5.3 Why Fair Value Is the Core of Market Making

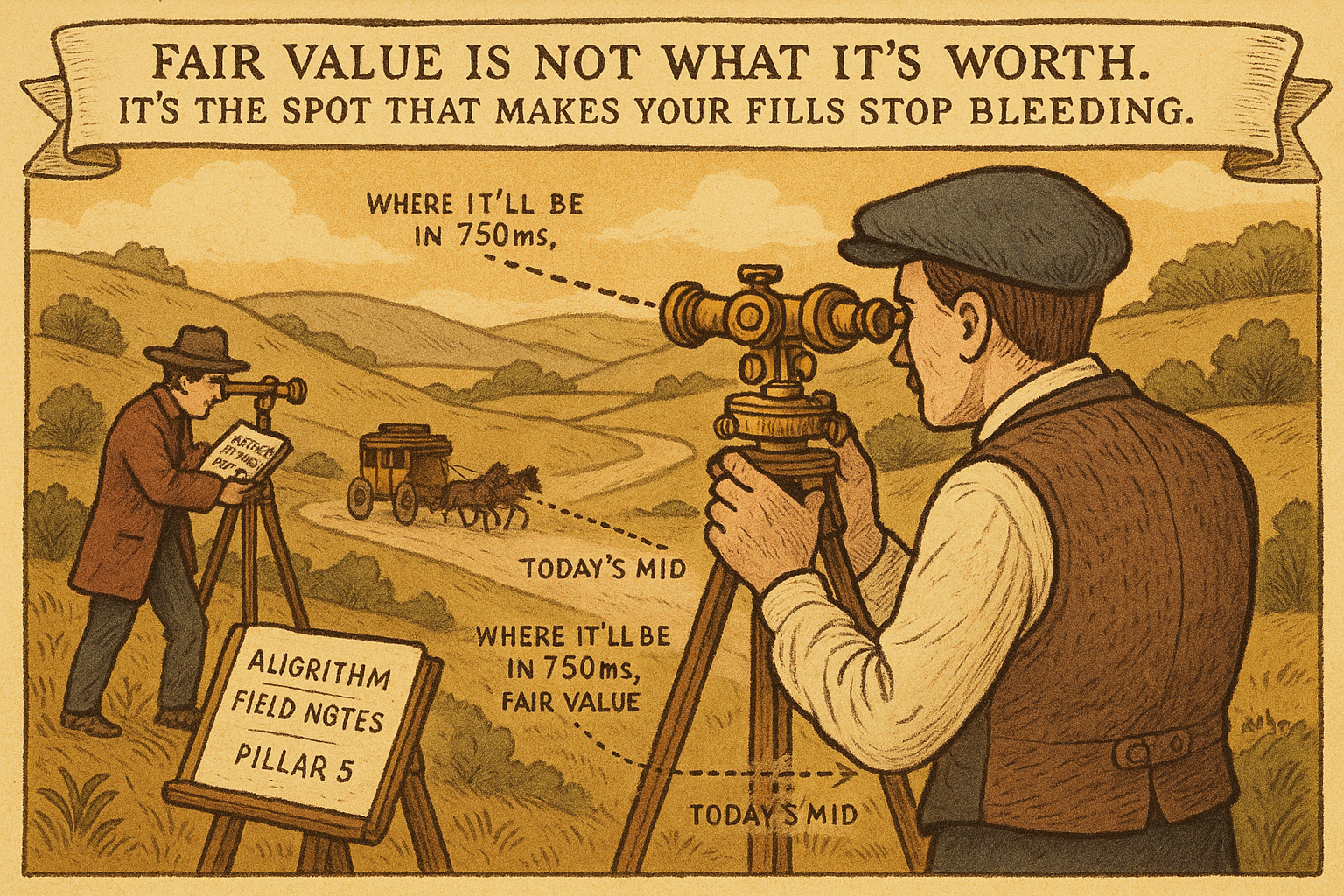

Fair value is the price that gives good markouts when you quote around it. If your losses realize 750 ms after a fill, fair value is where price will be then, not today's mid.

Ask a market maker what fair value is and the honest answer is not philosophical. Fair value is the price that, when you quote around it, gives you good markouts. Nothing about intrinsic worth, nothing about discounted cash flows. A number is fair if your fills around it do not bleed in the seconds after they print. That operational definition is the whole reason fair value sits above spread and skew in importance: it is the only one of the three pillars defined directly by the profit it produces.

