5.21 Cross-Exchange Fair Value for Crypto Perps

On a follower crypto venue, your local mid is stale. Build fair value from the leader: regress the basis against Binance's mid, blend global and local prices, and respect the stablecoin rates.

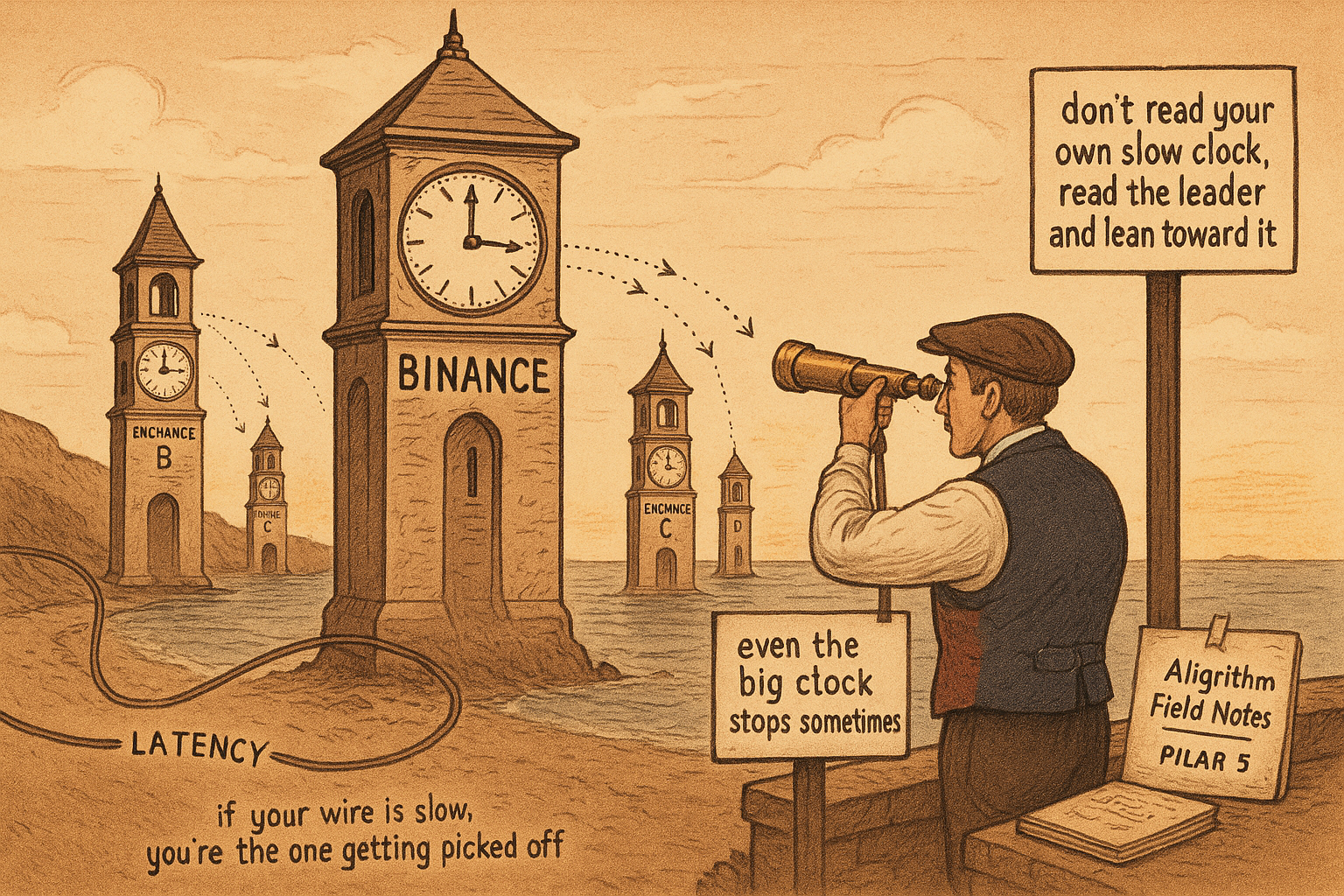

Quote a perpetual on a mid-size exchange using that exchange's own mid price as your fair value, and you have started from a bad number. Crypto is fragmented across dozens of venues that do not move together, and the smaller venues follow the larger ones with a lag. A market maker on a follower exchange who treats its local mid as the truth is quoting around a stale price, and every fast trader who saw the leader move first picks them off. The fix is to build fair value from the whole cross-exchange picture, with the dominant venue as the leader that pulls the laggards.

This article extends "Why Fair Value Is the Core of Market Making" to the multi-venue reality of crypto perpetuals, the hardest and most important place to get the center right.

The leader-laggard structure

Crypto venues form a hierarchy. The largest, Binance for most pairs, leads, and the smaller exchanges lag, tending to drift toward wherever the leader's price went. So the leader's price is information about where the laggard's price is about to go, and a market maker on a laggard venue should treat the leader as a forecast of their own near-future mid, not as a separate market.

