5.15 Using Trade Flow to Predict Short-Term Price Movement

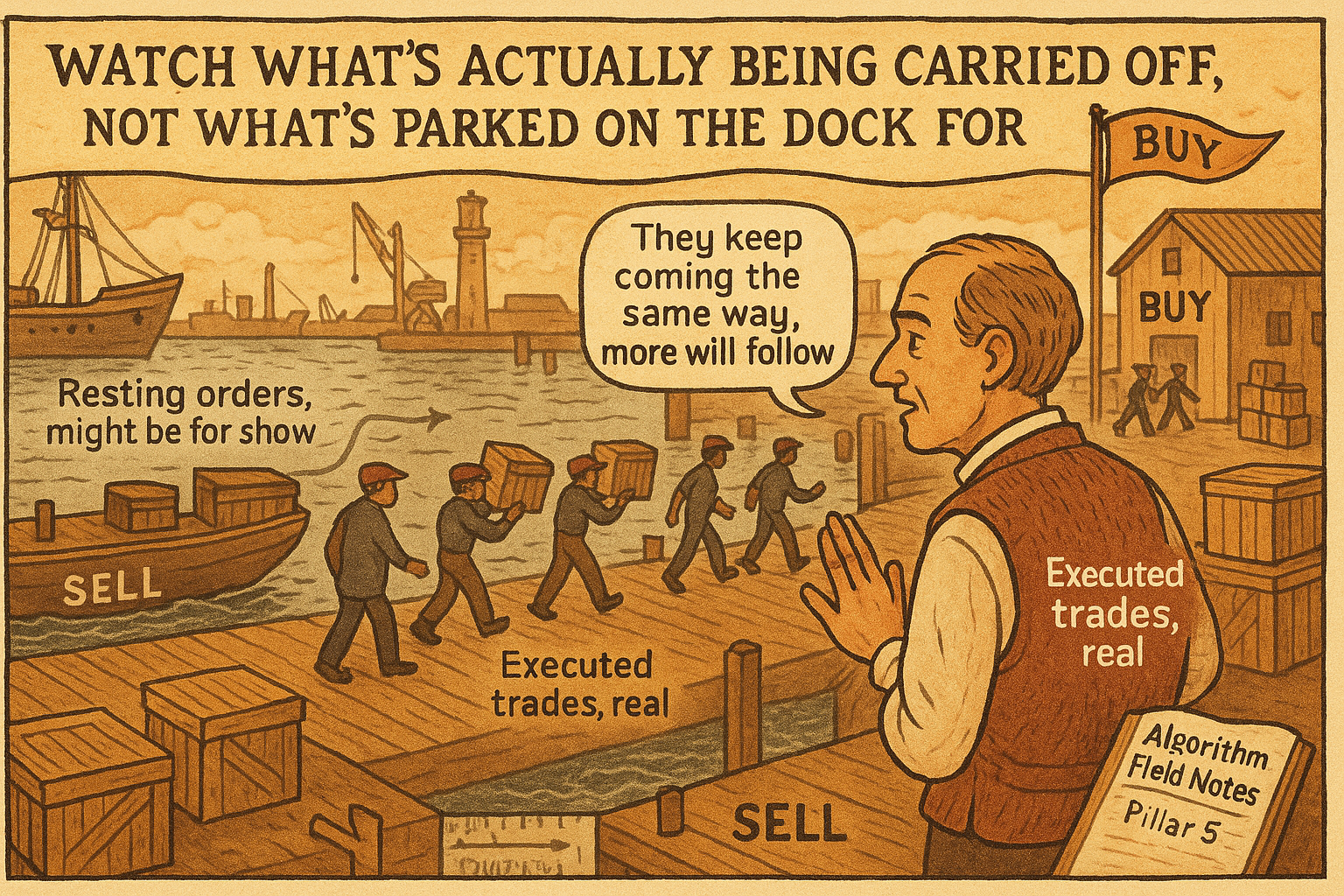

Trade flow reads liquidity being taken, not posted. Signed and summed, it predicts price because trades are autocorrelated: buys follow buys. And unlike book imbalance, executions can't be spoofed.

Order book imbalance reads the resting liquidity, the orders people have posted. Trade flow reads the opposite thing: the liquidity people are taking, the actual executed trades. As a market maker you ultimately do not care where others provide liquidity, you care where people are taking it and how much, because takers are the ones who move the price and the ones who fill your quotes. Signed trade flow is the second microstructure feature to build after imbalance, and it works because trades are autoregressive, which means past trades predict future trades, and future trades predict the price.

