5.19 Maker vs Taker Edge: Same Signal, Different Economics

One signal, two businesses. The taker pays the spread and needs a strong edge; the maker earns it and thrives on weak ones across a wider universe at higher frequency. The spread divides them.

Take one signal, an RSI-based ranking, a momentum tilt, an order-flow lean, whatever, and hand it to two desks. One trades it as a taker, crossing the spread to enter. One trades it as a maker, posting passive quotes. The signal is identical, the predicted move is identical, and the two desks end up with completely different businesses. The taker needs a strong signal to overcome cost and trades a small universe at low frequency. The maker thrives on weak signals, trades a huge universe at high frequency, and earns the spread the taker pays. Same alpha, opposite economics.

This article runs the comparison that "Why Small Alphas Matter More for Makers Than Takers" set up, by walking a single concrete signal through both roles.

The same signal, two strategies

Start with one alpha: rank a universe of assets by a metric, go long the top decile and short the bottom, the ranked long-short structure. Size by volatility, normalize, rebalance. The taker version crosses the spread to take each position. The maker version posts passive quotes skewed toward the same ranking, leaning the bid down on the names it wants long and the ask up on the names it wants short, so it accumulates the position by being filled rather than by lifting.

The predicted edge per name is the same number in both. What differs is everything that happens around the predicted edge: the cost of entry, the frequency you can run it, and the breadth of the universe you can apply it to.

Cost: the spread is the hinge

The taker pays the spread plus fees on entry, so the signal's edge must clear that cost or the trade loses. The maker collects the spread, so the same edge sits on top of spread income. The entire difference in economics hinges on this sign flip, worked through in the previous article: a cost for one desk, a revenue for the other.