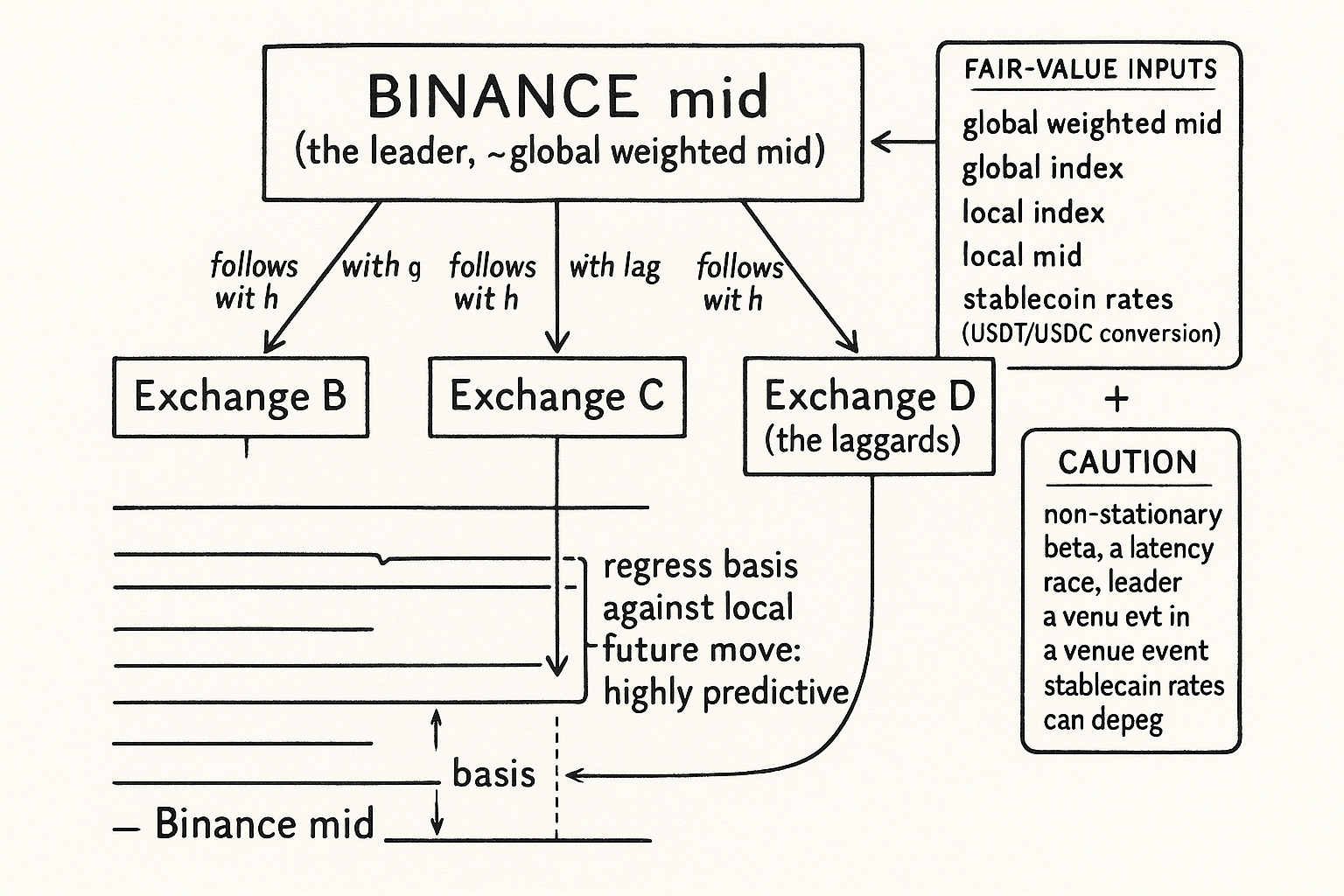

In a simplified model, take the Binance mid price as a proxy for the globally weighted mid, which works because its market share is large enough that its mid is close to the volume-weighted consensus. Then quantify the lead-lag: regress the basis, the difference between the Binance mid and your exchange's mid, against your exchange's future mid-price changes.

$$ \Delta \text{mid}^{\text{local}}_{t \to t+\tau} = \beta \cdot \big( \text{mid}^{\text{Binance}}_t - \text{mid}^{\text{local}}_t \big) + \varepsilon $$

The future change in your local mid over horizon tau is proportional, with coefficient beta, to the current basis between the Binance mid and your local mid. The basis is the gap, and the regression says your local price will close that gap, moving toward Binance. This relationship is highly predictive, because most smaller exchanges follow Binance, so the basis is a clean lead signal you fold straight into your local fair value: when Binance trades above your local mid, lean your fair value up, and when below, lean it down.

