5.4 Markouts: The Truth Serum of Market Making

The markout asks one question of every fill: what did the price do next? It ignores the spread you collected and the cleverness you intended, exposing toxic flow as a curve that sinks.

A market maker can tell a flattering story about any fill. The spread was captured, the quote was tight, the volume was good. The markout ignores the story and asks one question: what did the price do right after the fill printed? Measure the change in price in the seconds following each of your trades and the flattering story collapses into a number that is either positive or negative. That number is the truth serum, because it does not care how clever your quote looked, only whether the market ran through it.

This article defines the measurement that "Why Fair Value Is the Core of Market Making" leaned on and that "Toxicity and Adverse Selection" in the order-book material treats as the central diagnostic. Markouts sit under almost every later refinement in this pillar.

What a markout is

A markout is the change in price after a fill, measured at a chosen horizon. Record the price you filled at, look at a reference price (the mid is the usual choice) some interval later, and take the difference, signed by the side you traded so that a profitable outcome is positive.

$$ \text{markout}(\tau) = s \cdot \left( \text{mid}_{t+\tau} - p_{\text{fill}} \right), \quad s = +1 \text{ if you bought}, \; -1 \text{ if you sold} $$

The sign s flips the difference so a buy that is followed by a rising mid scores positive and a sell followed by a falling mid scores positive. Compute this for every fill, average across many fills, and you have the average markout, the cleanest available estimate of whether your quotes are centered on the future or the past.

