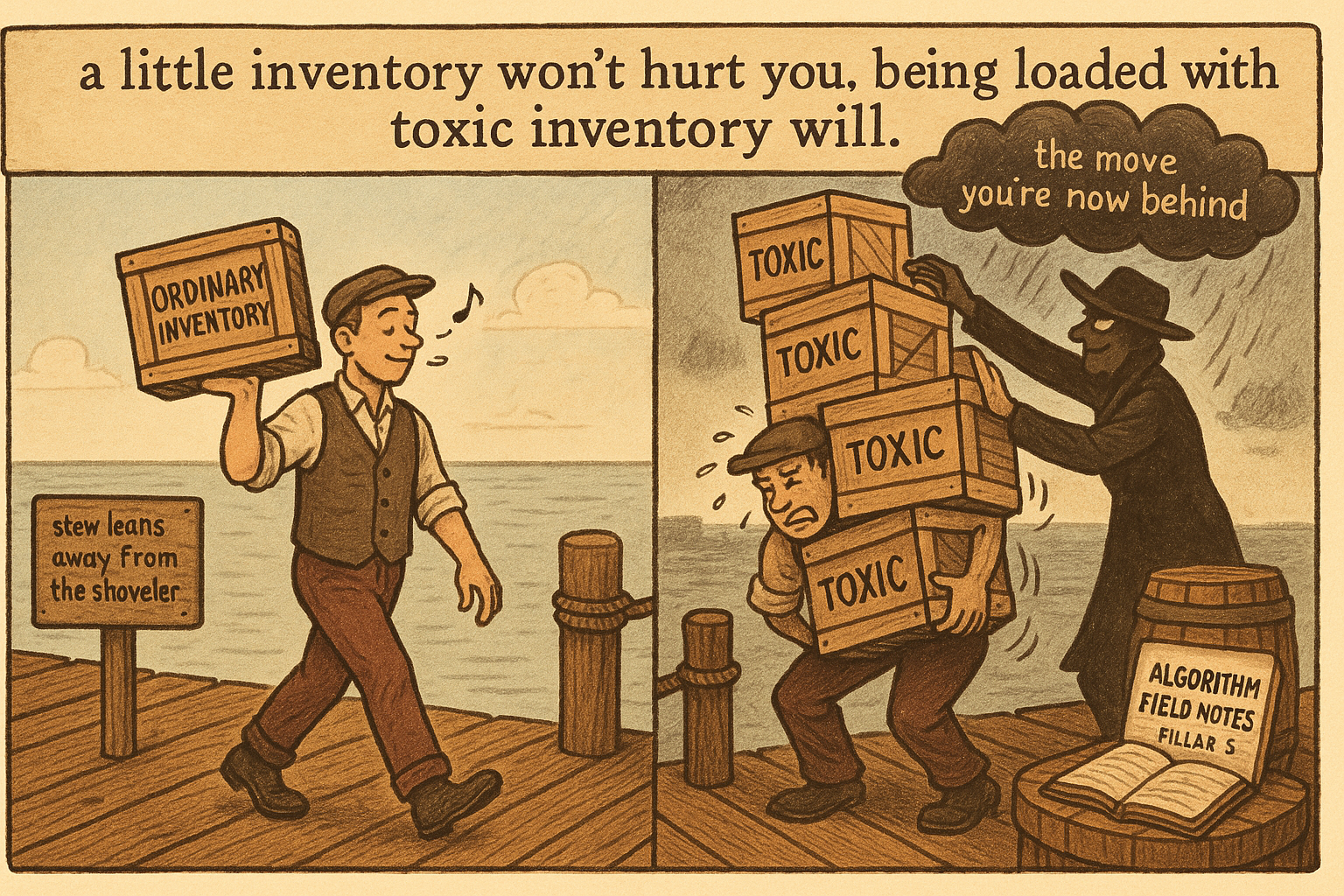

5.7 Toxic Flow vs Inventory Risk

Holding some inventory is benign. Being loaded with toxic inventory by someone who knows it'll move against you kills the book. Skew exists to stop the loading, not to tidy variance.

The textbook market making problem is framed as inventory risk. You hold a position, the position has variance, the variance is risk, so you build elaborate machinery to keep inventory near zero. That framing puts the effort in the wrong place. Holding some inventory is not a serious problem. Holding toxic inventory, and a lot of it, is the problem that kills the book, and the two are not the same thing at all.

