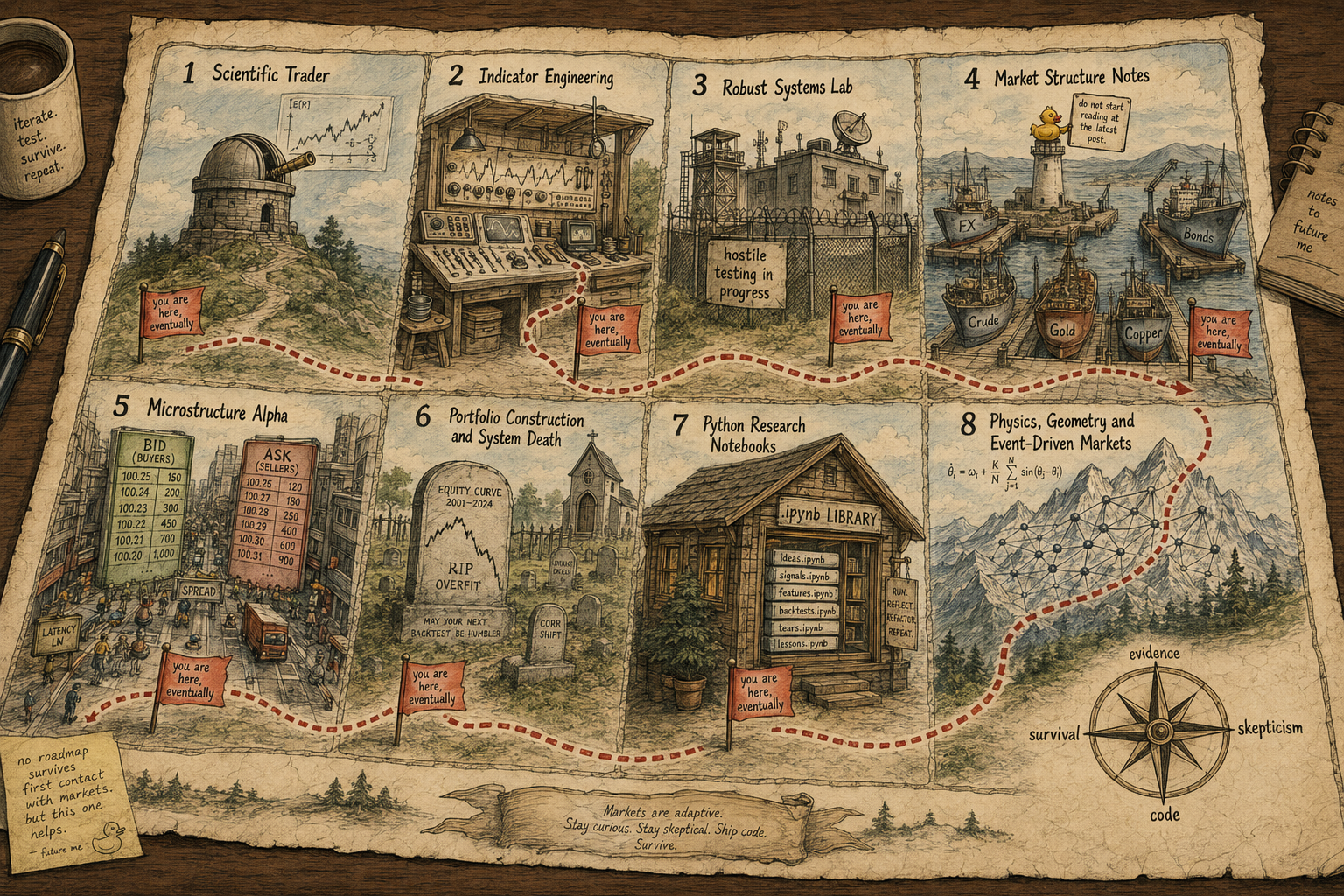

You landed on a site with over three hundred articles and no obvious door. The front page shows whatever I published last, which is the worst place to begin, because the last thing I wrote assumes ten earlier things you have not read. A band-pass filter article in Pillar 2 quietly presupposes the indicator-quality framework three articles before it and the scientific-method framework an entire pillar earlier. Read it cold and you get the formula without the reason the formula matters.

