5.17 TWAP and VWAP Are Execution Models, Not Just Indicators

TWAP and VWAP are not indicators to cross over. They are execution benchmarks and the slicing algorithms built to hit them, the machinery for moving a large order without blowing out the price.

Most charting packages list TWAP and VWAP next to the moving averages, as if they were one more line to cross over for a buy signal. That framing misses what they are. TWAP and VWAP are execution benchmarks and the algorithms built to hit them, the machinery a desk uses to push a large order into the market without moving it. Treat VWAP as the most important indicator in quant finance only once you see it as the yardstick execution is measured against, not as a squiggle to trade.

This article reframes two numbers retail traders use as oscillators. It connects to the maker side of this pillar, because the flip side of an execution algorithm working an order is the market maker on the other side of those slices.

The two benchmarks

TWAP is the time-weighted average price, the simple average of price over a period, every observation counted equally.

$$ \text{TWAP} = \frac{1}{N} \sum_{i=1}^{N} P_i $$

The TWAP over a period is the sum of the prices divided by the number of observations N. It weights every moment of the period equally, ignoring how much volume traded at each price.

VWAP is the volume-weighted average price, each price weighted by the volume that traded at it.

$$ \text{VWAP} = \frac{\sum_i P_i V_i}{\sum_i V_i} $$

The VWAP is the sum of price times volume over the sum of volume, so a price where a lot of traded changes the average more than a price where little traded. VWAP answers the question execution actually cares about: what was the average price the market transacted at, weighted by where the trading happened.