This article draws the line that "Adverse Selection Explained for Traders" set up and that "Why Skewing Is Simpler Than People Think" relies on. Confuse toxic flow with inventory risk and you build a skewing model that fights the wrong enemy.

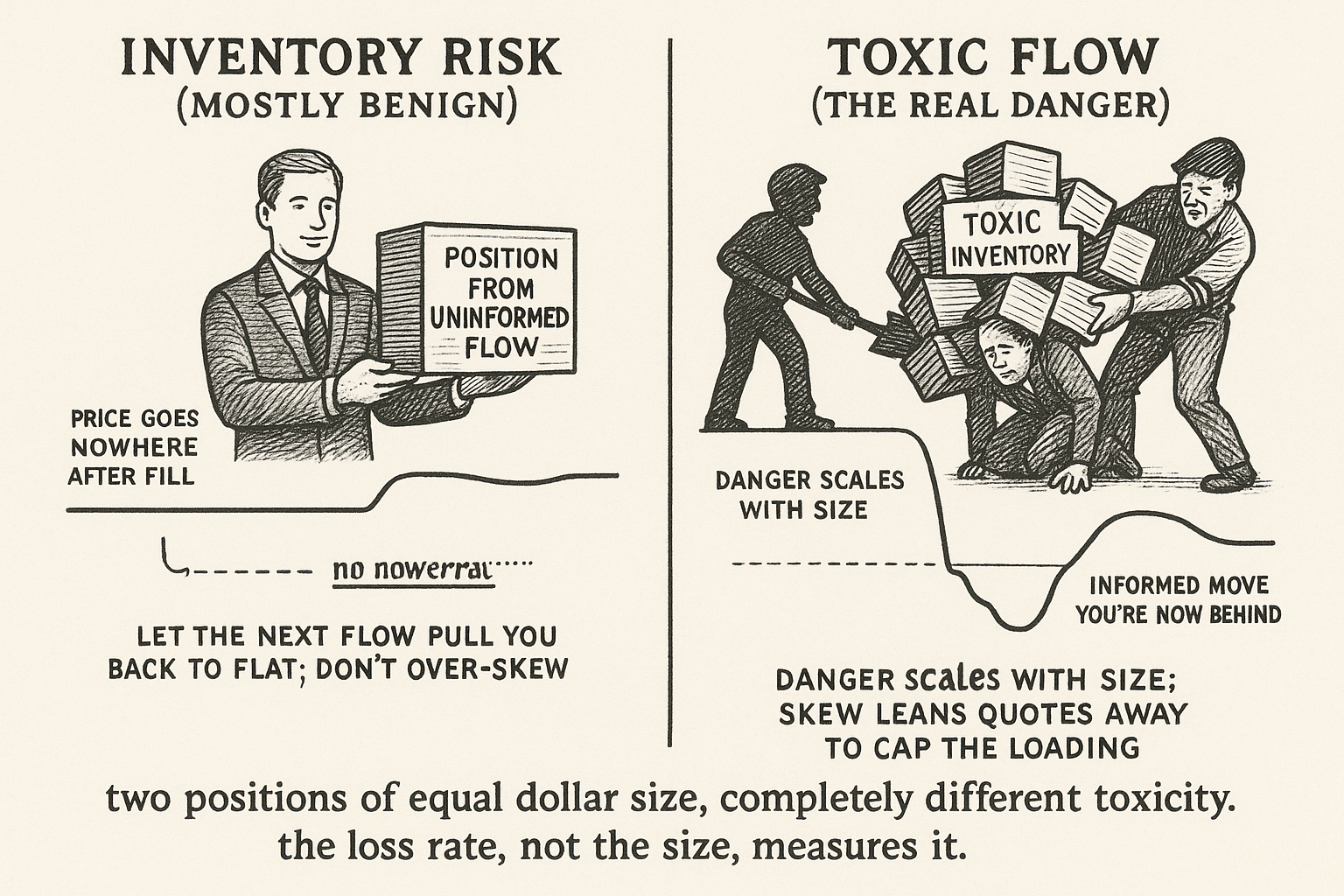

Inventory risk is mostly benign

A position you accumulate from uninformed flow is just a position. It has variance, and variance is uncomfortable, but the expected value of the path is roughly flat, because the people who filled you had no edge over your fair value. You are long some coin because balanced two-sided flow happened to leave you long. Sit on it, let the next round of flow pull you back toward flat, and the holding cost is the ordinary variance of a position centered on a fair price.