This page is the door. It is the order I would hand you if you walked up and asked where to start.

Think of it as a route, not a library. Eight pillars, over three hundred articles, plus a seventeen-chapter advanced stream at the end. Each pillar takes you in believing one thing and walks you out believing something more useful. Pillar 1 rebuilds how you judge any trading claim. Pillars 2 through 6 are the engineering: how to build a signal, prove it, place it in a market, execute it, and size it without dying. Pillar 7 turns the claims into code you can re-run. Pillar 8 is the frontier, and it assumes you did the work in 1 through 6.

Read each pillar's framing first. It tells you the trap you are walking out of and what you can do once you have. Then work the table top to bottom. The order is the point.

A blank link means the article is written and queued, not missing. The titles are the map whether or not the link is live yet.

Pillar 1 — The Scientific Trader

Start here even if you have traded for years. This is the pillar that changes what you accept as evidence. You walk in treating a good backtest as proof. You walk out knowing that one backtest is a single sample with error bars wide enough to hide a loss, that most apparent edge is just long bias collecting market drift, and that a result means nothing until it beats a null you wrote down in advance. Every rule becomes a hypothesis, every backtest an experiment, every claim something you can falsify. The articles move from why you lose with good ideas, through what a backtest can and cannot tell you, to a full scientific method for building a system. After this pillar you ask sharper questions about every strategy on the rest of the site, including mine.

Pillar 2 — Indicator Engineering

Once you can judge a claim, you need something worth claiming. This pillar is about the input, because the input decides the ceiling: a weak indicator fed to a strong model still predicts nothing. You walk in thinking the model is where the edge lives. You walk out treating indicators as engineered objects with measurable properties, distribution shape, tail behaviour, stationarity, entropy, lag, and frequency response, and you know which of those properties carry the prediction. The pillar takes apart the "throw raw indicators into a model and hope" pipeline and shows where it destroys signal before the model ever sees it. Filters get demystified too: a moving average is an operator with a knowable lag and frequency response, not a magic line. After this pillar you can build a feature that survives the tests from Pillar 1.

Pillar 3 — Robust Systems Lab

You have a feature that looks predictive. This pillar tries to kill it, because a strategy is not robust for surviving one friendly backtest, it is robust for surviving hostile testing. You walk in proud of a smooth equity curve. You walk out able to tell whether that curve is an edge or an artifact of how hard you searched. The articles cover the machinery that exposes false discovery: stationarity, regime coverage, walk-forward, CSCV, Monte Carlo, permutation tests, degrees of freedom, parameter stability, and transaction costs added before you fall in love. The recurring lesson is that most strategies fail because the research process was weak, not because the idea was wrong. The pillar closes with a backtest integrity checklist you run before any strategy gets capital. After this you stop confusing a good search with a good system.

Pillar 4 — Market Structure Notes

A validated signal still has to live somewhere. This pillar is about the market it trades, because the same rule is an edge on one instrument and noise on another, and the difference is structural, not a parameter you can tune. You walk in believing a good system works everywhere. You walk out able to read a market's personality before you deploy: noise versus volatility, the efficiency ratio, trend quality, and the right timeframe. The first half teaches you to match a strategy family to a market's noise level. The second half is cross-asset structure, how bonds, equities, commodities, gold, crude, copper, and the dollar move each other and act as filters. It ends with a hard-edged FX section on why retail execution is a different product from wholesale, and why your broker's routing changes the economics of the exact same signal. After this you stop running one system on everything and calling it robust.

Pillar 5 — Microstructure Alpha

Zoom in to the shortest horizons and prediction stops being separable from execution. This is the order-book layer, and you walk in thinking market making means collecting the spread. You walk out knowing the real job is avoiding adverse selection and quoting around a fair value better than the public mid. The pillar's headline result reframes everything earlier: the same statistically real signal can be worthless as taker flow and valuable as a maker improvement, because the economics flip with who pays the spread. The articles cover fair value, markouts as the truth serum, adverse selection, skew, order-book imbalance, the microprice, and fill probability. After this you understand why a small alpha that fails as a taker can pay as a maker, and why most retail "microstructure" content measures the wrong thing.

