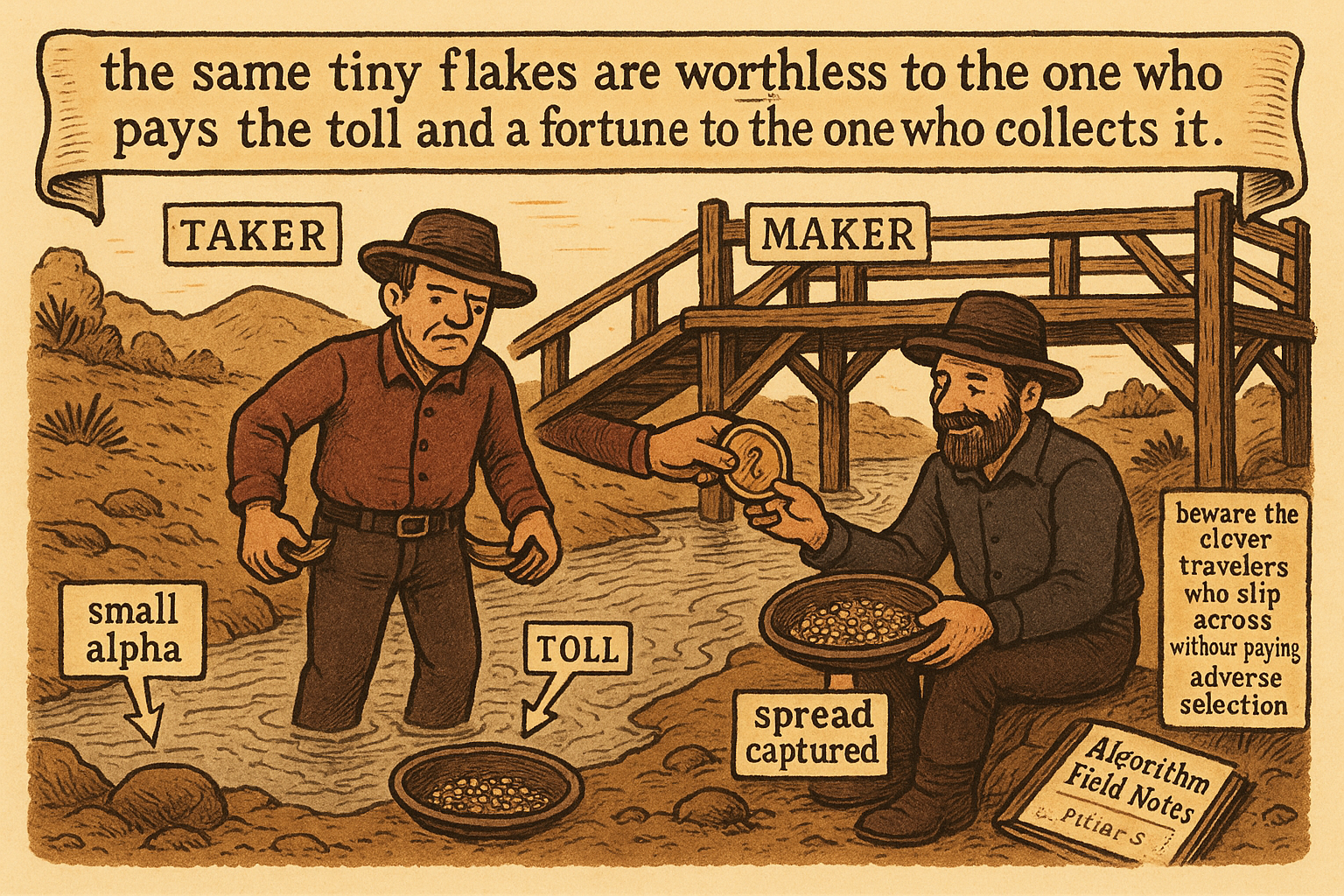

5.18 Why Small Alphas Matter More for Makers Than Takers

A half-bp signal is garbage to a taker who pays the spread and money to a maker who collects it. That cost flip turns thousands of weak alphas into the bulk of a maker's PnL.

A signal that predicts the next move with half a basis point of edge is garbage to a taker. Cross the spread, pay the fees, and the cost swamps the edge before you start. The same signal in the hands of a market maker is money, because the maker is collecting the spread instead of paying it, so the cost that killed the signal for the taker is not just absent, it is reversed into income. The economics of who pays and who earns the spread is the whole reason small alphas matter far more on the maker side.

