5.10 Order Placement Alpha: The Forgotten Edge

Order placement, the exact tick you rest on, matters more than skewing. Sit just in front of a large sturdy order so takers can't push the price through your fill, and your markouts improve.

Fair value, spread, and skew decide the levels you want to quote at. They do not decide the exact tick you rest your order on, and that last decision, where inside the small neighborhood of your target level you actually place, is its own source of edge. Order placement modification is more important than skewing, and almost nobody writes about it. The academic literature spends its time on inventory control while the practical money sits in an unglamorous adjustment made after the three pillars have already spoken.

This article covers the fourth decision the three pillars articles deferred. It pairs with "How to Use Order Book Density for Better Limit Orders", which works through the density analysis that drives the placement.

What order placement is

Once fair value, spread, and skew have set the level you want to quote, you make an ad hoc modification to the precise placement of the order around that level. The goal is to extract a little more edge for very little change in fill probability. You are not changing your view or your width. You are nudging the order a tick or two to a better spot within the neighborhood your strategy already chose, where "better" means improved markouts and hidden flow without meaningfully changing how often you fill.

Three things the modification buys you: a bit more edge per fill, improved markouts, and concealment of your flow so other participants cannot read your intentions off the book. The first is the obvious one. The second and third are where the real value sits.

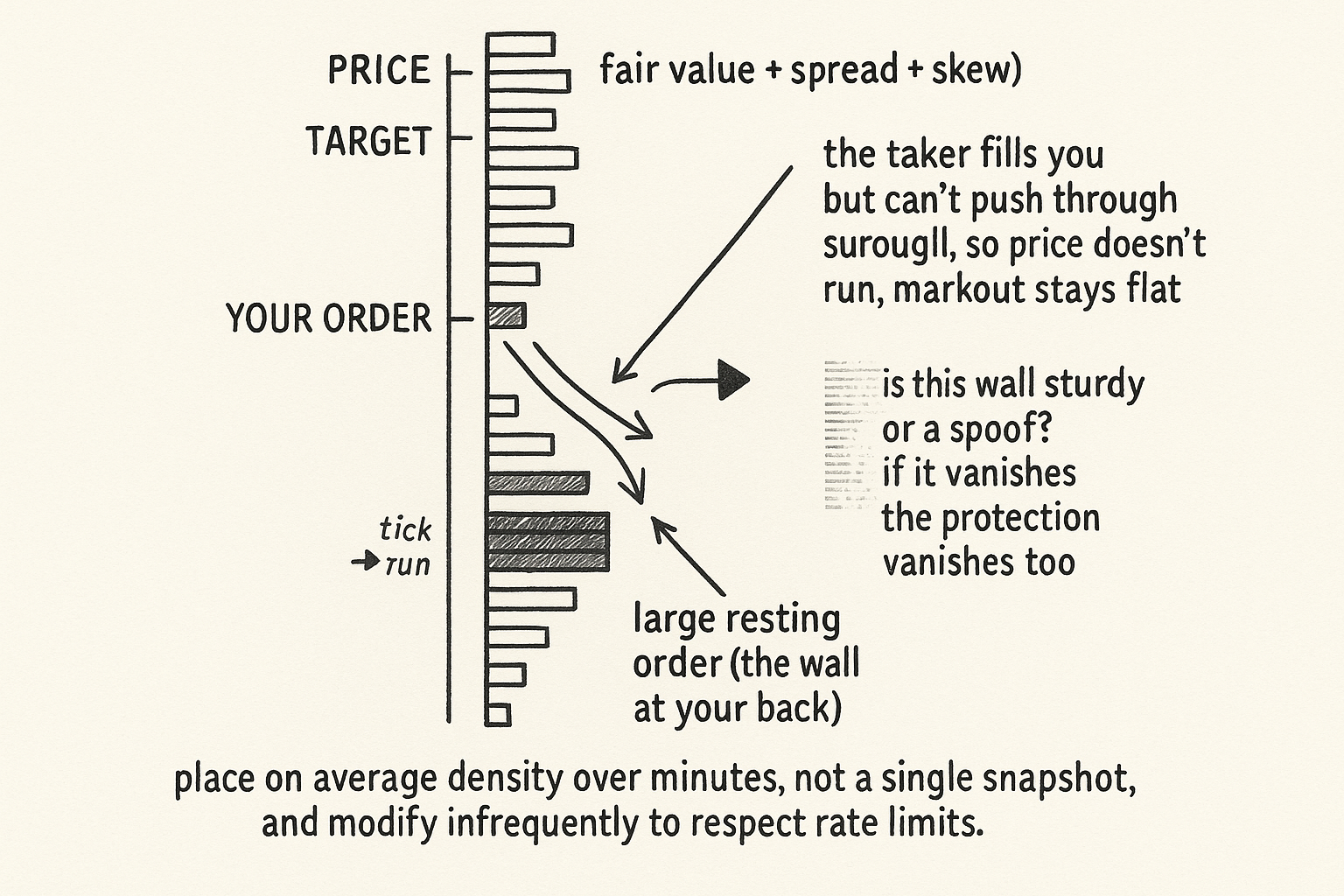

Placing in front of size improves markouts

The sharpest placement trick uses the resting liquidity around you. Place your order just in front of a large resting order and your markouts improve, for a mechanical reason. If a taker fills you, they then have to get through the large order sitting right behind you to push the price further against your fill. They usually cannot. The large order behind you absorbs the continuation, so the price does not run, and your markout stays flat instead of sinking into the adverse-selection trough from "Markouts: The Truth Serum of Market Making".

The large order is a wall at your back. Sitting just in front of it means anyone who hits you is immediately blocked from moving the price, so the fills you take in that spot are systematically less toxic than fills taken in open water with nothing behind them.

Read density over minutes, not snapshots

The placement decision runs on average book density, not the instantaneous snapshot. Take the average density over the course of several minutes and find the optimal spot to place within your target neighborhood, because a single snapshot is noise: orders flicker in and out, and a wall that is there this instant may be gone the next. The multi-minute average tells you where liquidity reliably sits.

