5.6 Adverse Selection Explained for Traders

Quote both sides with no view and informed takers hit whichever side is about to move, leaving you the losing inventory. That is adverse selection, the permanent maker-versus-taker battle.

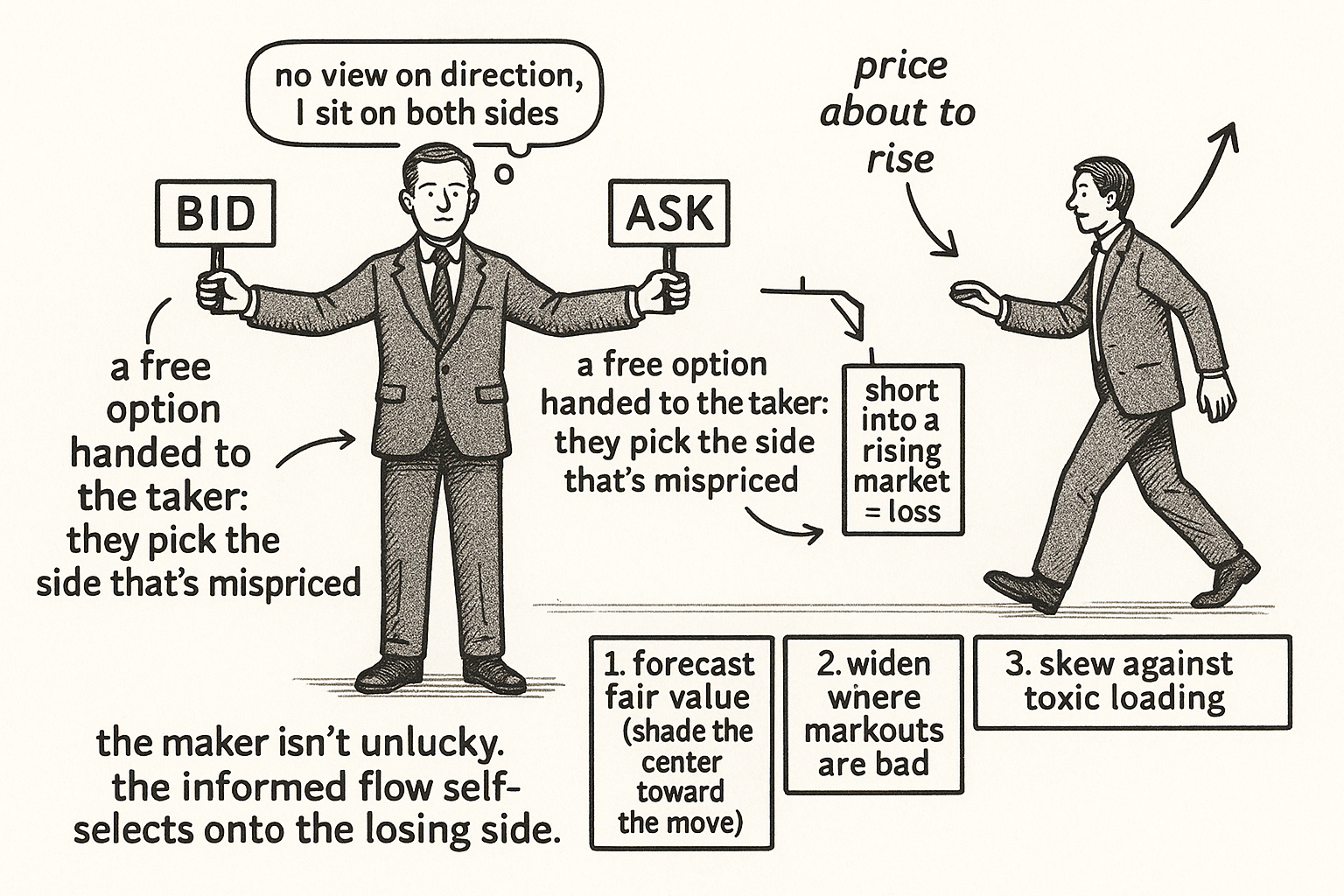

Post a bid and an ask around a price you believe is fair. You have no view on direction, so you sit symmetrically on both sides. Someone with a view does have a direction, and they are usually right, so they hit the side that the market is about to move toward. They lift your offer right before the price climbs, or hit your bid right before it falls, and you are left holding the inventory that loses. That is adverse selection, and it is the permanent battle of maker against taker that decides whether a market making book lives or dies.