The full perp fair value

The simplified Binance-mid proxy is a starting point. A proper perpetual fair value blends several venue-level prices, because no single number captures it. The inputs a desk combines: the globally volume-weighted mid across exchanges, the globally weighted index price, the local index price, the local mid price, and the stablecoin rates needed to convert between contracts denominated in different quote currencies.

The global mid leads and pulls the laggard exchanges, so you weight it heavily when forecasting where local prices will go. The local mid and local index anchor where you actually trade. The stablecoin rates matter because a perp quoted in USDT and a perp quoted in USDC are not directly comparable until you account for the USDT-USDC rate, and ignoring that conversion misprices the cross-venue basis. Combining these gives a fair value that respects both the global leader and the local microstructure of the venue you quote on.

Layer the standard predictive factors on top of the cross-exchange basis: funding rates, the lead-lag between spot and perp, volatility, rate of trading, book imbalance from "Order Book Imbalance: The First Microstructure Feature to Test", and momentum. Each adds information about where the price is heading, and you tune their weights over time as you learn how the price evolves. The cross-exchange basis is usually the single strongest of these on a follower venue, because it is the most direct read on the leader's information advantage.

Spot has extra constraints

The spot case is the same problem with two added constraints. Spot fair value must respect triangular arbitrage bounds, the requirement that the prices of related pairs, say a coin against USDT, against USDC, and the stablecoins against each other, stay consistent or an arbitrage opens. And it must respect cross-exchange arbitrage bounds, the requirement that the same spot asset cannot diverge too far across venues without inviting arbitrage. These bounds constrain how far your fair value can drift from the cross-venue consensus, because a fair value that violates them is a fair value the arbitrageurs will trade against you. For perps the funding mechanism and the index construction play a similar anchoring role, tying the perp to its underlying.

The limits

Cross-exchange fair value is the strongest center on a follower venue, and it carries real fragilities. The lead-lag relationship is non-stationary, so the beta drifts and the regression must be re-estimated continuously, and a stale beta quotes around a relationship that no longer holds. Latency decides whether the edge survives: the whole signal is the leader moving before the laggard, so if your feed from the leader is slow you are the laggard being picked off rather than the maker exploiting the lag, and the cross-exchange game is partly a latency race you can lose. The leader itself can be wrong during a venue-specific event, a Binance outage or a local liquidation cascade, when the usual hierarchy inverts and the follower leads for a moment. And the stablecoin rates that tie the contracts together can themselves dislocate, a USDC depeg being the obvious case, which breaks the conversion the whole fair value rests on. The cross-exchange center is the right one to build, and it is a moving, latency-sensitive estimate, not a constant truth.

Visualizing cross-exchange fair value

KEY POINTS

- Quoting a perp on a mid-size venue using its own mid as fair value starts from a bad number, because crypto is fragmented and smaller venues follow the larger ones with a lag.

- Crypto venues form a leader-laggard hierarchy. The dominant venue (Binance for most pairs) leads, and its mid proxies the globally weighted mid, so it forecasts the laggard's near-future price.

- Quantify the lead-lag by regressing the basis (Binance mid minus local mid) against the local mid's future change. It is highly predictive, so lean your local fair value toward the leader.

- A full perp fair value blends global weighted mid, global index, local index, local mid, and stablecoin rates (needed to compare USDT- and USDC-denominated contracts), weighting the leader heavily.

- Layer standard factors on top: funding rates, spot-perp lead-lag, volatility, trading rate, book imbalance, and momentum, tuning weights over time. The cross-exchange basis is usually the strongest on a follower venue.

- Spot adds triangular and cross-exchange arbitrage bounds that constrain how far fair value can drift from consensus. Perps are anchored by funding and the index.

- Limits: the beta is non-stationary and needs continuous re-estimation; the edge is a latency race you can lose; the leader can invert in a venue-specific event; and the stablecoin rates can depeg, breaking the conversion.

References

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Fundamentals of Perpetual Futures

- Where is the Price of Bitcoin Determined? Price Discovery in a Decentralized Market

- The Impact of Fragmentation in European Equity Markets

- The Cost of Latency in High-Frequency Trading

- Funding Rate Mechanism in Perpetual Futures

- technology and automation in financial trading: a bibliometric review

- THE CHOICE OF TRADING VENUE AND RELATIVE PRICE

- An ADX-Conditioned VWAP Strategy in FX Markets

- Fragmentation, Price Formation and Cross-Impact in Bitcoin Markets

- Market Making in Crypto

- High-frequency dynamics of Bitcoin futures

- Predicting Adverse Selection in High-Frequency Cryptocurrency Markets

- High-Frequency Trading in Cryptocurrency Exchanges: Benefits and Risks

- Cryptocurrency Perpetual Futures and Swaps: A Systematic Literature Review

- Lead-Lag Relationships in Market Microstructure

- To Make, or to Take, That Is the Question: Impact of Adverse Selection on Maker-Taker Choice in High-Frequency Trading

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.