4.10 Why Breakout Systems Need Low Noise Environments

A breakout rule is trivial; noise decides if a new high is an entry or a trap. Breakouts need continuation, which only low noise provides, so pick trend-quality markets and gate the entries.

A breakout system buys when price exceeds the highest high of the prior 20 days. The signal itself is trivial; the price either makes a new 20-day high or it does not. What determines whether that signal makes money is not the breakout rule but the environment the breakout fires into. In a low-noise market, a new 20-day high is the leading edge of a sustained move, and the breakout captures most of it. In a high-noise market, a new 20-day high is the top of an oscillation that is about to reverse, and the breakout buys the exact worst price. The rule is identical. The noise environment decides whether the rule is an entry or a trap.

This article is the design consequence of the trend-reversion split for the most popular trend-entry mechanism. "Low Noise Markets Are Trend-Following Markets" established that trend systems need efficient markets; the breakout is the sharpest case because its entire premise, that a new extreme will be followed by continuation, is a direct bet on low noise. A breakout in a high-noise market is a contradiction in terms: you are betting on continuation in a market defined by reversal. The numbers make the dependence stark, which is why breakout systems are the cleanest illustration of why the noise environment is the first design parameter, not the last.

A breakout is a bet that an extreme will not reverse

The breakout logic assumes that when price pushes past a recent boundary, the push will continue rather than snap back. That assumption is the definition of low noise. In a low-noise market, extremes are made by directional flow that keeps going, so the new high is a waypoint, not a destination. In a high-noise market, extremes are made by oscillation that reverses, so the new high is a destination the price immediately leaves, in the wrong direction for your long.

The whipsaw cost is the breakout's structural enemy, and it scales with noise. Every false breakout (a new high that reverses) costs the entry-to-stop distance. In a high-noise market, most breakouts are false because most extremes reverse, so the system pays the whipsaw cost over and over while waiting for the rare breakout that runs. The article "Noise Is Not Volatility" framed high noise as motion that cancels out; for a breakout system, every cancellation is a false signal and a small loss. The breakout does not fail gracefully in noise; it fails repeatedly.

The source material on breakout design points at the same dependence from the other direction: the value of a breakout improves when the lookback is long enough to filter noise but short enough to catch the trend, and that balance only exists when there is a trend to catch. In a market with no sustained direction at any reasonable lookback, no breakout length works, because the thing the breakout is trying to catch is not present.