They are execution algorithms

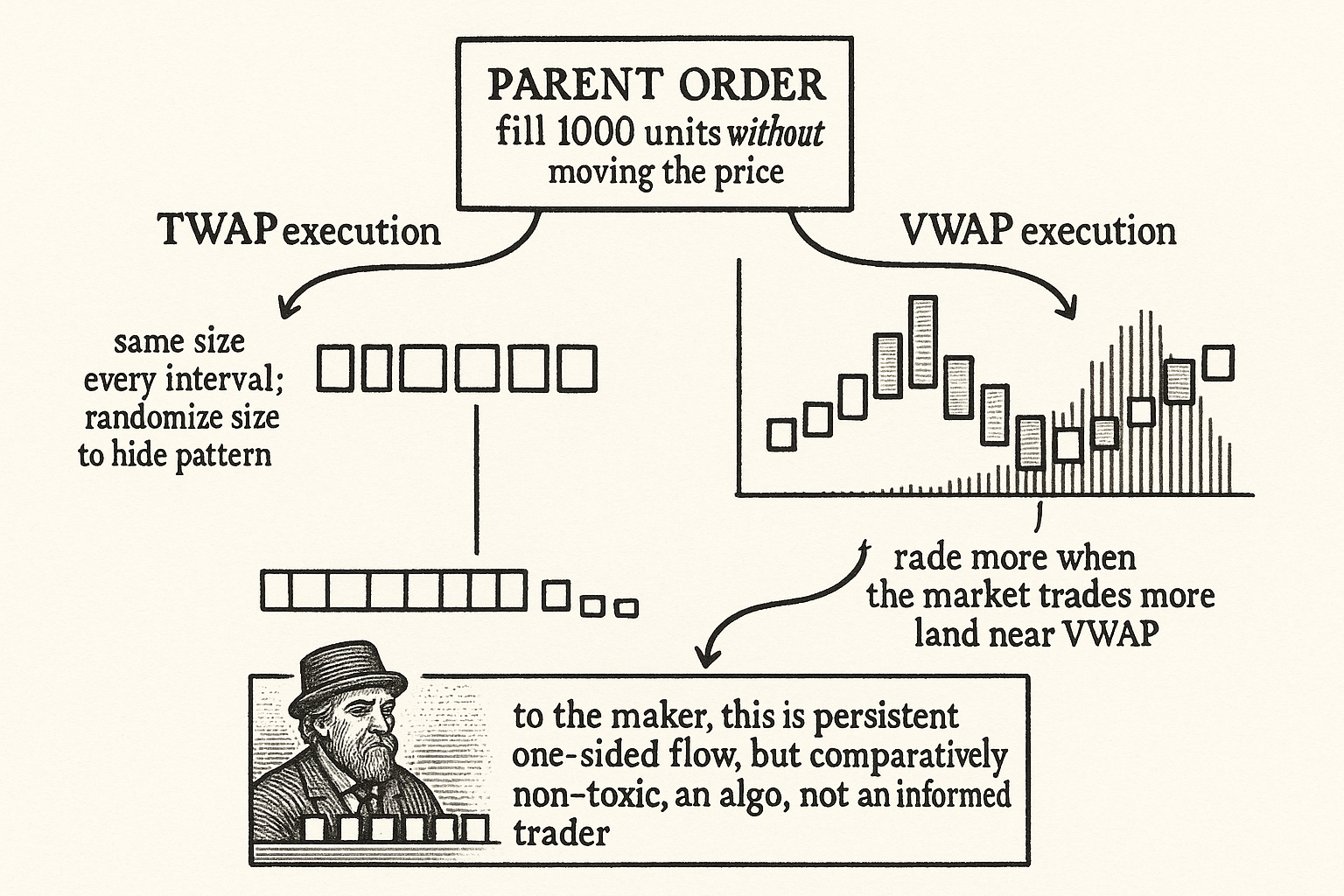

The reason these are execution models is that each benchmark has a matching algorithm designed to achieve it. A TWAP execution buys a fixed quantity every fixed interval: split a large parent order into equal child slices spaced evenly in time, and your average fill price tracks the time-weighted average. To hide the schedule from anyone watching, randomize the slice size so the pattern is not a clean metronome an observer can front-run.

A VWAP execution makes the slice size depend on volume instead of time: trade more when the market trades more, less when it trades less, so your participation tracks the volume profile and your average fill lands near the VWAP. Over the execution window you end up at an average price of roughly the VWAP. The algorithm is leaning the size toward the high-volume parts of the period, because matching the volume profile is what keeps your average at the benchmark.

The point of both: a desk with a large order to fill cannot just cross the spread for the whole size without moving the price against itself. Slicing the order to track TWAP or VWAP spreads the impact across time or volume, so the execution lands near a fair average rather than at a price the order itself blew out.

Why a market maker cares

For the market maker side of this pillar, execution algorithms are the counterparty. A VWAP algorithm working a large buy is a stream of taker buy slices arriving in proportion to volume, which shows up in your trade flow as persistent signed pressure, the autocorrelated buying from "Using Trade Flow to Predict Short-Term Price Movement". Recognizing execution flow matters because it is comparatively non-toxic: an algorithm mechanically working a parent order is not trading on a short-horizon price forecast against you, so the flow it generates is less likely to be the toxic, adversely-selecting flow from "Toxic Flow vs Inventory Risk".

This is why distinguishing execution flow from informed flow is part of the maker's job. The same buy pressure can come from a trader who knows the price is about to jump (toxic, widen against it) or from a VWAP algorithm indifferent to the next tick (benign, you can provide liquidity into it and hold the inventory). Reading which is which, partly from trade size and pattern, is how a maker decides whether a stream of one-sided flow is a threat or a customer.

The limits

TWAP and VWAP as benchmarks have known weaknesses. VWAP is a backward-looking number, the true VWAP of a period is only known after the period ends, so a live VWAP algorithm forecasts the remaining volume profile and is wrong when the profile shifts. Both are gameable: a participant who knows a large VWAP order is working can trade ahead of its predictable slices. And hitting the benchmark is not the same as good execution, since the benchmark itself can be a bad price if the whole period drifted against you. As indicators to trade, a price crossing its VWAP carries far less information than the order-flow features in this pillar; their real value is as the language execution speaks, not as another oscillator.

Visualizing the two algorithms

KEY POINTS

- TWAP and VWAP are execution benchmarks and the algorithms built to hit them, not indicators to cross over. They are the machinery for pushing a large order into the market without moving it.

- TWAP is the equal-weighted average price over a period. VWAP weights each price by the volume traded there, answering what average price the market actually transacted at.

- A TWAP algorithm buys a fixed quantity every fixed interval, randomizing slice size to hide the schedule. A VWAP algorithm sizes slices by volume, trading more when the market trades more, landing near the VWAP.

- Both exist because a desk cannot cross the spread for a whole large order without moving price against itself. Slicing spreads the impact across time or volume.

- For a maker, an execution algorithm is the counterparty: a VWAP buy shows up as persistent autocorrelated buy pressure in trade flow, and it is comparatively non-toxic because the algo is not trading a short-horizon forecast against you.

- Distinguishing execution flow from informed flow (partly via trade size and pattern) decides whether one-sided flow is a threat to widen against or a customer to provide liquidity into.

- Limits: true VWAP is known only after the period, so live algos forecast the remaining profile; both are gameable by anyone who knows the order is working; and hitting the benchmark is not the same as a good price.

References

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Effective Trade Execution

- Optimal VWAP Tracking

- Mean Variance Optimal VWAP Trading

- Algorithmic Trading of Portfolios

- Deep Learning for VWAP Execution in Crypto Markets

- Optimal High-Frequency Trading in a Pro-Rata Microstructure with

- Optimal Quoting under Adverse Selection and Price Reading

- Short-Horizon Excess Returns in Liquid Equities

- Volume-weighted average price tracking: A theoretical and empirical investigation

- Optimal VWAP trading under noisy conditions

- Optimal algorithms for trading large positions

- Analysis and modeling of client order flow in limit order markets

- On-line VWAP Trading Strategies: Sequential Analysis

- Optimal closing benchmarks

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.