This article builds the trade-based forecast that "Why Fair Value Is the Core of Market Making" listed alongside imbalance, and connects it to the skew logic that uses a predicted move.

Sign the flow

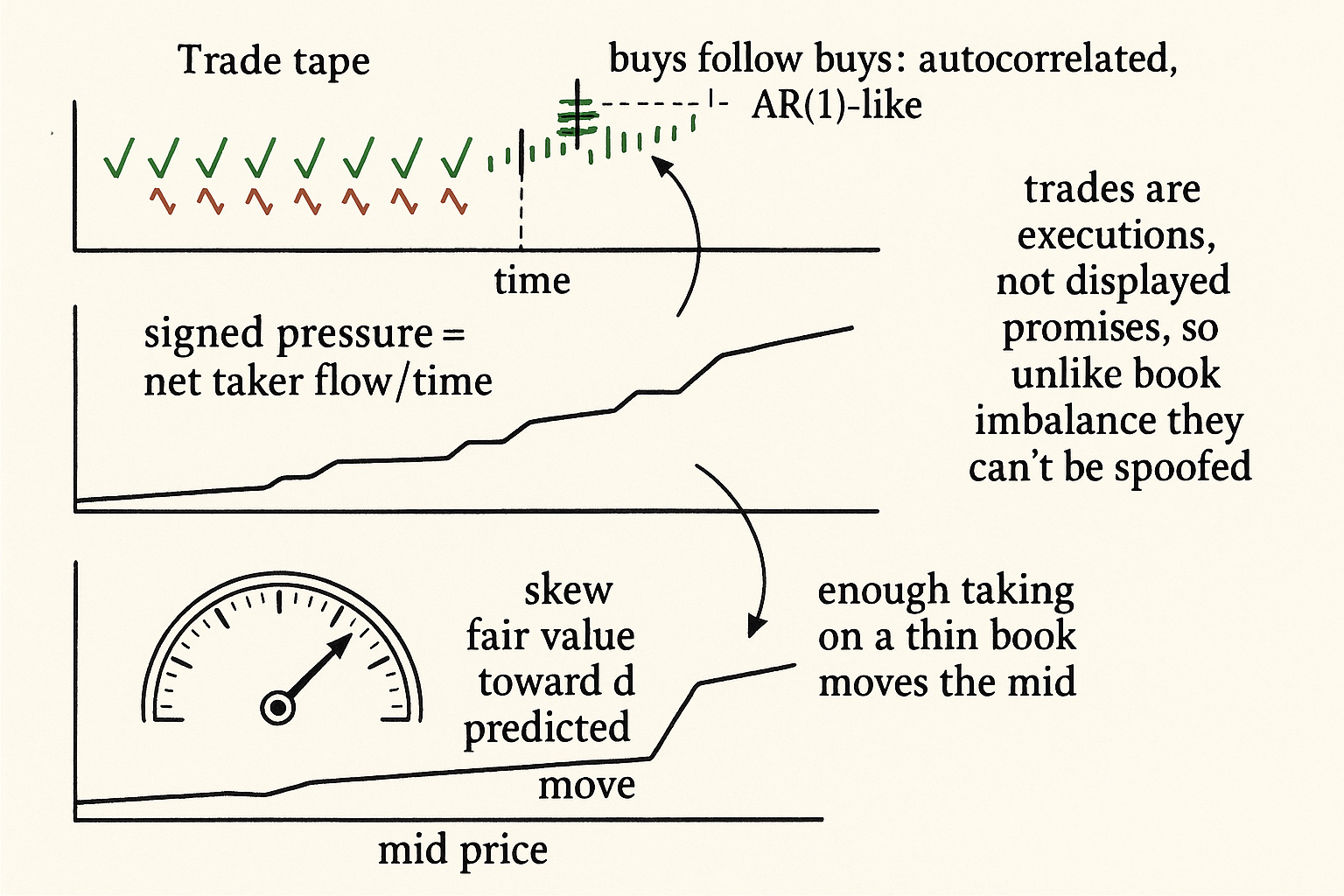

The raw input is the trade tape: each execution has a size and a side, a buy taker or a sell taker. Sign the size by the side, positive for taker buys and negative for taker sells, and sum over a window to get net signed flow, sometimes called pressure.

$$ \text{pressure}_t = \frac{\sum_i s_i \cdot \text{size}_i}{\Delta t}, \quad s_i = +1 \text{ for taker buy}, \; -1 \text{ for taker sell} $$

Pressure over a window is the sum of signed trade sizes divided by the window length, where s_i is the side of trade i. Positive pressure means buyers are leaning on the book harder than sellers; negative means the reverse. This is a flow rate, dollars or units of net taking per unit time, and it is the cleanest summary of which side is consuming liquidity.