Pillar 6 — Portfolio Construction & System Death

You can have a real signal and still lose, because sizing and correlation decide outcomes that the signal never touches. This pillar is where a good rule becomes a survivable business or a slow bleed. You walk in thinking the edge is the hard part. You walk out knowing that the wrong size turns a good signal into a bad strategy, the wrong correlations turn good strategies into a bad portfolio, and a misread drawdown turns a normal losing streak into a panic exit. The articles work through ranking versus forecasting, volatility-adjusted sizing, expectancy, what a drawdown actually diagnoses, and when to switch a system off. A long behavioural section names the failures that keep you attached to a dying system, get-even-itis, taking profits early and losses late, revenge trading. The complexity and econophysics articles at the end explain why fat tails and non-Gaussian dynamics make naive sizing dangerous. After this you treat sizing and portfolio construction as part of the signal, not an afterthought.

Pillar 7 — Python Research Notebooks

Reading about a method is not the same as trusting it. This pillar is where the claims from the other pillars become code you can run yourself. You walk in taking my results on faith. You walk out able to re-run them on your own data and see whether they hold. Each notebook ships with a research question, the data setup, the calculation, the chart, the statistical test, the trading interpretation, and a failure-modes section. These are not tutorials that hold your hand to a pre-baked answer. They are research artifacts built to show whether a claim survives a re-run with different data, which is the only test that matters. Use this pillar to verify anything elsewhere on the site that surprised you, especially if it surprised you in a way you liked.

| # | Notebook |

|---|---|

| 181 | Build an Indicator Quality Report in Python |

| 182 | Build a Threshold Tester for Any Indicator |

| 183 | Permutation Test for Trading Indicators in Python |

| 184 | Monte Carlo Drawdown Simulator for Trading Systems |

| 185 | Optimization Surface Visualizer |

| 186 | MAE/MFE Analyzer in Python |

| 187 | Efficiency Ratio Market Screener |

| 188 | ATR-Normalized Momentum Indicator |

| 189 | Band-Pass Filter Indicator in Python |

| 190 | Dominant Cycle Heatmap with DFT |

| 191 | Order Book Imbalance Backtest |

| 192 | Microprice vs Mid Price: Empirical Test |

| 193 | Crypto Cross-Exchange Lead-Lag Study |

| 194 | Fill Probability Estimator Using Trade Size CDF |

| 195 | Cost-Aware Ranked Long/Short Strategy |

| 196 | Volatility-Regime Filter for Any Strategy |

| 197 | Stationarity Diagnostics for Trading Features |

| 198 | Backtest Integrity Checklist as Code |

| 199 | Portfolio of Systems Simulator |

| 200 | System Decay Detector |

| 249 | Synthetic Prices: EMA of Random Numbers as a Market Model |

| 309 | Dynamic Time Warping for Time-Series Alignment |

| 330 | Rust Data Server, Python Brain |

Pillar 8 — Physics, Geometry & Event-Driven Markets

The frontier, and the one pillar you should not read first. It studies markets as evolving, event-driven, nonlinear systems instead of fixed-time price series. You walk in thinking clock time is the natural axis. You walk out seeing why it is the wrong one: events arrive in bursts, volatility clusters, and a liquidity shock can rewire the correlation structure inside a single afternoon. The chapters move through intrinsic time, a taxonomy of event-driven filters, market geometry, network causality, topological turbulence indicators, optimal-transport regime detection, and the physics of phase transitions in crowded markets. Every chapter assumes you already think the way Pillars 1 through 6 taught you. Read it without that foundation and the terminology will feel like understanding when it is only vocabulary. That is the most expensive way to spend a weekend here.

