5.1 Market Making Is Not Just Collecting the Spread

Posting a bid and ask is the easy part. The money comes from forecasting fair value, dodging informed flow, and skewing thousands of weak alphas into passive quotes at zero cost.

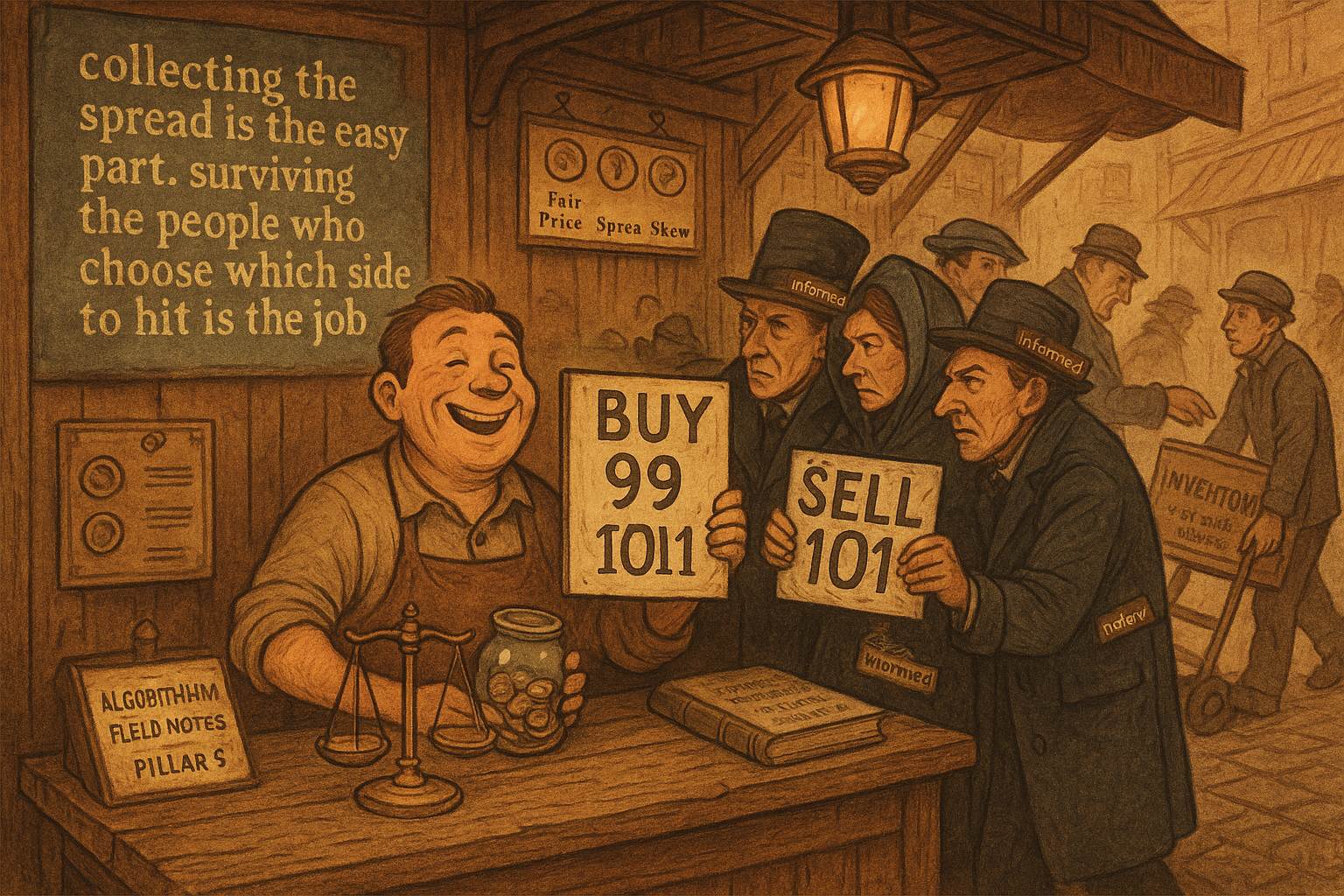

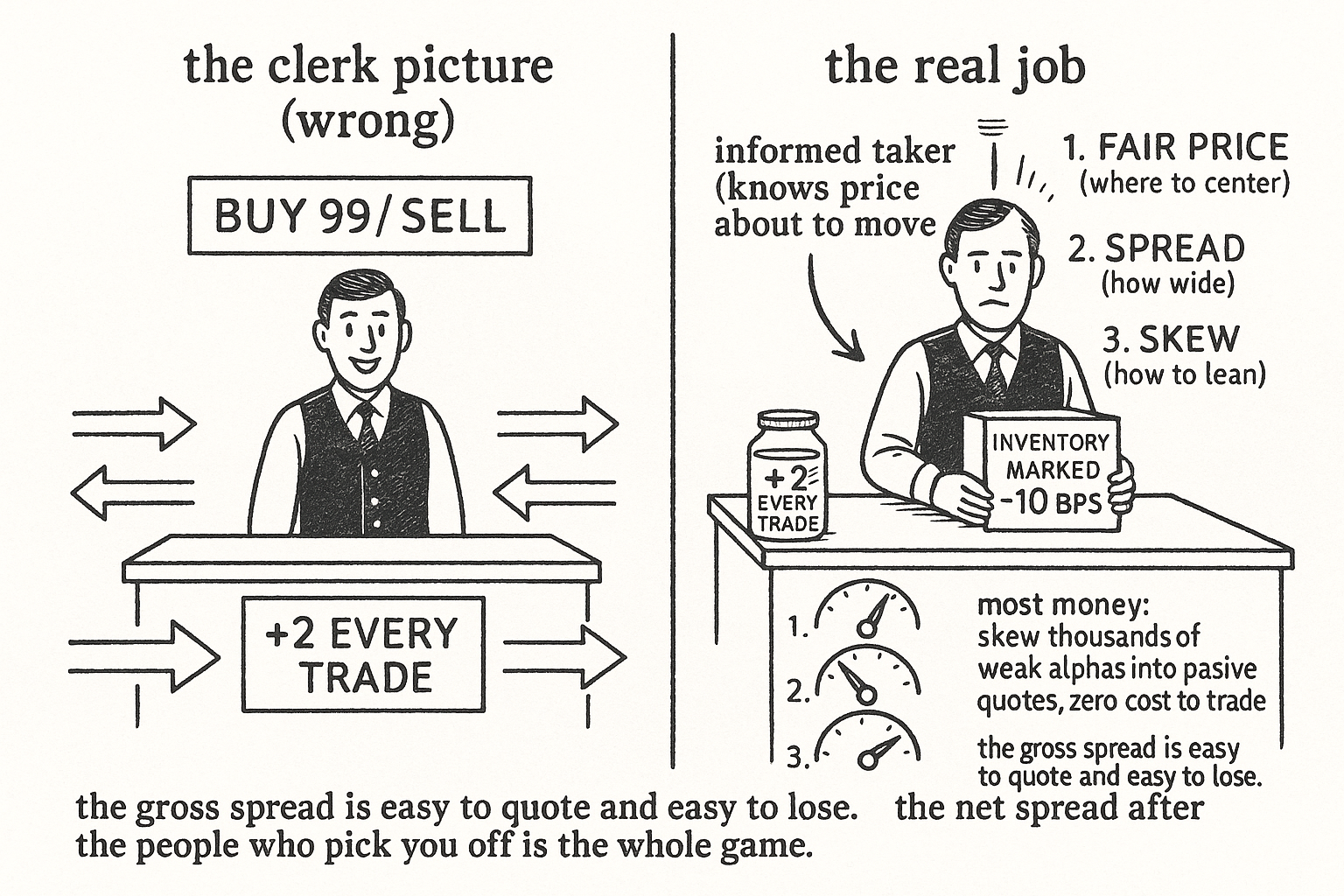

The picture most retail traders carry of a market maker is a patient clerk who posts a bid and an ask, sells to whoever crosses the spread, buys from whoever hits the bid, and pockets the difference forever. Quote 99 bid, 101 ask, collect two dollars per round trip, repeat a million times. That picture is wrong in the way that matters, and the gap between it and the real job is where the entire profit-and-loss of a market making desk lives.

The clerk picture assumes the flow is symmetric and dumb. It is neither. The trader who lifts your offer often knows something you do not, and a second later the price has moved through your fill and left you holding inventory at a loss larger than the spread you collected. Posting a two-sided quote is the easy part. Surviving the people who choose which side to hit is the whole game.

This article frames what market making actually is before the later articles in this pillar pull apart its pieces. It sits next to "The Three Pillars of Market Making: Fair Price, Spread, Skew", which names the components, and "Adverse Selection Explained for Traders", which names the enemy.