The previous article, "The Three Pillars of Market Making: Fair Price, Spread, Skew", ranked fair price first. This one builds it.

Define fair value by markouts, not by belief

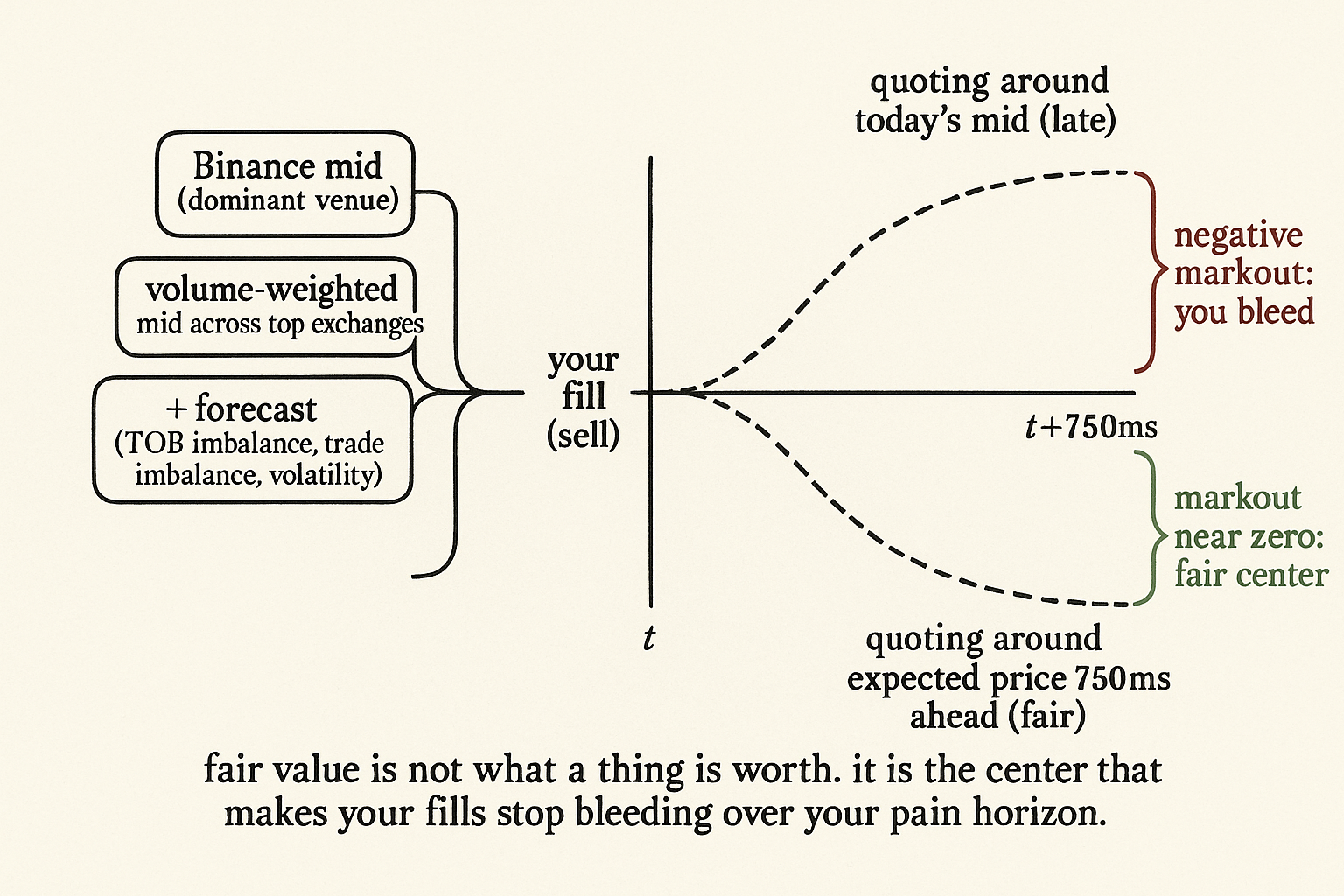

Markout is the change in price after one of your fills, measured at some horizon. Fill a sell, look at the mid price 750 milliseconds later, and the difference is your markout on that trade. Good markouts mean the price did not run away from your fills. Bad markouts mean it did, and you were quoting around the wrong center.