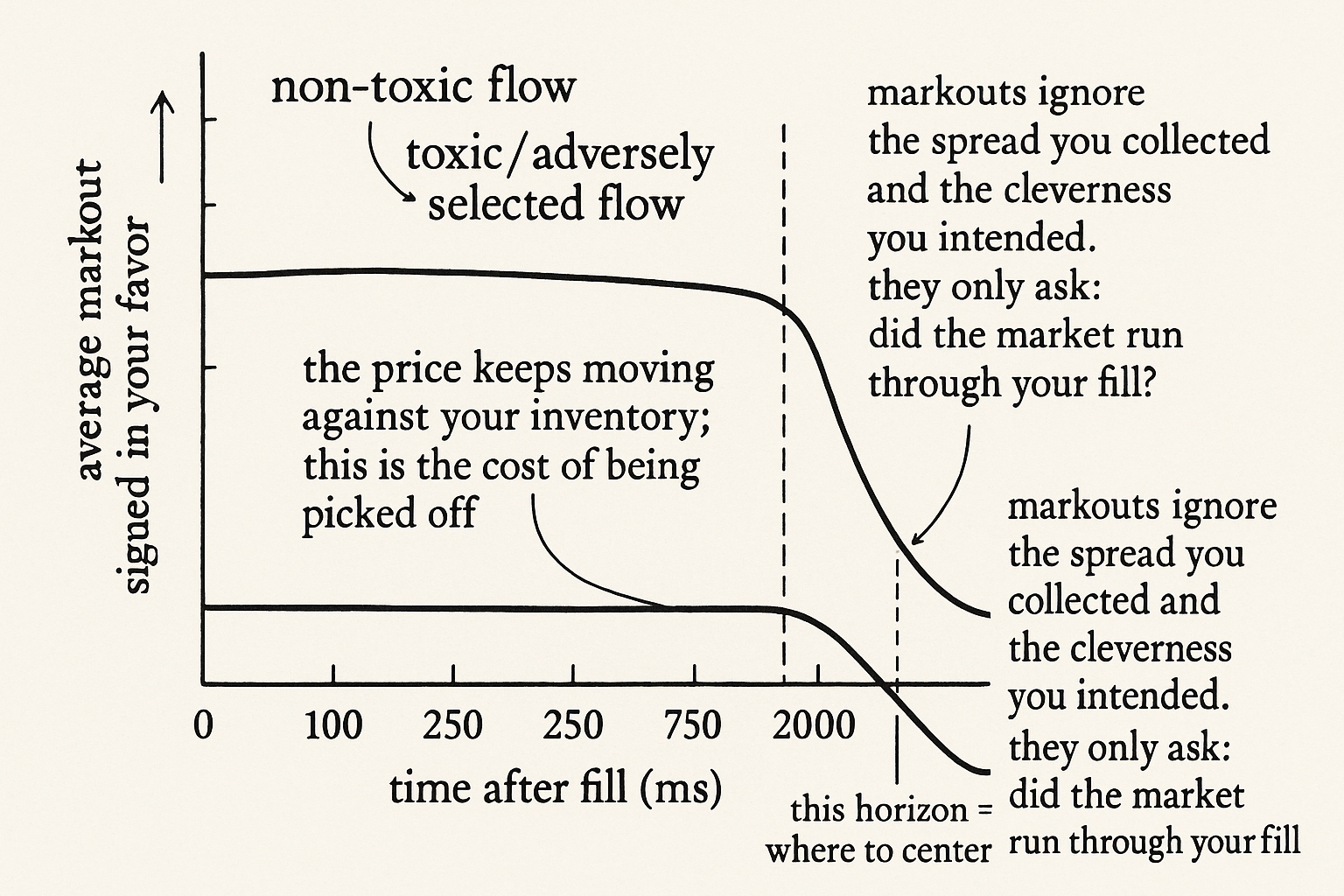

Read it as a curve, not a point

A single horizon hides the shape. Compute the markout at a sweep of horizons (50 ms, 100 ms, 250 ms, 750 ms, 2 s) and plot the average against the horizon. The curve is the story of what your inventory does to you over time.

The classic adverse-selection signature is a curve that starts near zero and decays downward: right after the fill you look flat, and as the seconds pass the price keeps moving against you, the loss deepening as the informed move you were on the wrong side of plays out. The depth of the trough and the horizon at which it bottoms tell you how toxic the flow is and over what timescale the damage lands. That bottoming horizon is the same one that defines where you should center fair value, which is why the two articles share the 750 millisecond figure.

Why it is the truth serum

Markouts strip out the two things traders use to flatter themselves. They ignore the spread you collected, since the markout measures only the post-fill price path, so a fill that banked 2 bps of spread but lost 10 bps to an adverse move shows up as the loser it is. And they ignore intent, since the price does not know you meant to be clever.

This makes the markout the validator that overrides the quoted spread. A book can show a healthy gross spread and a deeply negative average markout at the same time, which means it is collecting pennies and losing dollars to the people picking it off. No other single number catches that as fast.

What you do with it

Markouts are not only a scorecard, they are a control input. Three uses run through this pillar.

First, fair-value placement. The horizon where the markout curve bottoms is the horizon your fair value should forecast to, so a desk reads the markout shape to decide where to center quotes. Second, defense. Widen spreads on the instruments, sides, or conditions where your markouts are worst, since a bad markout marks exactly the flow you should be charging more to interact with. "Spread Widening During Volatility Expansion" runs this logic on the volatility dimension.

Third, instrument selection. Track the rolling average markout (a five-second markout works) of every trade in a symbol as an EWMA, before you ever quote it, and the symbols that sustain genuinely good markouts are the non-toxic ones worth quoting. "Dynamic Symbol Selection for Market Makers" turns this into a live filter, and the same signal can scale your size up on names you make money on and cut it fast on names you do not.

Visualizing the markout curve

KEY POINTS

- A markout is the change in price after a fill at a chosen horizon, signed by your side so a favorable outcome is positive. Averaged across many fills it estimates whether your quotes are centered on the future or the past.

- Read markouts as a curve across horizons (50 ms to a few seconds), not a single point. The shape is the story of what your inventory does to you over time.

- The adverse-selection signature is a curve starting near zero and decaying into a trough: the price keeps moving against you as the informed move plays out. Trough depth and timing measure toxicity.

- Markouts are the truth serum because they ignore the spread you collected and the intent behind the quote. A book can show a healthy gross spread and a deeply negative markout at once.

- The horizon where the markout bottoms is the horizon your fair value should forecast to, linking markouts directly to where you center quotes.

- Use markouts as a control: place fair value at the trough horizon, widen spreads where markouts are worst, and select instruments by tracking the rolling EWMA markout of every trade before you quote.

- The same signal scales size up on names you make money on and cuts it fast on names you lose on.

References

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Algorithmic Trading and Market Quality: International Evidence

- Market Making with Deep Reinforcement Learning from Limit Order

- Predicting Adverse Selection in High-Frequency Cryptocurrency

- Deep Limit Order Book Forecasting A microstructural guide - arXiv

- Market Simulation under Adverse Selection - arXiv

- High‐Frequency Price Discovery and Price Efficiency on Interest

- Order Book Filtration and Directional Signal Extraction at ... - arXiv

- Optimal Quoting under Adverse Selection and Price Reading - arXiv

- High Frequency Market Making

- Detecting toxic flow

- Bitcoin wild moves: Evidence from order flow toxicity and price jumps

- Differential access to dark markets and execution outcomes

- Decomposing the Cost of Trend Following

- arXiv:2410.19107v2 [q-fin.TR] 17 Jan 2025

- Attention: How high-frequency trading improves price efficiency

- Zero-shot adaptation to order book dynamicsPreprint. Draft version.

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.