This article names the enemy that "Market Making Is Not Just Collecting the Spread" introduced and that "Markouts: The Truth Serum of Market Making" measures. Every defense in this pillar exists to fight it.

Where it comes from

The maker quotes both sides because the maker has no forecast of direction, only an estimate of the current center. The taker who crosses the spread is choosing to pay it, and people do not pay the spread at random. They pay it when they expect the move to more than cover the cost, which means they carry information, or speed, or both, that the maker lacks at the moment of the fill.

So the maker's two-sided quote is an offer to trade in either direction at a fixed center, and the informed counterparty exercises the side that is mispriced relative to the immediate future. The maker is not unlucky. The maker is structurally on the wrong side of the fills that come from informed flow, because the informed flow self-selects onto the losing side. This is why a symmetric quote with no prediction bleeds: it hands the taker a free option to pick the direction.

You do not need to predict big moves

The fix is not to out-forecast the market on large moves. For a maker the bar is much lower, because the maker pays no spread to enter. A signal too weak to be profitable for a taker, who must cross the spread and overcome fees, can be plenty for a maker, who is collecting the spread instead of paying it. A fraction of a basis point of directional edge, worthless to anyone who has to pay to act on it, lets the maker lean quotes away from the side the informed are about to hit.

The relationship is direct: the better you can predict where the market is going, even slightly, the less adverse selection you suffer, because you shade your fair value and your quotes toward the predicted move and the informed trader no longer finds a mispriced side to exercise. "Why Small Alphas Matter More for Makers Than Takers" works through why weak signals are enough on the maker side.

The defenses

Three lines of defense fight adverse selection, each covered in its own article.

Forecast the fair value. Move your center toward where price is heading so the option you are handing the taker is no longer mispriced. The microstructure features do this work: top-of-book imbalance, signed trade flow, short-horizon volatility. "Why Fair Value Is the Core of Market Making" builds the center and "Order Book Imbalance: The First Microstructure Feature to Test" builds the strongest single feature.

Widen where the markouts are bad. Your markout curve marks exactly the conditions, instruments, and sides where adverse selection is eating you, so you widen spreads there and charge the informed more for the option. "Spread Widening During Volatility Expansion" runs this on volatility.

Skew against toxic loading. Lean your quotes so an aggressive informed trader cannot pile a large toxic position onto you at a fixed price. The point of skew is not ordinary inventory management, it is refusing to be loaded up by the informed. "Toxic Flow vs Inventory Risk" makes that distinction the center of its argument.

Visualizing adverse selection

KEY POINTS

- Adverse selection: a maker quotes both sides with no directional view, and informed takers hit whichever side the market is about to move toward, leaving the maker with the inventory that loses.

- People do not pay the spread at random. They pay it when they expect the move to cover the cost, so paid spread carries information or speed the maker lacks at the moment of the fill.

- A symmetric quote with no prediction hands the taker a free option to pick the direction. The maker is structurally on the wrong side of informed fills, not merely unlucky.

- The fix is not out-forecasting large moves. A maker pays no spread to enter, so a signal too weak for a taker is enough to shade quotes away from the informed side.

- The better you predict direction, even slightly, the less adverse selection you suffer, because the informed trader no longer finds a mispriced side to exercise.

- Three defenses: forecast the fair value to remove the mispriced option, widen spreads where markouts are bad, and skew to refuse being loaded with toxic inventory.

- Adverse selection is the permanent maker-versus-taker battle; every microstructure feature and quoting rule in this pillar exists to fight it.

References

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Optimal Quoting under Adverse Selection and Price Reading

- A Pure-Jump Market-Making Model for High-Frequency Trading

- Navigating the Fill Probability vs. Post-Fill Returns Trade-Off

- Order Book Filtration and Directional Signal Extraction at High Frequency

- Deep Limit Order Book Forecasting: A Microstructural Guide

- Timing Equity Quant Positions with Shorter-Horizon Alphas

- Optimal High-Frequency Trading in a Pro-Rata Microstructure with

- Full article: Deep limit order book forecasting: a microstructural guide

- Trading Costs on a Limit Order Book Market: Evidence from the Paris Bourse

- Adverse Selection and Competitive Market Making: Empirical Evidence from a Limit Order Market

- Market-making with Search and Information Frictions

- High-Frequency Market Making: Liquidity Provision, Adverse Selection, and Competition

- High-frequency trading: Definition, implications, and controversies

- Insider Trading and the Bid-Ask Spread: A Critical Evaluation of Adverse Selection in Market Making

- Analysis of Limit Order Book and Order Flow

- Do Informed Investors Time the Horizon? Evidence from Equity Markets

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.