5.8 Why Skewing Is Simpler Than People Think

Skewing is the academic favorite and the desk's afterthought. Make one side wider so it fills less, lean harder against aggression, and skip the stochastic control. Keep it simple.

Skewing is the most published topic in academic market making and the most over-engineered idea on a real desk. The papers wrap it in stochastic-control equations, Hamilton-Jacobi-Bellman solutions, optimal inventory trajectories. The actual operation is this: make one side of your quote wider than the other so that side fills less, and the cheaper side fills more, which moves your inventory the way you want. That is the whole mechanism. You do not need a complex skewing model, and the elaborate machinery mostly polishes the least important of the three pillars.

"The Three Pillars of Market Making: Fair Price, Spread, Skew" ranked skew last on purpose. This article explains why the simple version is enough, building on the toxicity argument from "Toxic Flow vs Inventory Risk".

The mechanism in one move

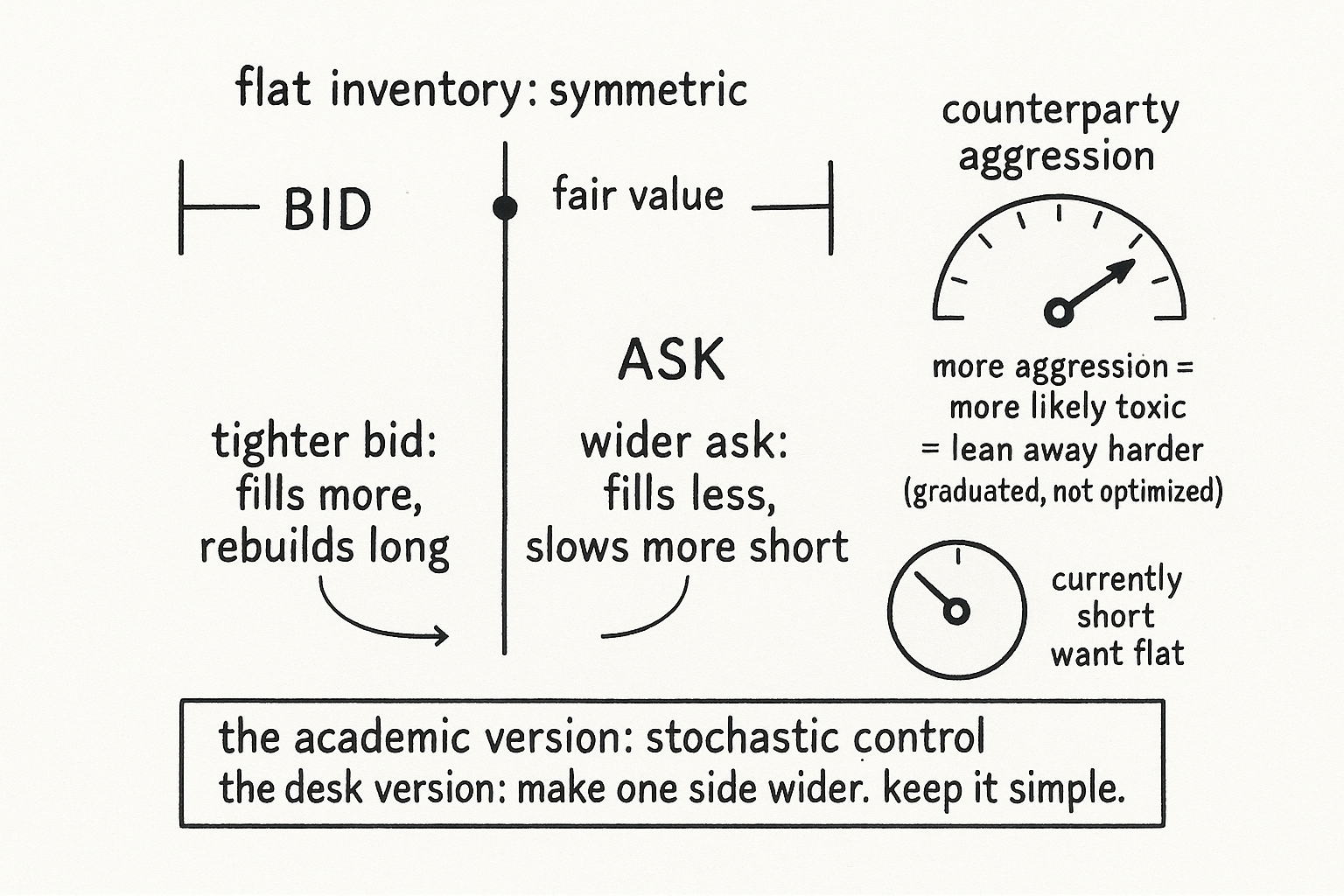

You have a center (fair value) and a spread on each side. To skew, you push one side out and pull the other in around that center. Short some inventory and want to get flatter? Tighten your bid and widen your ask. The tighter bid gets hit more often, rebuilding your long side; the wider ask gets lifted less often, slowing the bleed of more short. Over the next batch of fills your inventory drifts back toward your target. Reverse it to shed a long. The asymmetry of the two distances is the entire control.