The spread is a gross number, not a net one

Start with the arithmetic that the clerk picture gets right and then ruins. You quote a bid and an ask around some center price. The full width between them is your gross edge per round trip: buy at the bid, sell at the ask, bank the difference. On a perfectly random walk with uninformed counterparties on both sides, you would earn half the spread per fill and never carry meaningful inventory.

Real flow does not arrive at random. Suppose you quote a 4 bps spread and a fast trader with a genuine forecast lifts your ask right before the price climbs 10 bps. You collected 2 bps of spread on that fill and you are now short into a rising market, marked down 10 bps. One adversely selected fill erased five spreads of honest profit. The gross spread is real; the net spread after the people who pick you off is what you keep, and it can be negative even when the quoted spread looks generous.

What the desk is actually optimizing

A market making book is not collecting a spread. It is running a forecast of the fair price, posting quotes around that forecast, and shading those quotes to avoid the informed and attract the uninformed. Three things drive the whole result, in descending order of how much they matter: where you center your quotes (fair price), how wide you make them (spread), and how you lean them based on the inventory you already carry (skew).

The academic literature inverts this ordering. Most published market making research obsesses over the skewing problem, the inventory-control equations that decide how to lean your quotes. In practice skew is the most trivial of the three. Get the fair price wrong and no amount of clever inventory math saves you, because you are quoting around the wrong number and every fill is a small donation to whoever quoted around the right one.

Most of the money is positional, not micro

There is a second, larger thing the clerk picture misses. A great deal of market making profit is not made on the second-to-second spread capture at all. It is made by treating market making as a delivery mechanism for medium-frequency alphas, what the desks call positional market making.

The mechanism is simple once you see it. When your cost to trade is zero, because you are earning the spread rather than paying it, signals that would never survive transaction costs as a taker suddenly become tradable. A weak ranking signal that predicts tomorrow's returns with a thin edge is worthless if you have to cross the spread to express it. Skew your passive quotes toward that signal and you express the same view while collecting spread instead of paying it. Stack thousands of these weak signals, skew into all of them, and ensemble the result. That stack, not the tick-by-tick spread, is how the large firms generate the bulk of the number.

"Why Small Alphas Matter More for Makers Than Takers" works through the cost arithmetic that makes this possible, and "Maker vs Taker Edge: Same Signal, Different Economics" shows the same signal paying off for a maker and dying for a taker.

Visualizing the difference

KEY POINTS

- The clerk picture (post a bid and ask, collect the difference forever) assumes symmetric, uninformed flow. Real flow is chosen by counterparties, and the one who hits you often knows the price is about to move through your fill.

- The quoted spread is a gross number. One adversely selected fill into a real move can erase several spreads of honest profit, so net spread after pick-offs is what you keep and it can be negative.

- A desk optimizes three things in descending importance: fair price (where to center quotes), spread (how wide), and skew (how to lean given inventory). Academic research over-weights skew, the most trivial of the three.

- Get the fair price wrong and no inventory math saves you; every fill is a donation to whoever quoted around the right number.

- Much of the profit is positional, not micro: market making delivers medium-frequency alphas at zero trading cost, so weak signals that die for a taker become tradable for a maker.

- The large firms run thousands of small alphas, skew passive quotes into all of them, and ensemble the result. That stack, not tick-by-tick spread capture, is the bulk of the number.

References

- The Art of Currency Trading - Brent Donnelly (Amazon)

- High-Frequency Market Making

- Market Simulation under Adverse Selection

- Optimal Quoting under Adverse Selection and Price Reading

- Market Making with Deep Reinforcement Learning from Limit Order Books

- Predicting Adverse Selection in High-Frequency Cryptocurrency Markets

- Deep Limit Order Book Forecasting: A Microstructural Guide

- Order Book Filtration and Directional Signal Extraction at Ultra-High Frequency

- Short-Horizon Excess Returns in Liquid Equities

- High-frequency market making: The role of speed

- Liquidity Provision, Adverse Selection, and Competition: High-Frequency Market Making

- Liquidity supply and adverse selection in a pure limit order book market

- To Make, or to Take, That Is the Question: Impact of LOB Mechanics on Natural Trading Strategies

- Trading Costs on a Limit Order Book Market: Evidence from the Paris Bourse

- The short-term predictability of returns in order book markets: A deep learning perspective

- When AI Trading Agents Compete: Adverse Selection of Meta ... - arXiv

- Causal and Predictive Modeling of Short-Horizon Market Risk ... - arXiv

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.