My Portfolio

Portfolio of quantitative trading systems and market infrastructure: graph-based alpha research, event-driven backtesting, low-latency FX arbitrage, financial visualization, trade geometry analytics, and multi-account trade replication. Built for signals that survive real markets.

Research, trading systems, and low-latency market infrastructure.

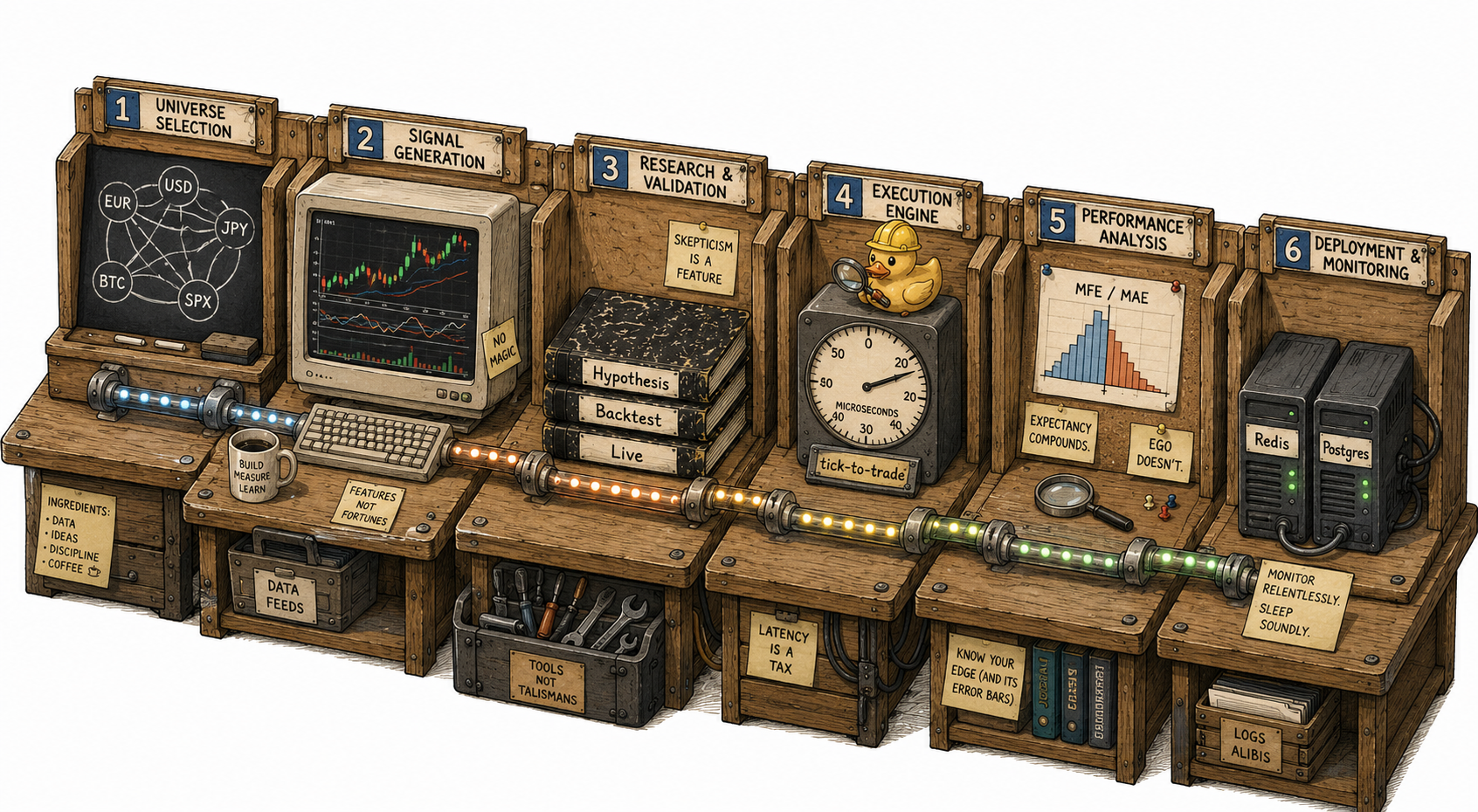

I build quantitative trading systems that sit at the intersection of market microstructure, machine learning, statistical research, and high-performance execution infrastructure. The work covers the full lifecycle: signal research, backtesting, execution, risk, monitoring, and live deployment.

The projects below cover graph-based alpha research, event-driven backtesting, low-latency execution, financial visualization, trade analytics, and multi-account trade management.

DM me for more.

Featured projects

Global Network Momentum Trading Strategy

A production-grade implementation of network momentum, designed to capture momentum spillovers across global assets through graph-based learning. The system treats markets as a dynamic network where information, momentum, and structural relationships propagate across nodes, instead of treating assets as isolated return streams.

The strategy builds adaptive asset networks using convex optimization, propagates signals across those networks with graph signal processing, and generates long/short portfolios via cross-sectional regression. The research pipeline includes walk-forward validation, hyperparameter optimization, parallelized computation, and strict no-lookahead controls.

Area | Implementation |

|---|---|

Network construction | Dynamic asset graphs from cross-asset relationships |

Signal propagation | Graph signal processing over financial networks |

Portfolio generation | Long/short cross-sectional regression |

Validation | Walk-forward testing with no-lookahead bias |

Scalability | Parallelized research and optimization pipeline |

Skills: machine learning, statistical research, quantitative finance, Python. Related pillars: event-driven, robust-systems, scientific-trader, python-notebooks.

PyCharting

A high-performance financial charting library built for fast, interactive visualization of large-scale OHLC datasets. Quantitative researchers need to explore millions of price points, indicators, and trade signals without waiting on slow plotting workflows.

