5.2 The Three Pillars of Market Making: Fair Price, Spread, Skew

A market maker's quote is three stacked decisions: fair price, spread, skew. Fair price carries more than the other two combined, and skew, the academic favorite, is the trivial one.

Every two-sided quote a market maker posts comes out of three decisions stacked on top of each other. Pick a center price you believe is fair. Add a spread on each side to set how wide you sit. Lean the whole thing left or right depending on the inventory you already carry. Fair price, spread, skew. That is the entire machine, and the order matters because the three pillars carry wildly different weight.

The previous article, "Market Making Is Not Just Collecting the Spread", argued the job is forecasting and survival rather than passive spread capture. This one names the three controls that do the work and ranks them by how much they decide your profit.

Pillar one: fair price, and why it dominates

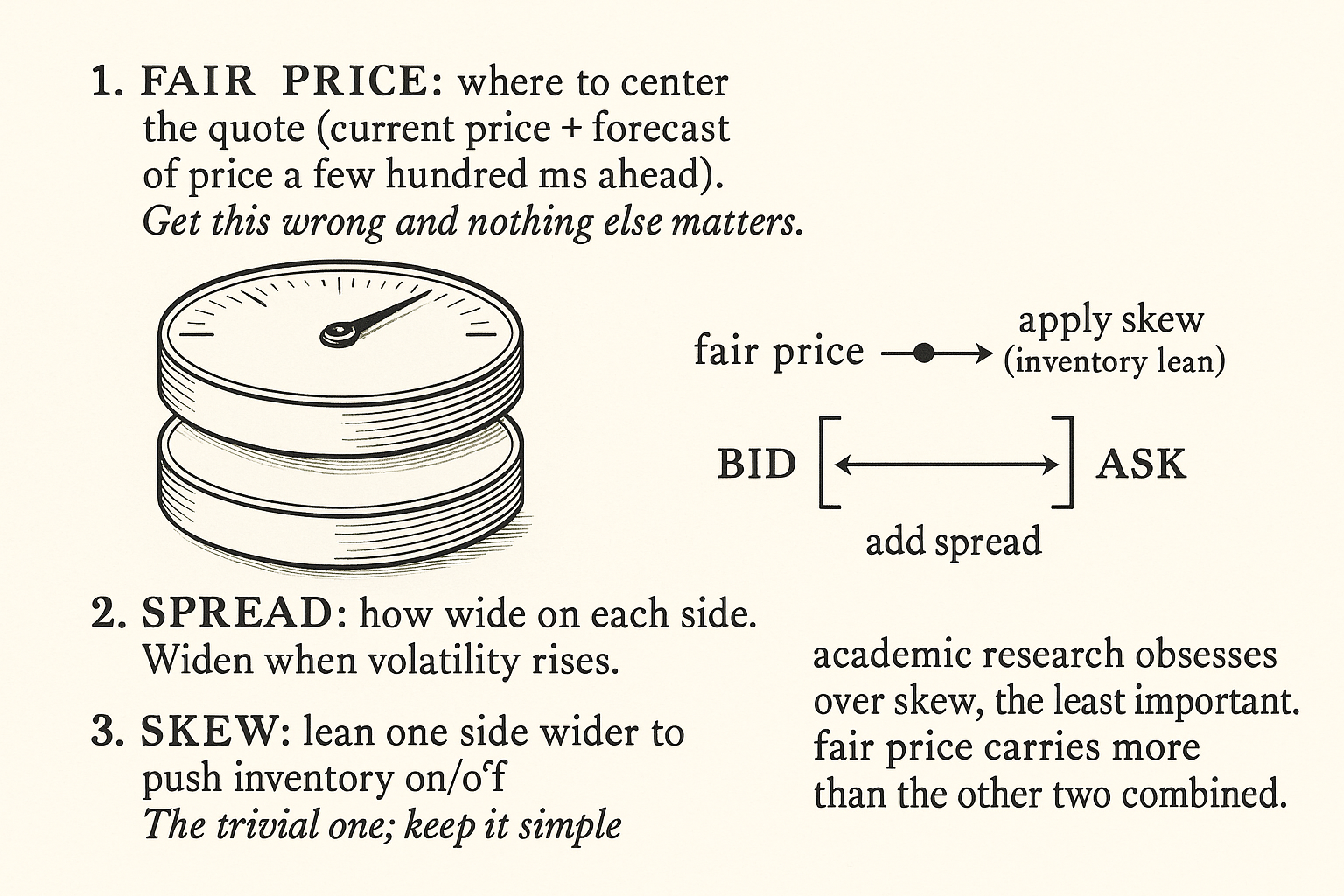

Fair price is the center you quote around, and it carries more of the result than the other two combined. The working definition is operational: fair price is the price that, when you quote around it, gives you good markouts. Markout is the change in price after one of your fills, the measure of whether your quote was centered on the future or on the past. Quote around a number that the market drifts away from and every fill bleeds; quote around a number the market sits at and your fills break even before you collect any spread.