The horizon is where the definition gets sharp. Suppose your losses on adverse fills tend to fully realize about 750 milliseconds after you trade. Then fair value is not today's mid price. It is roughly where you expect the market to be 750 milliseconds from now, because that is the price your fills will be marked against once the dust settles. Quote around the present when your pain horizon is the near future, and you are systematically late.

$$ \text{markout}(\tau) = \text{mid}_{t+\tau} - p_{\text{fill}, t} $$

The markout at horizon tau is the mid price tau later minus the price you filled at. Average it across many fills and a center that produces a markout near zero (after accounting for the side you traded) is a fair center; a center that produces a persistently negative markout is mis-placed, and the size of that negative number is the rate you are bleeding per fill.

A first fair value with no forecast

The simplest workable fair value uses no forecast at all. Take the mid price of Binance, the venue with the dominant share, and quote around it. It costs nothing to compute and it beats quoting around your own small venue's mid by a wide margin.

Improve it one step by replacing a single venue's mid with a volume-weighted mid across the top exchanges, so a thin or stale book on any one venue does not drag your center. A further refinement filters which moves to follow: some moves on other venues are informed and will pull the global fair price, others are noise that will not, and a careful version reacts to the first kind and ignores the second. None of this forecasts the future. It only builds a clean estimate of the present, and that alone is a reasonable starting center.

The contrast that makes the point: quote on a small exchange and assume Bitcoin is worth whatever that exchange's mid says, and you have started from a bad number. The small venue follows the large one with a lag, so its mid is a stale shadow of the real center, and every fast trader who sees the large venue move first picks you off before your stale mid catches up.

Adding a forecast on top

A real edge layers a forecast onto the present estimate. The center becomes the current price plus a prediction of where the price will sit a few hundred milliseconds ahead, so traders with a good short-horizon forecast cannot lift the side you have mis-priced.

Building the forecast is a standard machine-learning problem. Take features that predict the near-future price and fit whatever maps them to a prediction: ridge regression, OLS, gradient boosting. Three simple features start the work. Top-of-book imbalance, the relative size resting on the bid versus the ask, is by far the strongest. Trade-volume imbalance and short-horizon volatility help but need more care to extract signal from. "Order Book Imbalance: The First Microstructure Feature to Test" builds the strongest of these, and "Using Trade Flow to Predict Short-Term Price Movement" builds the trade-based one.

One warning carries over from the forecasting articles in this pillar. The goal is not a forecast with a high R-squared across all moves. It is a forecast that is accurate conditional on the moves where you actually get filled, which is a different and harder target. "Why Forecast Accuracy Is Not Enough in Market Making" handles that distinction.

Visualizing fair value

KEY POINTS

- Fair value is operational, not philosophical: the price that, when you quote around it, gives good markouts. A number is fair if your fills do not bleed in the seconds after they print.

- Markout is the change in price after a fill at some horizon. Average it across fills; a center near zero markout is fair, a persistently negative one is mis-placed and tells you the rate you are bleeding.

- If your adverse losses realize about 750 ms after a fill, fair value is roughly where you expect price to be 750 ms ahead, not today's mid. Quoting around the present when your pain is in the near future leaves you late.

- A first fair value needs no forecast: quote around the dominant venue's mid (Binance for crypto), then upgrade to a volume-weighted mid across top exchanges so a stale single book does not drag the center.

- Treating a small venue's own mid as the value of the asset starts you from a bad number, because the small venue lags the large one and fast traders pick off your stale center.

- A real edge adds a forecast: current price plus a prediction of price a few hundred ms ahead. It is a standard ML problem; top-of-book imbalance is the strongest simple feature, with trade imbalance and volatility behind it.

- The forecast target is accuracy conditional on the moves you get filled on, not a high R-squared across all moves.

References

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Analysis of Limit Order Book and Order Flow

- Mid-Price Prediction in a Limit Order Book

- The Predictive Power of Limit Order Book for Future Volatility, Trade and Order Flow

- Market making under a weakly consistent limit order book model

- Optimal High-Frequency Trading in a Pro-Rata Microstructure with Limit Order Books

- Market Simulation under Adverse Selection

- Short-Horizon Excess Returns in Liquid Equities

- Deep Limit Order Book Forecasting A microstructural guide - arXiv

- High frequency market making: The role of speed

- High-Frequency Market Making Design, Liquidity, and Asset Prices

- Understanding the worst-kept secret of high-frequency trading

- Limit Order Book Shape and Return Distribution

- Deep Limit Order Book Forecasting: A Microstructural Guide

- Predicting Adverse Selection in High-Frequency Cryptocurrency Markets

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.