About aligrithm

Aligrithm is an independent research publication on systematic trading, quantitative research, market microstructure, and adaptive systems. Long-form essays, code notebooks, and architecture breakdowns across eight pillars, built for traders who care more about how markets behave than about hype.

Aligrithm is an independent research publication on systematic trading, quantitative research, market microstructure, and real-time adaptive systems. The work sits at the intersection of trading, AI, signal processing, statistics, physics, and systems engineering, with a strong empirical bias.

Most trading content online sells predictions, indicators, and short-term excitement. Aligrithm covers what happens after the prediction layer. How real trading systems are researched, tested, engineered, and deployed under live market conditions. How edge survives the journey from notebook to live account, and how often it does not. How a rule that looks great in a backtest becomes a system that holds capital responsibly, then dies in the regime change that comes next, then gets replaced by the next one.

The publication is built for traders, researchers, and engineers who would rather read about a permutation test than a "secret indicator."

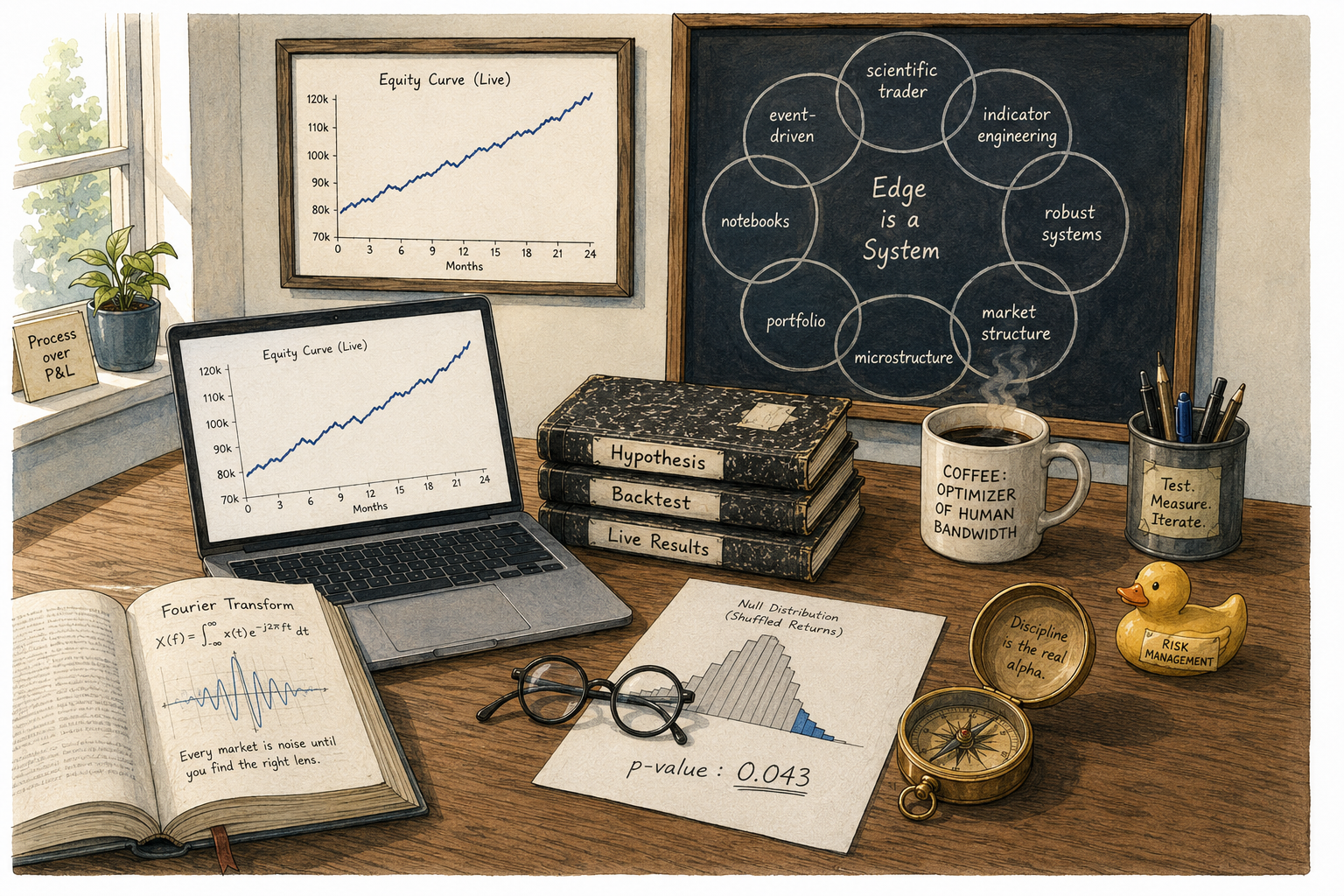

The eight pillars

The content on this site is organized into eight content pillars. Each pillar has its own tag so articles can be filtered, indexed, and cross-referenced.

The Scientific Trader

Evidence-based trading, hypothesis testing, benchmarks, falsifiability, and the scientific method applied to systematic trading. The philosophical and methodological foundation of everything else on the publication. The pillar that teaches the reader to stop asking "does this strategy make money" and start asking "what would prove this strategy wrong."

Indicator Engineering

Signal processing for traders. Entropy, stationarity, smoothing, transformations, frequency response, lag, tail behavior, Range/IQR, sigmoid transforms, band-pass filters, decyclers. Why a clean feature beats a complex model.

Robust Systems Lab

Backtesting realism, walk-forward analysis, Monte Carlo, permutation tests, CSCV, parameter stability, regime coverage, transaction cost modeling, degrees of freedom, the backtest integrity checklist. The anti-overfitting laboratory.

Market Structure Notes