A first version of fair price needs no forecast at all. Take the mid price of the most liquid venue, Binance for most crypto, and quote around that. Improve it by using a volume-weighted mid across the top exchanges instead of one venue's mid. A real edge layers a forecast on top: the current price plus a prediction of where the price will sit a few hundred milliseconds from now, so the fast traders with good forecasts cannot pick you off by quoting a better center than yours.

The failure mode is concrete. Quote on a small exchange and treat that exchange's own mid as the value of Bitcoin, and you have started from a bad number, because the small venue lags the large one. "Why Fair Value Is the Core of Market Making" works through how to build the center properly, and "Cross-Exchange Fair Value for Crypto Perps" handles the multi-venue case.

Pillar two: spread, the width dial

Spread is how wide you sit around the fair price, and it controls the trade-off between how often you get filled and how much you make per fill. The most basic version is a fixed markup on the skewed fair value. The next version widens the markup when volatility rises.

The rule is to blow your spreads out when the market's volatility does. Volatility means larger moves between now and whenever you can adjust, which means more chance an informed trader runs through your quote before you reprice. Wider spreads buy you protection during the exact moments when getting picked off costs the most. Advanced desks attach a different fair value to each quoting depth, because a quote sitting at the top of the book worries about getting picked off in the next minutes while a deep quote worries about longer-horizon forecasts. "Spread Widening During Volatility Expansion" covers the width-control logic in full.

Pillar three: skew, and why it is the trivial one

Skew makes one side of your quote wider than the other so that one side fills more than the other, which lets you push inventory on or take it off. Short too much? Skew so your bid is more aggressive and your ask backs away, and the next fills rebuild your position toward flat.

The academic literature treats skew as the hard problem, the place for elaborate inventory-control equations. In practice it is the most trivial of the three pillars and needs no complex model. Most people think skewing manages inventory risk. The risk of holding some inventory is not the real problem. Holding toxic inventory, and a lot of it, is the problem, and skew earns its keep by stopping informed traders from loading you up. You do not need a fancy skewing model. Keep it simple. "Why Skewing Is Simpler Than People Think" and "Toxic Flow vs Inventory Risk" take this apart.

Stacking the three into a quote

The construction runs in order. Start with the fair price, your best estimate of the center including any forecast. Apply skew around that center based on your current position, so your aversion to inventory leans the quotes. Add the spread on each side of the skewed center to get the actual buy and sell prices you post. Often a desk runs multiple quoters at once with different settings, a grid of quotes at different depths, each with its own fair value and width.

The ranking is the lesson. Fair price first, spread second, skew a distant third. Effort spent perfecting the skew model while the fair price is mis-centered is effort spent polishing the least important pillar while the most important one leaks.

Visualizing the stack

KEY POINTS

- Every quote is three stacked decisions: fair price (the center), spread (the width), and skew (the lean based on inventory). The order reflects how much each decides your profit.

- Fair price dominates and carries more than the other two combined. Operationally it is the price that gives good markouts when you quote around it.

- A first fair price is just the most-liquid venue's mid; a better one is a volume-weighted mid across top exchanges; a real edge adds a forecast of where price sits a few hundred milliseconds ahead.

- Spread sets the fill-frequency versus profit-per-fill trade-off. Widen it when volatility rises, since that is when getting picked off costs the most. Advanced desks attach a different fair value to each depth.

- Skew leans one side wider to push inventory on or off. The literature treats it as the hard problem; in practice it is trivial and needs no complex model.

- Skew's real job is blocking informed traders from loading you with toxic inventory, not managing ordinary inventory risk. Keep it simple.

- Construction order: start at fair price, apply skew for your position, then add spread on each side. Desks often run a grid of quoters at different depths, each with its own fair value and width.

References

- The Art of Currency Trading - Brent Donnelly (Amazon)

- High-frequency market-making with inventory constraints and directional bets

- Market making under a weakly consistent limit order book model

- Deep Limit Order Book Forecasting A microstructural guide - arXiv

- Market Simulation under Adverse Selection - arXiv

- Market-maker's Profit Maximisation in Spread and Price Setting

- Optimal Quoting under Adverse Selection and Price Reading - arXiv

- Order Book Filtration and Directional Signal Extraction at ... - arXiv

- Evidence from Blue Ocean ATS and NASDAQ Regular Trading Hours

- High-frequency market making: The role of speed

- High-Frequency Market Making: Liquidity Provision, Adverse Selection, and Competition

- High Frequency Trading

- Market Simulation under Adverse Selection

- Toward Understanding the Fair Price in High-Frequency Markets

- Limit Order Book Shape and Return Distribution: On the (Market Microstructure) Origins of the Return Distribution

- Market Making with Scaled Beta Policies

- Deep Limit Order Book Forecasting: A Microstructural Guide

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.