5.9 Spread Widening During Volatility Expansion

Blow your spreads out when volatility does, because a fixed markup that was safe in a calm tape becomes a gift to informed traders in a moving one. Around scheduled news, stop quoting entirely.

The width of your quote is the dial that trades fill frequency against profit per fill, and the single most important thing that dial responds to is volatility. The rule is blunt: blow your spreads out when the market's volatility does. A fixed markup that was safe in a calm tape becomes a gift to informed traders the moment the market starts moving, because the same spread now covers a fraction of the distance the price can travel before you reprice.

This article builds the spread pillar from "The Three Pillars of Market Making: Fair Price, Spread, Skew" and uses the markout diagnostic from "Markouts: The Truth Serum of Market Making" to decide where the widening should bite.

Start fixed, then add a volatility layer

The most basic spread is a fixed markup on your skewed fair value. Quote a constant number of basis points on each side and leave it. It works in a stationary market and fails the instant volatility regime-shifts, which crypto does constantly.

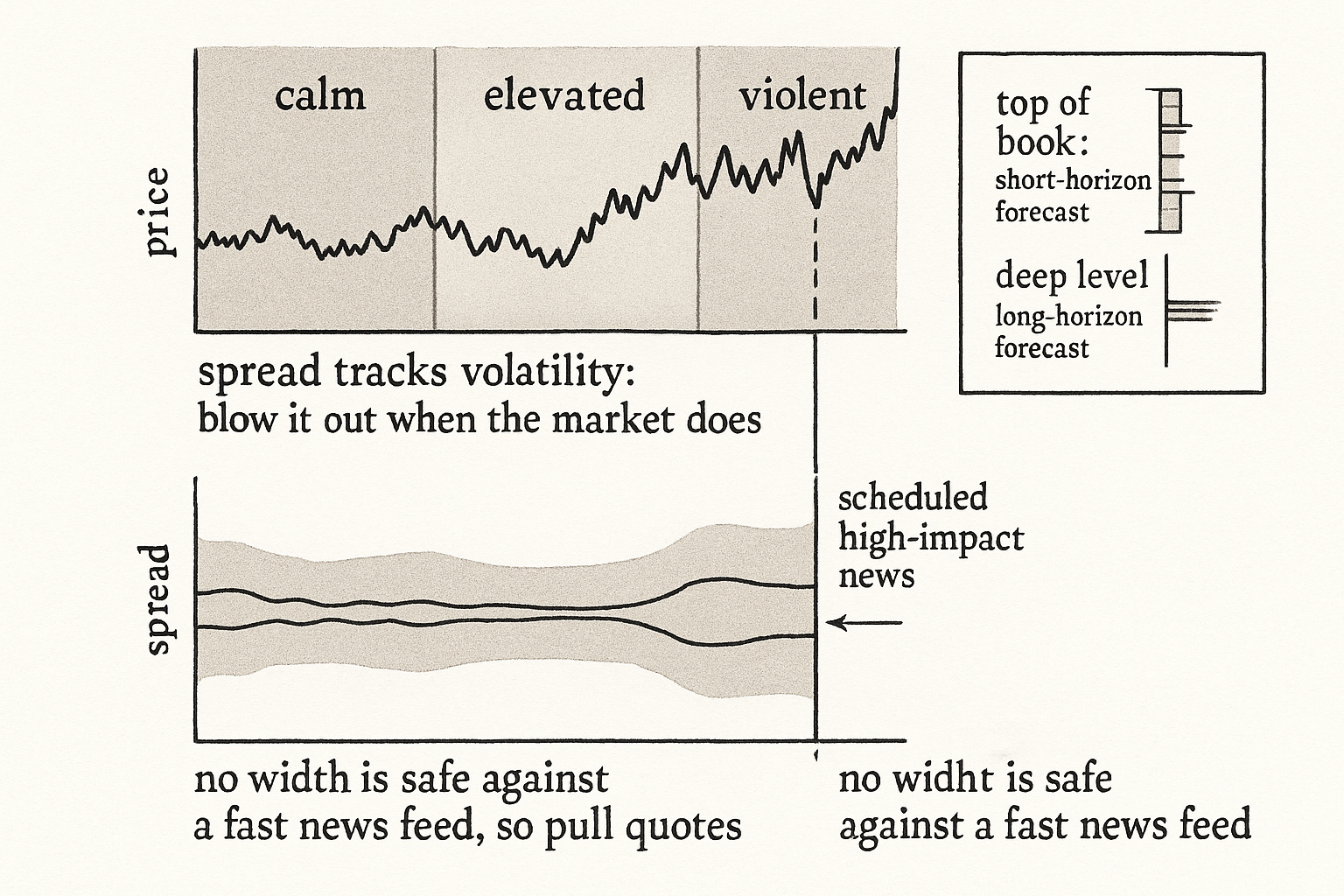

The next model adds layers of wider spread as volatility rises. Estimate short-horizon volatility, your own fair-value volatility is a clean choice, and map it to a spread width: calm regime, tight spread; elevated regime, wider; violent regime, widest. The mapping can be discrete, three regimes set by volatility quantiles each with its own width, or continuous, interpolating the width between regime anchors so the spread moves smoothly as volatility drifts. Either way the spread is now a function of volatility rather than a constant.