The hit-rate math that low noise rescues

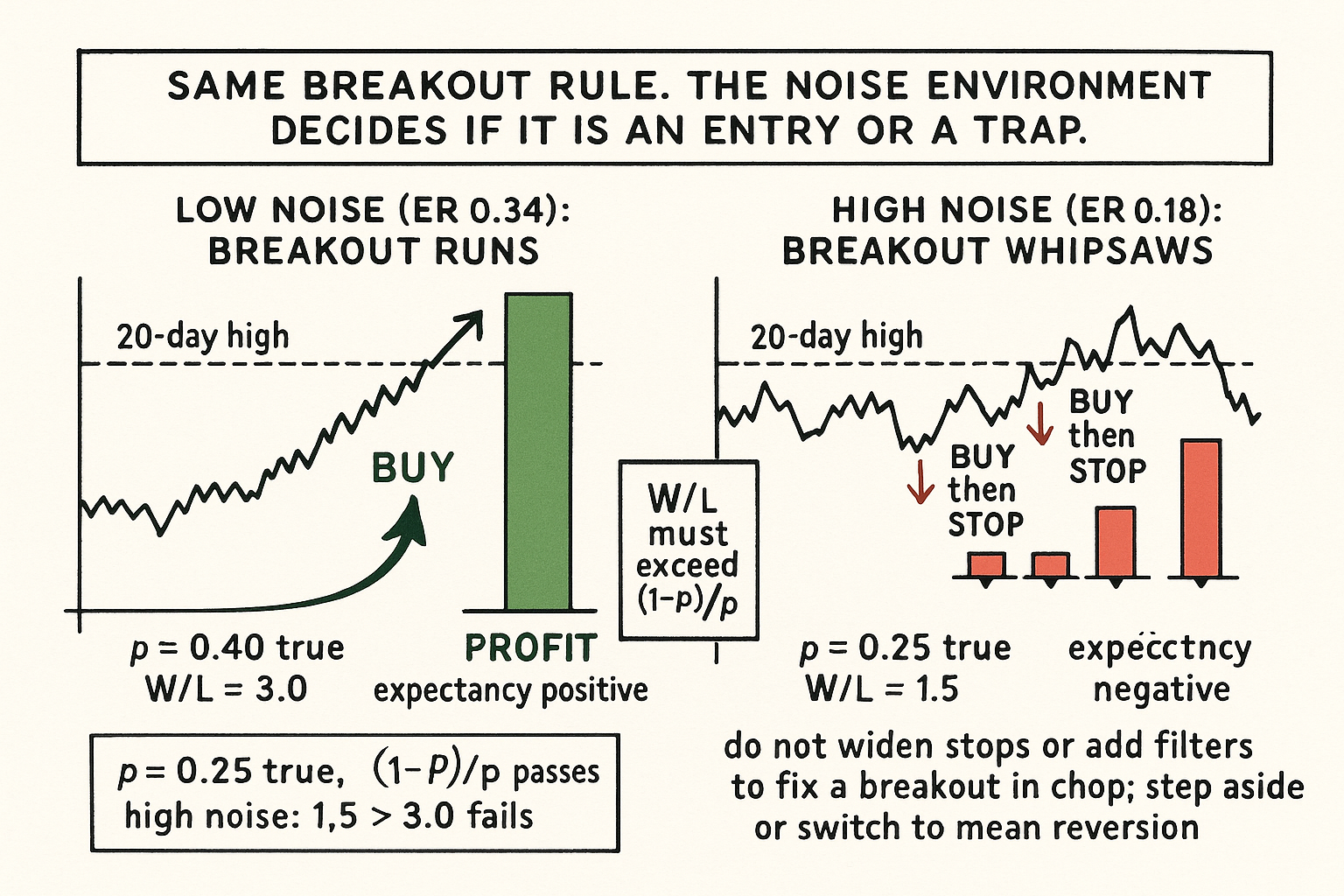

A breakout system has a low win rate by design (the trend-payoff asymmetry from "Low Noise Markets Are Trend-Following Markets": many small losers, few large winners). It survives only if the few winners are large enough to pay for the many losers. The noise level controls both the fraction of breakouts that are true and the size of the winners relative to the losers, so it controls whether the asymmetry closes.

Write the breakeven condition. Let p be the fraction of breakouts that are true (lead to a real move), the average winner be W, and the average loser (a false breakout cut at the stop) be L.

$$ E = p \cdot W - (1 - p) \cdot L > 0 \quad\Longleftrightarrow\quad \frac{W}{L} > \frac{1 - p}{p} $$

The expectancy E is positive only when the win-to-loss size ratio exceeds the loss-to-win odds ratio. In a low-noise market, p is higher (more breakouts are true) and W is larger (the true ones run further before reversing), so both sides of the inequality move in your favor. Suppose low noise gives p equal to 0.40 and a win-to-loss ratio of 3.0: the condition needs W over L above (1 minus 0.40) over 0.40, equal to 1.5, and 3.0 clears it comfortably. Now suppose high noise gives p equal to 0.25 and a win-to-loss ratio of 1.5 (winners are smaller because the market reverses sooner): the condition needs W over L above 0.75 over 0.25, equal to 3.0, and 1.5 fails it badly. The same breakout rule has positive expectancy in low noise and negative expectancy in high noise, and the efficiency ratio predicts which regime you are in before you trade.

Designing the breakout around the noise environment

If the breakout depends on low noise, the design follows: measure the noise, deploy the breakout only where the noise is low, and gate it dynamically when the noise rises. Three design rules.

Rule 1: select instruments by trend quality. The breakout belongs on the top of the trend-quality ranking from "How to Rank Markets by Trend Quality", the instruments with high median efficiency ratio and high persistence. Deploying a breakout on a bottom-ranked choppy instrument is a design error no parameter tuning fixes. The selection is the first and largest design decision.

Rule 2: gate entries on the rolling efficiency ratio. Even on a good instrument, the regime drifts. Disable or shrink breakout entries when the rolling efficiency ratio at the breakout horizon falls toward chop territory, the defensive gate from "Low Noise Markets Are Trend-Following Markets". This keeps the breakout out of the choppy patches where its expectancy is negative, paying the small cost of missing the occasional breakout that fires during a low-efficiency reading.

Rule 3: confirm the breakout with directional follow-through. From "The Difference Between Volatility Expansion and Directional Opportunity", a new high accompanied by a volatility expansion is not enough; require the post-breakout efficiency ratio or a close near the extreme to confirm direction before committing full size. This filters the violent-chop false breakouts (big bar through the high, immediate reversal) that pure price-level breakouts get trapped by.