There is nothing to solve here that needs an optimizer. A skew proportional to your inventory, leaning harder the further you are from flat, does the job. The marginal gain from a theoretically optimal skew schedule over a simple proportional one is tiny next to the gain from getting the fair value right, which is why the effort ranking matters.

Why simple is enough: the target is toxicity, not variance

The reason the simple version suffices traces back to what skew actually defends against. If skew existed to minimize the variance of your inventory, the precise schedule would matter, because you would be solving a genuine optimization of risk against spread captured. But skew does not exist for that. It exists to stop informed traders from loading you with toxic inventory, and that job is coarse by nature.

You do not need a finely tuned response to refuse a toxic loading. You need to lean away from aggression fast enough that an informed trader cannot pile a large position onto you cheaply. A blunt, simple skew does that as well as a precise one, because the thing you are stopping is itself blunt: someone hammering one side of your book.

The one rule that matters: graduate with aggression

The single piece of nuance worth keeping is matching your skew to how toxic the counterparty looks, and aggression is the proxy for toxicity. The more aggressive someone becomes, the more likely they are an informed player, so you widen against them gradually in line with their impact.

A light, occasional taker on one side is probably non-toxic, and as the toxicity argument says you should not skew hard against benign flow, since you give up spread refusing inventory that was never going to hurt you. Hold some of it. A relentless aggressor running through one side and moving the price is probably informed, and you lean away from them harder the more they push. The skew is a graduated response to observed aggression, not a fixed inventory-control law. Aggression you can measure in real time; the optimal control law you cannot, and you do not need to.

$$ \text{ask offset} = \text{base} + k \cdot (\text{inventory lean}) + g \cdot (\text{observed aggression on this side}) $$

The ask offset is a base spread plus a term proportional to your inventory (the standard inventory lean, with constant k) plus a term proportional to how aggressively that side is being taken (constant g). Both k and g are simple, hand-set constants. The second term is the toxicity defense; the first is the inventory nudge. No optimizer is involved, and that is the point.

Visualizing the skew

KEY POINTS

- Skewing is the most published and most over-engineered topic in market making. The real operation: make one side wider so it fills less and the other side fills more, moving your inventory the way you want.

- A skew proportional to inventory, leaning harder the further you are from flat, does the job. There is nothing here that needs an optimizer, and the gain over a theoretically optimal schedule is tiny next to getting fair value right.

- Simple suffices because skew defends against toxic loading, not inventory variance. Refusing a toxic loading is a coarse job, so a blunt skew works as well as a precise one.

- The one rule worth keeping: graduate the skew with counterparty aggression, the proxy for toxicity. Light flow is probably benign and should not be skewed against hard; a relentless aggressor gets leaned away from harder.

- A practical skew is a base spread plus an inventory-lean term plus an aggression term, all with simple hand-set constants. The aggression term is the toxicity defense, the inventory term is the nudge.

- Aggression is measurable in real time; the optimal control law is not, and you do not need it.

References

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Optimal High-Frequency Trading in a Pro-Rata Microstructure with Predictable Spread Dynamics

- Market Making under a Weakly Consistent Limit Order Book Model

- The Predictive Power of Limit Order Book for Future Volatility, Trade Prices, and Market Depth

- Optimal Quoting under Adverse Selection and Price Reading

- Short-Horizon Excess Returns in Liquid Equities

- Deep Limit Order Book Forecasting A microstructural guide - arXiv

- Market Simulation under Adverse Selection - arXiv

- Order Book Filtration and Directional Signal Extraction at ... - arXiv

- FX Market Making with Internal Liquidity

- Market Making with Competition

- Navigating the Fill Probability vs. Post-Fill Returns Trade-Off

- Market‐Maker Mechanism, Information Asymmetry, and Market Quality

- The Market-Level Evidence of Limit Order Book Asymmetry

- A Specialist's Quoted Depth and the Limit Order Book

- Market Simulation under Adverse Selection

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.