Part I — Foundations

| Ch | Chapter |

|---|---|

| 1 | Intrinsic Time and the Case for Physics in Markets |

| 2 | Mathematical Toolkit: Stochastic Processes, Hilbert Transform, Phase-Space, Optimal Transport |

Part II — Event-Driven Filters (the 19-family taxonomy)

| Ch | Chapter |

|---|---|

| 3 | Change and Threshold Detection: CUSUM, BOCPD, Directional Change, CDaR |

| 4 | Path Geometry and Bar Anatomy: Swings, Pivots, Range Estimators, Matrix Profiles |

| 5 | Volatility, Jumps, Clustering: Lee-Mykland, BNS, GARCH States, Hawkes |

| 6 | Trend, Memory, Spectrum: Variance Ratio, Hurst, ARFIMA, Wavelets, EMD |

| 7 | Multi-Series, Regimes, Schedules: HMM, Cointegration, Kalman Pairs, Event Studies |

Part III — Market Geometry

| Ch | Chapter |

|---|---|

| 8 | Correlation Done Right: Marchenko-Pastur, RMT, MST, PMFG |

| 9 | Network Causality: Granger Networks, Transfer Entropy, Contagion Density |

| 10 | Riemannian Geometry of Markets: Ollivier-Ricci, Forman-Ricci, Ricci Flow as Regime Speed |

| 11 | Topological Data Analysis: Persistent Homology, Betti Dynamics, TDA Turbulence Index |

| 12 | Optimal Transport and Distributional Regimes: Wasserstein, MF-DCCA |

Part IV — Physics of Market Dynamics

| Ch | Chapter |

|---|---|

| 13 | Coupled Oscillators and Phase Synchronization: Kuramoto, Wavelet Coherence |

| 14 | Information and Thermodynamics: NMI, Permutation Entropy, Market Temperature, Tsallis |

| 15 | Chaos and Nonlinear Dynamics: Lyapunov, Recurrence Quantification, MF-DFA |

| 16 | Many-Body Markets: Ising/Spin-Glass, Magnetization, Sornette LPPL Crash Precursors |

Part V — Systematic Trading Synthesis

| Ch | Chapter |

|---|---|

| 17 | Filter Stacking, ML Pipelines, and Production: Triple-Barrier Labels, Purged CV, Deployment |

Written essays feeding this stream

These standalone essays are already published and feed the chapters above. Read them once you have the foundation; on their own they are vocabulary, not understanding.

Pick your path

You do not have to read all of them in order. Pick the route that matches where you are.

The new-trader path. Read Pillar 1 in order, then Pillar 3 in order, and leave Pillars 4 through 8 alone until both feel obvious. Almost every "I lost money on a system that looked great in backtest" story lives in those two pillars. The lesson is much cheaper here than in a live account, which is the whole reason to take it here.

The signal-engineer path. Skim Pillar 1 over two evenings to absorb the standard of evidence, then read Pillar 2 and Pillar 3 in full. Use Pillar 7 to re-run anything that surprised you. Pillars 4 and 6 are the natural next steps once feature quality and validation stop being your bottleneck.

The advanced-research path. Pillar 8 is the destination, but the way in runs through Pillar 3 for validation, Pillar 2 for signal engineering, and the complexity articles at the tail of Pillar 6. Skip those and Pillar 8 becomes an aesthetic exercise you cannot trade.

KEY POINTS

- The most recent article is the worst entry point, because it assumes earlier work you have not read. This page is the order to read in.

- Eight pillars, over three hundred articles, seventeen chapters in the advanced stream. Each pillar walks you out of a specific trap with a specific new ability.

- Pillar 1 changes what you accept as evidence. Pillars 2 through 6 build, validate, place, execute, and size a system. Pillar 7 is reproducible code. Pillar 8 is the frontier.

- If you want to stop losing money on systems that backtested well, read Pillar 1 and Pillar 3 before anything else.

- If you want to ship signals that survive a permutation test, read Pillar 2, then verify your own results in Pillar 7.

- Read Pillar 8 last. Its prerequisites are not optional, and skipping them buys vocabulary, not understanding.

- A blank link means the article is written and queued, not missing. The titles are the map regardless.