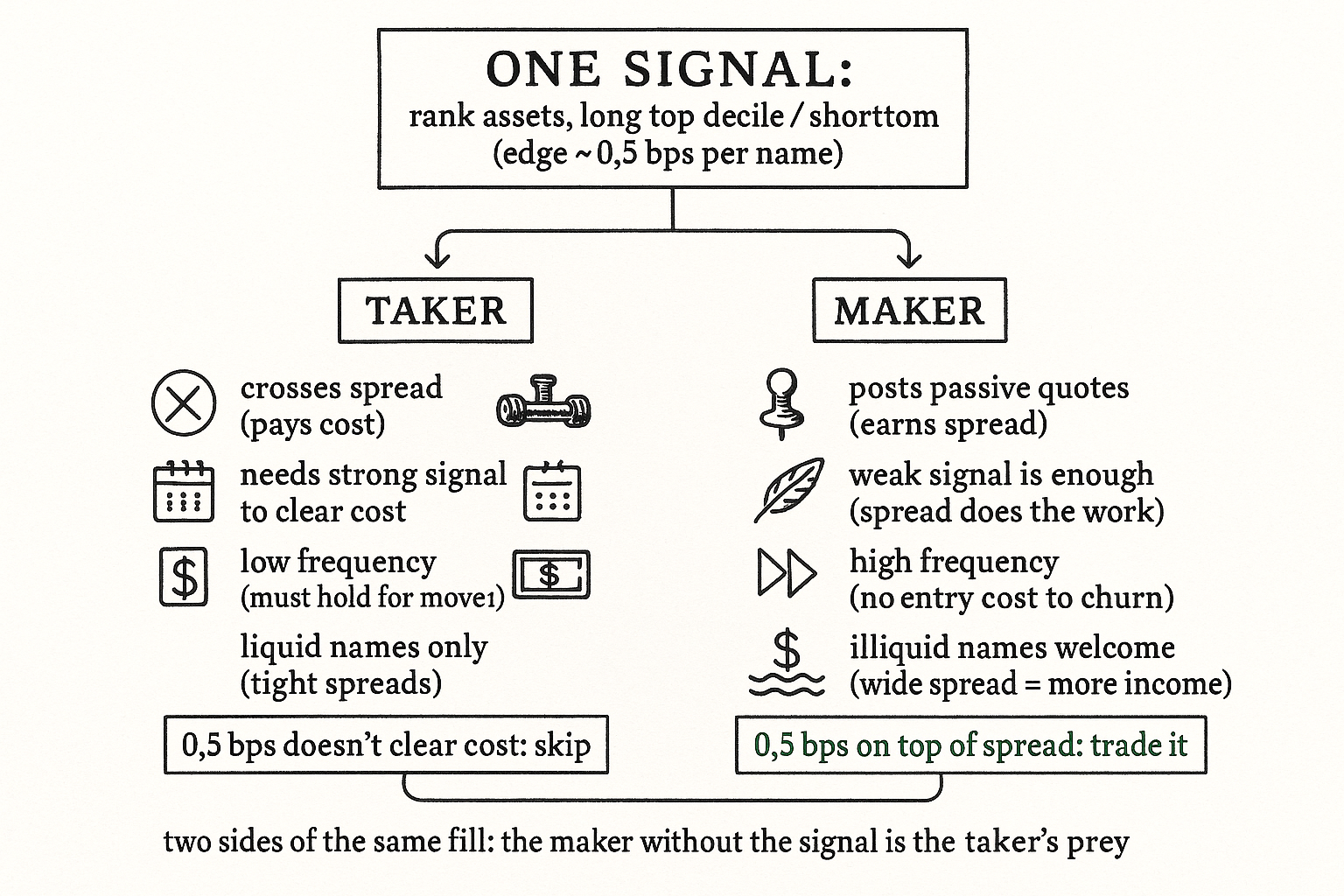

The consequence on strength: a taker needs a strong signal, several basis points of edge, to clear the wall. The maker needs almost nothing, because the spread capture does the heavy lifting and the signal is a small additional tilt. A signal worth 0.5 bps is a taker's loser and a maker's tiny winner, the same 0.5 bps in both calculations.

Frequency and universe

The cost flip cascades into two more differences. Frequency: because each taker round trip pays the spread, the taker must hold long enough for the move to clear the cost, which caps how often it can trade. The maker pays no entry cost, so it can churn at the microstructure frequency, rebalancing on every quote-level update, harvesting tiny moves the taker cannot afford to chase. The maker's natural frequency is far higher because nothing penalizes turnover.

Universe: the taker is pushed toward liquid names where spreads are tight enough to clear, while the maker is pulled toward the illiquid names where spreads are wide, because a wide spread is more income to capture and the smaller, less efficient names carry more edge per signal. The two desks want opposite ends of the liquidity spectrum from the same signal. The maker expanding its universe makes the same alphas perform better, the breadth amplifier from the small-alphas article, while the taker's universe shrinks to where costs are survivable.

They are mirror images, and the maker is the adverse selector's prey

The cleanest way to see the relationship: the maker and taker are two sides of the same fill. When the taker crosses to express the signal, someone makes the other side, and if that someone is a maker without the signal, the maker is being adversely selected, this is the adverse selection from "Adverse Selection Explained for Traders". So the maker does not just want weak signals because they are cheap to trade, the maker needs them to avoid being the uninformed side of the informed taker's trade. A maker running the same signal as the aggressive takers is no longer their prey, it is shading its quotes away from exactly the side they are about to hit.

This closes the loop of the pillar. The maker's edge is not a different kind of alpha from the taker's, it is the same alpha plus the spread, minus the adverse selection, run across a wider universe at higher frequency. Identical signal, mirror-image business, and the spread is the line between them.

Visualizing the two economics

KEY POINTS

- Hand one signal to a taker and a maker and you get two different businesses. The predicted edge is identical; the cost, frequency, and universe around it are opposite.

- Run a ranked long-short the same way: the taker crosses the spread to take positions, the maker posts passive quotes skewed toward the same ranking and accumulates by being filled.

- The spread is the hinge. The taker pays it on entry and needs a strong signal to clear the cost; the maker collects it and needs almost nothing, since spread capture does the heavy lifting.

- A 0.5 bps signal is a taker's loser and a maker's tiny winner, the same number in both calculations.

- Frequency cascades from cost: the taker must hold long enough to clear the spread, capping turnover; the maker pays no entry cost and churns at microstructure frequency.

- Universe diverges too: the taker is pushed to liquid, tight-spread names; the maker is pulled to illiquid, wide-spread names where spread income and per-signal edge are larger.

- Maker and taker are two sides of the same fill. A maker without the signal is the adversely-selected prey of the informed taker, so the maker needs the signal to shade quotes away from the side the taker will hit.

References

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Informed Trading and Maker-Taker Fees in a Low-Latency Limit Order Market

- High-Frequency Trading, Liquidity, and Execution Cost

- High-Frequency Trading, Asset Pricing, and Market Microstructure

- Short-Horizon Excess Returns in Liquid Equities

- Market Making with Deep Reinforcement Learning from Limit Order

- What Happens When Institutional Liquidity Enters Prediction Markets

- The Effect of Maker-Taker Pricing on Market Liquidity in Electronic

- Deep Limit Order Book Forecasting A microstructural guide - arXiv

- Trading Costs on a Limit Order Book Market: Evidence from the Paris Bourse

- Electronic limit order book and order submission choice around price changes

- Liquidity supply and adverse selection in a pure limit order book market

- Optimal Limit Order Execution in a Simple Model for Market Microstructure Dynamics

- The Price Implications of Order Flow Imbalance

- Deep order flow imbalance: Extracting alpha at multiple horizons from the limit order book

- Deep Learning for Short-Term Equity Trend Forecasting - arXiv

- Optimal High-Frequency Trading in a Pro-Rata Microstructure with

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.