PyCharting uses a FastAPI backend and a lightweight browser-based frontend to stream large financial datasets efficiently. It supports zooming, overlays, multi-panel indicators, trade signal visualization, and real-time interaction. Financial data exploration becomes instant and research-friendly.

Area | Implementation |

|---|---|

Backend | FastAPI data server |

Frontend | Browser-based lightweight charting |

Data support | Large-scale OHLC visualization |

Research tools | Overlays, indicators, signals, multi-panel charts |

Use case | Fast visual inspection of high-frequency financial data |

Skills: Python, FastAPI, financial visualization, research tooling. GitHub: alihaskar/pycharting Related pillars: python-notebooks, robust-systems.

Low-Latency Event-Driven Backtesting & Execution Engine

A high-performance event-driven backtesting and execution engine built around point-in-time correctness, realistic simulation, and production-grade architecture. The engine eliminates lookahead bias by treating every market update, corporate action, order event, fill, and portfolio update as part of a deterministic event stream.

It supports multi-asset strategies, corporate actions as real-time events, advanced order execution modeling, portfolio accounting, OMS/EMS components, and multi-timeframe strategy logic. The same architecture that tests a strategy supports its live deployment.

Area | Implementation |

|---|---|

Backtesting model | Event-driven, point-in-time simulation |

Market data | Multi-asset support with corporate actions as events |

Execution | Advanced order and fill modeling |

Architecture | OMS, EMS, portfolio accounting, strategy layer |

Strategy support | Multi-timeframe logic and scalable research workflows |

Skills: Python, high-frequency trading, backtesting, execution systems. Related pillars: robust-systems, event-driven, market-structure.

HFT FX Arbitrage Engine

A low-latency FX arbitrage system that detects and acts on cross-venue price dislocations across multiple liquidity sources. The architecture is built around hot-path optimization, shared memory, zero-copy data access, lock-free ring buffers, CPU core pinning, and C/Python bindings for deterministic performance.

The system tracks latency across transport, buffer, and processing layers, measuring where every microsecond is spent. It targets high-throughput tick ingestion, real-time state management, and arbitrage detection across 16 venues.

Area | Implementation |

|---|---|

Venue coverage | 16 FX venues |

Data transport | Shared memory and memory-mapped access |

Processing | Lock-free ring buffers, hot-path optimization |

Latency | Sub-20µs tick-to-trade target with full latency tracking |

Throughput | Designed for 200M+ market events per day |

Skills: Python, Rust, C/Python bindings, low-latency systems, FX microstructure. Related pillars: microstructure-alpha, market-structure.

Trade Geometry Signal Analyzer

A quantitative diagnostic engine for understanding what happens after a trading signal fires. Most trading research stops at the entry signal. This project starts where that research ends: how price moves after entry, how quickly it reaches favorable or adverse levels, and how different exit rules behave across regimes.

The system analyzes maximum favorable excursion, maximum adverse excursion, time sequencing, TP/SL probabilities, volatility regimes, and trade archetypes. Exit design becomes data-driven rather than dependent on brute-force parameter optimization.

Area | Implementation |

|---|---|

Trade path analytics | MFE, MAE, time-to-target, path sequencing |

Exit research | Probabilistic TP/SL outcome analysis |

Risk design | Risk/reward frontiers and adverse excursion diagnostics |

Regime analysis | Volatility-based behavior segmentation |

Clustering | Trade archetype discovery |

Skills: quantitative research, Python, risk management, trade analytics. GitHub: alihaskar/signal_analyzer Related pillars: portfolio-system-death, robust-systems, scientific-trader.

MT4/MT5 TradeManager

A distributed trade replication and risk management system that synchronizes trades across multiple master and slave accounts in real time. The system combines WebSocket event ingestion, REST execution, Redis state management, PostgreSQL persistence, reconciliation logic, and real-time monitoring.

Built for production-grade multi-account execution workflows where reliability matters more than cosmetic dashboards. It includes discrepancy detection, risk controls, fault-tolerant execution, account synchronization, and monitoring through Dash and Grafana.

Area | Implementation |

|---|---|

Trade ingestion | WebSocket-based event flow |

Execution | REST-based order routing |

State management | Redis and PostgreSQL |

Reliability | Reconciliation, discrepancy correction, fault tolerance |

Monitoring | Dash GUI and Grafana dashboards |

Skills: Python, Redis, PostgreSQL, WebSockets, MT4/MT5, trade replication. Related pillars: market-structure, robust-systems.

What connects these projects

All of these systems share the same focus. Build trading infrastructure that is fast, realistic, measurable, and production-ready.

Principle | Meaning |

|---|---|

Point-in-time correctness | No hidden lookahead bias, no unrealistic assumptions |

Execution realism | Model trading as it happens in live markets |

Latency awareness | Measure and optimize the full path from data to decision |

Research scalability | Large experiments stay repeatable and parallelizable |

Production discipline | Monitoring, reconciliation, and risk as core system components |

Market structure awareness | Build around how markets behave, not how they look in clean datasets |

Areas of focus

Domain | Focus |

|---|---|

Quantitative research | Alpha discovery, statistical validation, cross-asset modeling |

Market microstructure | Order flow, arbitrage, liquidity, execution behavior |

Machine learning | Feature engineering, graph learning, cross-sectional modeling |

Backtesting infrastructure | Event-driven simulation, PIT correctness, realistic execution |

Low-latency systems | Shared memory, lock-free design, hot-path optimization |

Trading operations | OMS/EMS, reconciliation, monitoring, risk controls |

I build systems for the full lifecycle of quantitative trading: research, validation, execution, monitoring, and scaling. The goal is to build infrastructure where signals survive contact with real markets.