Why it predicts: autocorrelation

Trade flow predicts because market orders are autocorrelated and follow roughly an AR(1) process: buys tend to be followed by more buys and sells by more sells, clustering at a low baseline with sudden spikes. A large order is often a slice of a bigger parent order being worked through execution, so seeing taker buys now raises the odds of taker buys in the next moments.

The chain to price is short. If enough taking happens on one side and the book is thin enough, the mid moves, because the takers consume the resting liquidity and walk the price. So predicting trades predicts price changes: forecast that buy pressure will persist, and you forecast the mid will drift up. The autocorrelation is the engine, the same statistical property that makes the feature actionable rather than instantaneous noise.

There is an immediate defensive use too. If you see a burst of taker buys, you should not be sitting there with sell orders feeding those takers cheap liquidity, because you will be left short into a market that is about to climb. Trade flow tells you which side is dangerous to quote on right now.

Fold it into fair value

The forecast enters the same way imbalance does: regress the signed-flow feature against future changes in your basic fair price, and skew the center toward the prediction. Positive pressure predicts an up move, so you lean fair value up, which tightens your bid and widens your ask, the skew from "Why Skewing Is Simpler Than People Think", expressed through a forecast rather than through inventory.

Trade flow and imbalance are complementary, not redundant. Imbalance reads intentions posted to the book, which can be spoofed; trade flow reads executions, which are real and cannot be faked the same way, since a trade is a completed transaction, not a displayed promise. Combining a resting-liquidity feature with a taken-liquidity feature gives a center that respects both what the book shows and what the tape does. "Order Book Imbalance: The First Microstructure Feature to Test" builds the first, and the microprice in "Microprice: Better Than Mid Price?" is where both can be folded into the center.

The limits

Trade flow is a short-horizon signal with the usual caveats. The autocorrelation decays fast, so the prediction is for the next seconds, not minutes, and stale flow is worthless. The signing can be wrong when the data does not cleanly mark the aggressor side, and a mis-signed tape produces a backwards feature. And the relationship between flow and price depends on book thickness: the same pressure moves a thin book and barely budges a thick one, so flow should be read together with the resting liquidity rather than alone. It is a strong, real feature, and it is one input to a center, not a standalone strategy.

Visualizing trade flow

KEY POINTS

- Trade flow reads liquidity being taken (executed trades), the opposite of order book imbalance, which reads liquidity being posted. A maker cares where people take liquidity, because takers move price and fill quotes.

- Sign each trade by its side, positive for taker buys and negative for taker sells, and sum over a window to get net signed flow (pressure), a rate of net taking per unit time.

- It predicts because market orders are autocorrelated and follow roughly an AR(1) process: buys follow buys, sells follow sells. Predicting trades predicts price, since enough taking on a thin book moves the mid.

- Defensive use: a burst of taker buys means you should not be feeding sell orders into it, or you end up short into a rising market.

- Fold it into fair value by regressing signed flow against future fair-price changes and skewing the center toward the prediction, the same way imbalance enters.

- Trade flow and imbalance are complementary: imbalance reads spoofable intentions, trade flow reads real executions that cannot be faked the same way. The microprice can carry both.

- Limits: the autocorrelation decays fast (next seconds, not minutes), the aggressor signing can be wrong in messy data, and the flow-to-price link depends on book thickness, so read it with resting liquidity, not alone.

References

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Optimal High-Frequency Trading in a Pro-Rata Microstructure with

- Evidence from Blue Ocean ATS and NASDAQ Regular Trading Hours

- Bridging the Reality Gap in Limit Order Book Simulation 1 - arXiv

- Deep Limit Order Book Forecasting A microstructural guide - arXiv

- Alpha Decay and Institutional Trading

- Price predictability at ultra-high frequency: Entropy-based ... - arXiv

- Event-Based Limit Order Book Simulation under a Neural Hawkes

- Market Simulation under Adverse Selection - arXiv

- The price impact of order book events: market orders, limit orders and cancellations

- Information-based trading, price impact of trades, and trade autocorrelation

- Why is equity order flow so persistent?

- Deep Order Flow Imbalance: Extracting Alpha at Multiple Horizons from the Limit Order Book

- Trade Co-occurrence, Trade Flow Decomposition, and Conditional Order Imbalance in Equity Markets

- Order Book Filtration and Directional Signal Extraction at High Frequency

- The impact of market orders (Chapter in "Market Microstructure" / related Cambridge volume)

- The short-term predictability of returns in order book markets: A deep learning approach

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.