These three are layers of the same idea: the breakout rule is fixed and cheap; the value is entirely in restricting it to the low-noise environments where its continuation premise holds.

The temptation to "fix" breakouts in noise, and why it fails

When a breakout system whipsaws in a choppy market, the tempting fixes all make it worse. Widening the stop to avoid whipsaws turns the many small losers into fewer large losers without adding winners, because the problem is that the extremes reverse, not that the stop is too tight. Adding confirmation filters until the whipsaws stop usually filters out the real breakouts too, because in a choppy market the real and false breakouts look the same on the way in. Shortening the lookback to catch moves earlier increases the signal count and the whipsaw count together. Every one of these is an attempt to make a continuation strategy work in a reversal environment, and they fail for the same reason: the environment, not the rule, is wrong. The article "The Difference Between Robustness and Optimization" warned that piling on parameters to rescue a strategy in a hostile regime is how you overfit; the breakout-in-chop case is the textbook example.

The correct response to a breakout that is whipsawing is not to fix the breakout. It is to recognize that the market has entered a high-noise regime and either step aside (the gate) or switch to the mean-reversion family that the high-noise regime favors (the family switch from "Why One Indicator Should Not Be Used on Every Market"). A whipsawing breakout is the market telling you it has changed regime, and the information is more valuable than the lost trade.

Decision summary

| Efficiency ratio at breakout horizon | True-breakout fraction | Action |

|---|---|---|

| Above 0.30 | High (most breakouts run) | Deploy breakout at full size, let winners run |

| 0.20 to 0.30 | Mixed | Breakout with directional confirmation, reduced size |

| Below 0.20 | Low (most breakouts reverse) | Disable breakout; switch to mean reversion |

The breakout rule is trivial and the environment is everything. Select low-noise instruments, gate on the rolling efficiency ratio, confirm with follow-through, and never try to optimize a breakout into a choppy market.

Visualizing the breakout's noise dependence

KEY POINTS

- A breakout signal is trivial; the price makes a new extreme or it does not. The noise environment the signal fires into decides whether it is an entry or a trap.

- A breakout is a direct bet that an extreme will be followed by continuation, which is the definition of low noise. A breakout in a high-noise market bets on continuation in a market defined by reversal.

- The whipsaw cost scales with noise. In high noise most extremes reverse, so most breakouts are false, and the system pays the whipsaw cost repeatedly while waiting for the rare runner.

- Breakouts have a low win rate by design and survive only if the few winners pay for the many losers. The breakeven needs the win-to-loss size ratio above the loss-to-win odds ratio.

- Low noise moves both sides of the inequality in your favor: more breakouts are true (higher p) and the true ones run further (larger W). The same rule has positive expectancy in low noise and negative in high noise.

- Worked example: low noise (p 0.40, W/L 3.0) clears the 1.5 hurdle; high noise (p 0.25, W/L 1.5) fails the 3.0 hurdle. The efficiency ratio predicts which regime before you trade.

- Three design rules: select instruments by trend quality, gate entries on the rolling efficiency ratio, and confirm breakouts with directional follow-through to filter violent-chop false signals.

- The tempting fixes (wider stops, more filters, shorter lookback) all fail because they try to make a continuation strategy work in a reversal environment. A whipsawing breakout means the regime changed; step aside or switch to mean reversion rather than optimizing the breakout into the chop.

- The next article, "Why Grid Systems Need Noise, Not Just Volatility", takes the opposite design case: the strategy family that needs exactly the high-noise environment a breakout cannot survive.

References

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Microstructure Evidence from the Polymarket Order Book - arXiv

- Identifying Noise Traders: The Head-And-Shoulders Pattern In U.S.

- Quantitative Analytics False Confidence in Systematic Trading

- MEME: Modeling the Evolutionary Modes of Financial Markets - arXiv

- Why Tokenised Securities Need Authoritative Market Records, Not

- Reframing Financial Markets as Complex Systems

- who sets the range? funding mechanics and 4h context in ... - arXiv

- MM-DREX: Multimodal-Driven Dynamic Routing of LLM Experts for

- Trading price jump clusters in foreign exchange markets

- Carry and Trend Following Returns in the Foreign Exchange Market

- A trend factor: Any economic gains from using information over investment horizons?

- Predictability in sovereign bond returns using technical trading rules: Do developed and emerging markets differ?

- Optimal trend-following with transaction costs

- The Complementarity of Trend Following and Relative Sentiment

- Non-random behavior in financial markets

- Liquidity-Driven Breakout Reliability: Why Price Moves Where

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.