For large-scale quoting there is a rate-limit constraint. One-upping other participants tick by tick burns through your order-update budget, so you only want to apply these placement modifications infrequently, matching them at a measured cadence rather than chasing every flicker. The analysis also trades size against tightness: you weight the benefit of skipping past a chunk of density against the cost of the increased aggression that skipping requires, and the optimal placement falls out of that trade-off. "How to Use Order Book Density for Better Limit Orders" builds this density analysis in full.

The spoofing complication

One hazard hangs over all of it. Placing in front of a large order assumes the large order is real. In crypto a lot of large orders are spoofs that vanish before they fill, and placing in front of a spoof is worthless: when the spoof disappears the wall at your back is gone, and the price turns toward where the order was because the book pressure has shifted. So order placement that leans on resting size has to be paired with logic that decides which orders are sturdy and which will evaporate, the subject of "Spoofing, Sturdy Liquidity, and Book Pressure". Place in front of sturdy size and your markouts improve; place in front of a spoof and you get the adverse move you were trying to avoid.

Visualizing the placement

KEY POINTS

- Fair value, spread, and skew set the level you want to quote. Order placement is the separate decision of the exact tick to rest on within that level, and it is more important than skewing.

- The modification extracts a little more edge for very little change in fill probability. Its main value is improved markouts and hidden flow, not just extra edge per fill.

- Placing just in front of a large resting order improves markouts: a taker who fills you is then blocked by the large order behind you from pushing the price further, so your fill is less toxic.

- Run placement on average book density over several minutes, not an instantaneous snapshot, because single snapshots are noise and walls flicker in and out.

- Large-scale quoting hits rate limits, so apply placement modifications infrequently rather than one-upping every tick, and trade size against tightness when deciding how far to skip.

- The hazard is spoofing: placing in front of a spoofed order is worthless because the wall vanishes before it protects you, and the price turns toward where the order was. Pair placement with logic that judges which orders are sturdy.

References

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Market Making and Mean Reversion

- Liquidity Provision, Adverse Selection, and Competition in High-Frequency Market Making

- Analysis of the Limit Order Book and Order Flow in the Paris Bourse

- Optimal High-Frequency Trading in a Pro-Rata Microstructure with

- The Term Structure of Machine Learning Alpha

- Market Liquidity and Convexity of Order-Book - arXiv

- Full article: Deep limit order book forecasting: a microstructural guide

- Decoding CTA Allocations by Trend Horizon

- Optimal order placement in limit order markets

- Optimal Placement in a Limit Order Book

- Optimal Execution in a Limit Order Book and an Associated Microstructure Market Impact Model

- Mid-Price Prediction in a Limit Order Book

- Limit Order Book Shape and Return Distribution*

- CME Iceberg Order Detection and Prediction

- A Pure-Jump Market-Making Model for High-Frequency Trading - arXiv

- The Impact of Market Informedness on Market Makers' Profitability

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.