This article works the cost arithmetic that "Adverse Selection Explained for Traders" leaned on when it said a maker does not need to predict big moves. It sets up "Maker vs Taker Edge: Same Signal, Different Economics", which runs the same signal through both desks.

The cost wall a taker faces

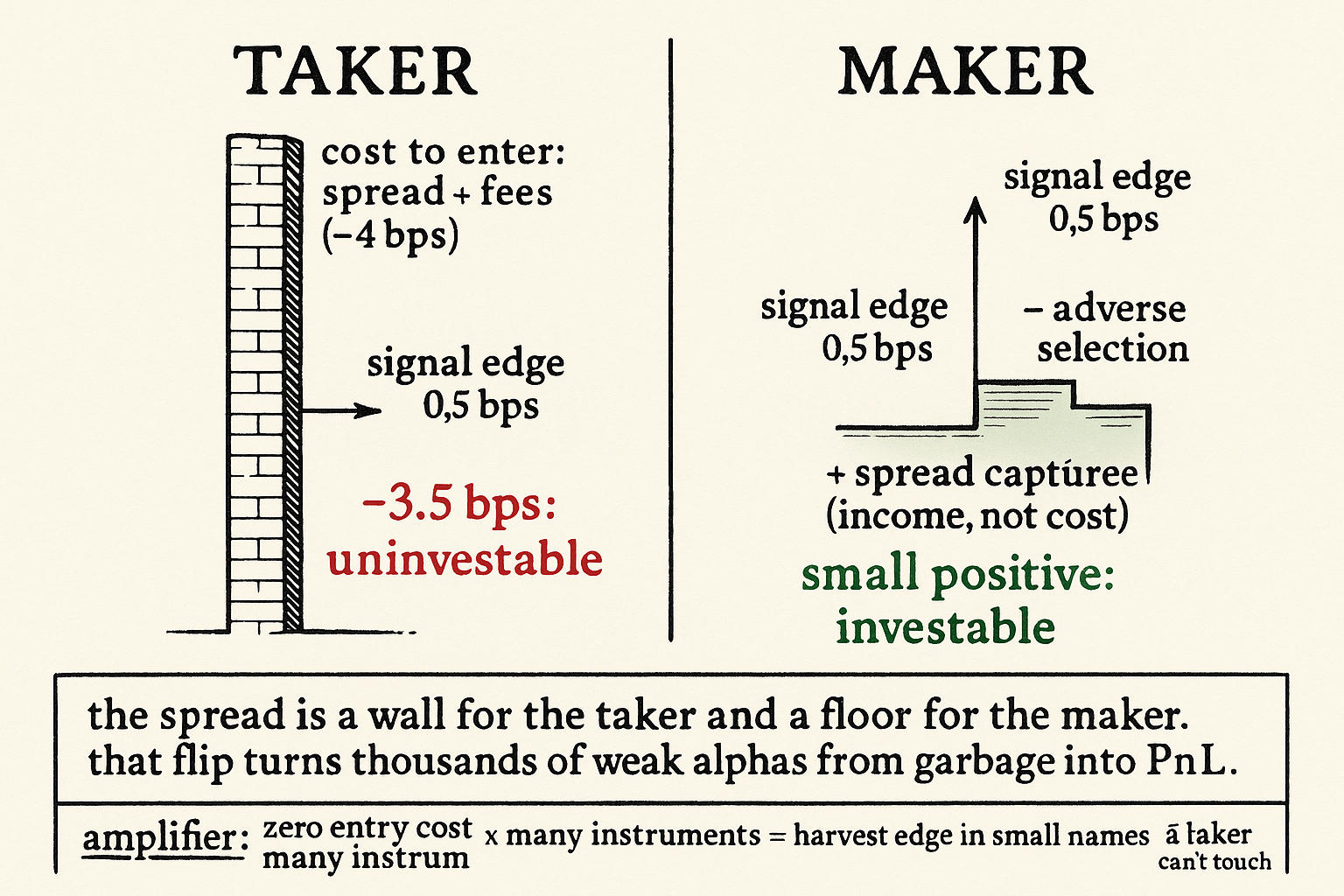

A taker pays to enter every position: the spread crossed plus the fee. For the trade to make money, the predicted edge must clear that wall.

$$ \text{net edge}_{\text{taker}} = \text{signal edge} - \text{spread} - \text{fee} $$

The taker's net edge is the raw signal edge minus the spread minus the fee. If the signal predicts 0.5 bps and the round-trip cost is 4 bps, the net is negative 3.5 bps, a guaranteed loser no matter how often the signal is right. The signal has to clear several basis points of cost just to break even, which throws out the entire population of weak, high-frequency edges, the small structural tilts that predict the next move by a sliver. For a taker, those are uninvestable.