$$ \text{spread}_t = \text{base} \cdot \left( 1 + \lambda \cdot \frac{\sigma_t}{\bar{\sigma}} \right) $$

The spread at time t is a base width scaled up by the ratio of current volatility sigma-t to its average sigma-bar, with a sensitivity constant lambda. When current volatility sits at its average the ratio is one and the spread is near base; when volatility doubles, the spread expands by lambda times the excess. The exact functional form is less important than the direction: more volatility, more width.

Why widen, in adverse-selection terms

The reason is the adverse selection from "Adverse Selection Explained for Traders". Volatility is the size of the move the market can make between now and the moment you can reprice. A larger possible move means a larger chance an informed trader runs through your stale quote before you adjust, and a larger loss when they do. Wider spreads during volatility buy protection in the exact moments getting picked off costs the most, because the price can travel further against your fill.

The markout tells you whether the widening is calibrated. If your markouts stay bad during high-volatility periods even after widening, you are not widening enough; if they are fine, the width is doing its job. Read the markout curve conditional on volatility regime and let it set how aggressively the spread should respond.

Different fair value per depth

Advanced desks attach a different fair value to each quoting depth, because quotes at different depths worry about different horizons. A quote sitting at the top of the book is exposed to getting picked off in the next minutes, so it is priced against a short-horizon forecast and reacts fast to short-horizon volatility. A deep quote will only fill on a large move, so it is concerned with longer-term forecasts and longer-horizon volatility. Running one fair value and one volatility estimate across all depths misprices both ends; matching the horizon of the forecast and the volatility to the depth of the quote prices each level for the risk it actually faces.

The news case: sometimes stop quoting

Beyond the smooth volatility response, there is a discrete defense. You can add modifications that blow your spread out conditional on spread-specific alpha, signals in the order book that news has been released. The clearest case is scheduled high-impact news. Some firms stop quoting entirely around high-impact news, because the informed traders with fast news feeds will pick off any quote you leave up, and no reasonable spread is wide enough to cover the gap risk. Scheduled events at least give advance warning, so a desk can widen drastically or pull quotes from the start rather than reacting after the first informed fill has already landed. Widening is the continuous defense; pulling quotes is the discrete one for the moments when no width is safe.

Visualizing the response

KEY POINTS

- Spread is the dial trading fill frequency against profit per fill, and its most important input is volatility. The rule: blow your spreads out when the market's volatility does.

- A fixed markup is safe only in a stationary market. Add a volatility layer that maps short-horizon volatility (your own fair-value volatility is a clean choice) to width, discretely by regime or continuously by interpolation.

- A simple form scales a base width by the ratio of current to average volatility. The exact function matters less than the direction: more volatility, more width.

- The reason is adverse selection. Volatility is the size of the move possible before you reprice, so it raises both the chance and the cost of getting picked off. Wider spreads protect exactly when pick-offs cost most.

- Calibrate with markouts conditional on volatility regime. Bad markouts in high-volatility periods after widening mean you are not widening enough.

- Advanced desks attach a different fair value and volatility horizon to each depth: top-of-book quotes price a short horizon, deep quotes price a long one.

- The discrete defense is stopping quotes around scheduled high-impact news, where informed fast-feed traders pick off any quote and no width is safe. Scheduled events give advance warning to pull or widen from the start.

References

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Market Makers and the Dynamics of Volatility Demand

- Insider Trading and the Bid-Ask Spread: A Critical Evaluation of the Adverse Selection Theory

- Analysts’ Information-Based Trading and Market Making

- Politically Affiliated Market Makers

- Market Making under a Weakly Consistent Limit Order Book Model

- Optimal High-Frequency Trading in a Pro-Rata Microstructure with Predictive Information

- ECNs, Market Makers, and the Components of the Bid-Ask Spread

- Short-Horizon Excess Returns in Liquid Equities

- Anticipations of Foreign Exchange Volatility and Bid-Ask Spreads

- Microstructure effects, bid–ask spreads and volatility in the spot foreign exchange market pre and post-EMU

- Currency volatility and bid-ask spreads of ADRs and local shares

- Informed Traders and Limit Order Markets

- The Market-Level Evidence of Limit Order Book Asymmetry

- Liquidity Supply and Adverse Selection in a Pure Limit Order Book

- High-Frequency Market Making During Stressed Periods

- Market conditions, fragility, and the economics of market making

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.