The mistake is treating that benign variance as the central danger and skewing hard to flatten it. Skew too aggressively on non-toxic flow and you give up spread you did not need to give up, refusing inventory that was never going to hurt you. As a rule, if the flow is clearly non-toxic you should not skew aggressively and should be willing to hold some risk. Even a net imbalance can be absorbed when it is probably not an informed imbalance.

Toxic flow is the real danger

Toxic inventory is a position handed to you by someone who knows it is about to move against you. The danger is not the variance of the position. It is the negative drift, the informed move that the toxic counterparty was front of and you are now behind. And the danger scales with size: a small toxic position is a small bleed, but an informed trader who can load you with a large toxic position at a fixed price has handed you a large guaranteed loss.

The markout curve from "Markouts: The Truth Serum of Market Making" is how you tell the two apart. Non-toxic inventory shows a flat markout, the price goes nowhere special after the fill. Toxic inventory shows the decaying trough, the price keeps moving against you. Two positions of identical dollar size can carry completely different toxicity, and the loss rate on the inventory, not its size, is what measures it.

What skew is actually defending

This reframing changes the job of skew. Skew is not there to manage inventory risk in the textbook variance sense. Skew is there to stop informed traders from loading you up with toxic inventory. When the flow turns aggressive on one side, you lean your quotes away from that side so the aggressor cannot keep filling you cheaply, which caps how much toxic inventory they can build before your price has moved against them.

The graduated response follows from this. The more aggressive a counterparty becomes, the more likely they are toxic, so you widen your quotes against them gradually in line with their impact. A timid taker gets near-normal quotes; an aggressor who keeps hitting one side and moving the price gets progressively worse prices from you, because their aggression is itself the evidence of toxicity. You are not flattening a position. You are refusing to be the cheap counterparty to someone who knows where the price is going.

The hedging trap that follows

The same confusion produces a second, expensive mistake on the risk-management side: hedging toxic inventory with a correlated instrument and believing you are now flat. The correlations in your model do not necessarily hold, and when they break you discover the hedge was toxic too. A book that trusts its correlation matrix will happily take on enormous toxic inventory believing it is fully hedged, then get adversely filled on both legs when the correlation fails. You can be adversely selected on nearly anything, and a hedge built on an assumed correlation is one more thing to be adversely selected on. The defense against toxic flow is pricing it out through skew and spread, not netting it against a correlation you do not control.

Visualizing the distinction

KEY POINTS

- The textbook frames market making as inventory risk and builds machinery to flatten positions. That puts effort in the wrong place: holding some inventory is benign, holding a lot of toxic inventory is what kills the book.

- Inventory from uninformed flow is just a position with variance and roughly flat expected path. Skewing hard to flatten it gives up spread you did not need to give up.

- If flow is clearly non-toxic, do not skew aggressively; hold some risk and absorb even a net imbalance, since it is probably not an informed imbalance.

- Toxic inventory carries negative drift, not just variance, and the danger scales with size: an informed trader loading you large at a fixed price hands you a large guaranteed loss.

- The markout curve separates the two: flat for non-toxic, a decaying trough for toxic. Equal-size positions can differ entirely in toxicity, measured by loss rate, not size.

- Skew's real job is stopping informed traders from loading you with toxic inventory, not textbook variance management. Widen against a counterparty gradually as their aggression (the evidence of toxicity) rises.

- Hedging toxic inventory with a correlated instrument is a trap: when the assumed correlation breaks you get adversely filled on both legs. Price toxic flow out with skew and spread instead of netting it against a correlation you do not control.

References

- The Art of Currency Trading - Brent Donnelly (Amazon)

- ‘Toxic’ Order Flow

- Detecting Toxic Flow

- Unwinding Toxic Flow with Partial Information

- Market Simulation under Adverse Selection

- Liquidity Provision, Adverse Selection, and Competition

- Market making under a weakly consistent limit order book model

- Deep Limit Order Book Forecasting: A Microstructural Guide

- HFT, Price Improvement, Adverse Selection: An Expensive Way to

- High frequency market making: The role of speed

- Arbitrage-free Limit Order Books and the Pricing of Order Flow Risk

- Market Making with Alpha Signals

- Market Making without Adverse Selection: Evidence from Retail Trading

- Detecting Toxic Flow

- A Simple Strategy to Deal with Toxic Flow

- Unwinding Toxic Flow with Partial Information

- Optimal Quoting under Adverse Selection and Price Reading - arXiv

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.