The maker earns what the taker pays

The maker expresses a view by posting passive quotes, so the maker is on the other side of that cost. Instead of paying the spread, the maker collects it on each fill. Having zero cost to trade, earning the spread rather than paying it, makes it suddenly easy to find an edge, because the break-even bar drops to the floor.

$$ \text{net edge}_{\text{maker}} = \text{signal edge} + \text{spread captured} - \text{adverse selection cost} $$

The maker's net edge is the signal edge plus the spread captured minus the adverse-selection cost from the fills the informed pick off. The spread term flipped sign relative to the taker: what was a cost is now income. A 0.5 bps signal that was hopeless for a taker becomes, for a maker, a small tilt layered on top of spread capture, and the only real cost left is adverse selection, which the signal itself helps reduce by shading quotes away from the informed side. The signal does not have to clear a cost wall, it only has to beat the adverse selection it offsets.

Why this expands the investable universe

The consequence is that the maker's universe of usable signals is enormous compared to the taker's. Every weak edge that predicts the next move by a fraction of a basis point, uninvestable for anyone who pays the spread, is investable for the maker. This is why the large desks run thousands of small alphas rather than a few strong ones. None of them would survive transaction costs as a standalone taker strategy. Skewed into passive quotes and ensembled, they stack into the bulk of a market making book's PnL, the positional market making from "Market Making Is Not Just Collecting the Spread".

The amplifier is universe size. With zero cost to trade, expanding the set of instruments you quote makes the same alphas perform better, because the smaller and less efficient names carry more edge per signal, and you can afford to harvest edge there that a taker paying spreads on illiquid books never could. Small alphas times many instruments times zero entry cost is the maker's structural advantage.

The catch: adverse selection is the real cost

The maker's break-even bar is low, not zero, and the thing that fills the gap is adverse selection from "Toxic Flow vs Inventory Risk". The spread is not free income, it is payment for providing liquidity, and the informed traders who pick off your quotes are the cost of earning it. A small alpha pays for a maker only when its edge plus the spread it captures exceeds the adverse selection on those fills. So the maker is not escaping cost, the maker is trading the taker's explicit spread-and-fee cost for an implicit adverse-selection cost, and the small alphas are valuable precisely because they reduce that implicit cost while the spread capture covers the rest. Get the adverse-selection defense wrong and the thousands of small alphas bleed through the same hole.

Visualizing the cost flip

KEY POINTS

- A weak signal worth half a basis point is garbage to a taker, who pays the spread and fees on entry, but money to a maker, who collects the spread instead of paying it.

- The taker's net edge is signal minus spread minus fee. A 0.5 bps signal against a 4 bps cost is a guaranteed loser, so the whole population of weak high-frequency edges is uninvestable for takers.

- The maker's net edge is signal plus spread captured minus adverse selection. The spread term flips from cost to income, so the break-even bar drops to the floor.

- A signal that was hopeless for a taker becomes a small tilt on top of spread capture for a maker, and it only has to beat the adverse selection it offsets, not clear a cost wall.

- This is why desks run thousands of small alphas: none survive transaction costs as standalone taker strategies, but skewed into passive quotes and ensembled they stack into the bulk of the book's PnL.

- Universe size amplifies it: with zero entry cost, expanding the instruments you quote makes the same alphas perform better because smaller, less efficient names carry more edge.

- The catch: the maker trades explicit spread-and-fee cost for implicit adverse-selection cost. Small alphas pay only when edge plus spread beats adverse selection, so getting the defense wrong bleeds all of them.

References

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Optimal High-Frequency Trading in a Pro-Rata Microstructure with Predictive Information

- Liquidity Provision, Adverse Selection, and Competition

- Full article: Deep limit order book forecasting: a microstructural guide

- HFT, Price Improvement, Adverse Selection: An Expensive Way to

- Cross-Market Alpha: Testing Short-Term Trading Factors in the U.S.

- Market-making with Search and Information Frictions - NBER

- Deep Limit Order Book Forecasting A microstructural guide - arXiv

- Insider Trading and the Bid-Ask Spread

- Liquidity supply and adverse selection in a pure limit order book market

- Informed traders and limit order markets

- Limit Order Strategic Placement with Adverse Selection Risk and the Role of Latency

- Deep Limit Order Book Forecasting: A microstructural guide

- Axiomatic Market Making

- Navigating the Fill Probability vs. Post-Fill Returns Trade-Off

- The Impact of Market Informedness on Market Makers' Profitability: Market making with alpha

- High frequency market making: The role of speed

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.