How real markets are organized. FX wholesale versus retail, intermarket relationships, execution mechanics, cross-asset signals, noise versus volatility, market personality, timeframe selection, currency strength decomposition.

Microstructure Alpha

Short-horizon edge that depends on execution. Order book imbalance, microprice, markouts, maker/taker economics, fair value, adverse selection, spread design, skew, fill probability from trade-size CDFs.

Portfolio Construction & System Death

Position sizing, forecast combination, volatility targeting, instrument weighting, drawdown analysis, expectancy, profit factor, MAE/MFE, system decay, behavioral discipline, fat tails, random walk versus efficient markets. The survival layer.

Python Research Notebooks

Reproducible code. Indicator quality reports, threshold testers, permutation tests, Monte Carlo drawdown simulators, optimization surface visualizers, OBI backtests, microprice empirical tests, portfolio simulators, system decay detectors.

Physics, Geometry & Event-Driven Markets

The advanced research frontier. Intrinsic time, event-driven filters, market geometry, network causality, Ricci curvature, topological data analysis, optimal transport, Kuramoto synchronization, Tsallis entropy, Sornette log-periodic power laws. Markets as event-driven, nonlinear, geometric, information-processing systems.

What you will not find on aligrithm

Aligrithm avoids signal services, guru newsletters, secret-strategy vendors, paid trading rooms, chart-pattern alerts, and screenshots of called tops. The publication exists to make rigorous quantitative thinking accessible to readers who are willing to do the work.

About the author

Ali H. Askar is a quantitative systems engineer and AI researcher. He builds production-grade trading systems across FX, crypto, equities, and derivatives markets. His work covers event-driven backtesting, market microstructure, execution systems, AI-driven signal research, and low-latency trading infrastructure, with the emphasis on robustness, realism, and live-market behavior over idealized backtests.

Over the past decade he has developed systematic trading systems, execution engines, arbitrage infrastructure, and quantitative research frameworks designed to operate under real-world market constraints. The opinions on this site come from running those systems, watching them work, watching them decay, and rebuilding them. The writing tries to share that experience without selling anything.