4.9 The Difference Between Volatility Expansion and Directional Opportunity

Volatility expansion and directional opportunity look identical on an ATR chart but differ: motion can go somewhere or cancel out. Confirm with the efficiency ratio before trading.

A volatility breakout system fires when the daily range expands past a multiple of its recent average true range, on the theory that a volatility burst signals the start of a move. On a day when crude oil's range triples after a supply headline and the price closes near its high, the system enters and rides a clean directional follow-through. On a day when the SPX range triples after a confusing macro print and the price whipsaws violently but closes near its open, the same system enters and gets stopped out by the next reversal. Both days had identical volatility expansion. Only one had directional opportunity. The system that cannot tell them apart will take both trades and wonder why half its volatility-breakout signals fail.

This article separates two things that the word "volatility" routinely conflates and that the noise framework already gives us the tools to distinguish. The article "Noise Is Not Volatility" established that volatility (how far price moves) and noise (how much cancels out) are different axes. Volatility expansion is a change in the magnitude of motion. Directional opportunity is net displacement per unit of that motion. A market can expand its volatility without producing any net direction, and that combination, big motion with no displacement, is the most dangerous environment for a system that treats volatility as a signal.

Two different events that look the same on a volatility chart

Volatility expansion is a denominator event. It means the daily ranges got bigger, the price is covering more ground per bar, the average true range is rising. That is all it means. It says nothing about whether the ground covered is accumulating in a direction or canceling out. The article "Why Volatility Is More Non-Stationary Than Trend" documented how volatility clusters and spikes on its own clock; those spikes are denominator events, and they arrive in both trending and choppy regimes.

Directional opportunity is a numerator-over-denominator event. It means the net displacement is large relative to the path, the efficiency ratio is high, the motion is going somewhere. This is the thing a directional strategy can actually monetize. It can coincide with a volatility expansion (a violent trending breakout) or with low volatility (a quiet steady grind), because direction and magnitude are close to independent, the two-axis point from the noise article.

The confusion happens because the two events share a symptom: both can produce a large bar. A large bar in a trend is direction. A large bar in a chop is just a wide oscillation that will be reversed. The bar size cannot distinguish them, which is exactly why a volatility-magnitude signal alone is an incomplete trade trigger. You need the second axis, whether the expansion is converting to displacement, and that is the efficiency ratio or price density measured around the expansion.

The four combinations

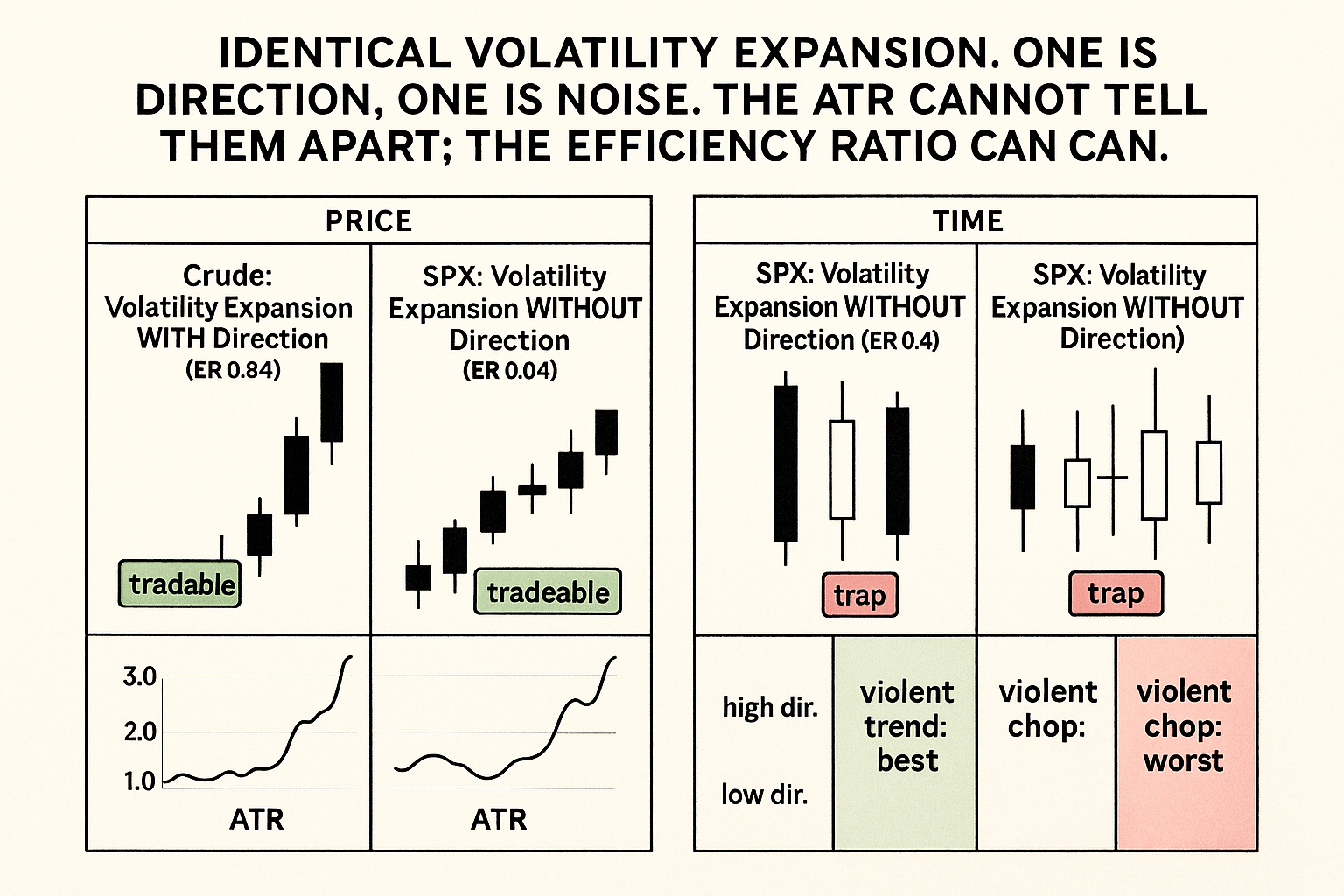

Cross volatility (expanding or contracting) with direction (high or low efficiency ratio) and you get four regimes, each demanding different handling. This is the two-by-two from "Noise Is Not Volatility" applied to the dynamic case, where volatility is changing rather than fixed.

| Low noise (directional) | High noise (no direction) | |

|---|---|---|

| Volatility expanding | Violent trend: best trend environment | Violent chop: worst environment, whipsaw |

| Volatility contracting | Quiet grind: trend with small size | Quiet range: classic fade environment |

The top-left, expanding volatility with direction, is the volatility-breakout system's dream: a real move with size behind it. The top-right, expanding volatility without direction, is its nightmare: maximum motion, zero displacement, every entry reversed. A system that triggers on volatility expansion alone takes both top cells and cannot tell which it is in until after the loss. The fix is to require a directional confirmation (a rising efficiency ratio, a close near the extreme, a follow-through bar) before treating a volatility expansion as a trade signal. Volatility expansion is a necessary condition for a violent trend and not a sufficient one.

A worked separation

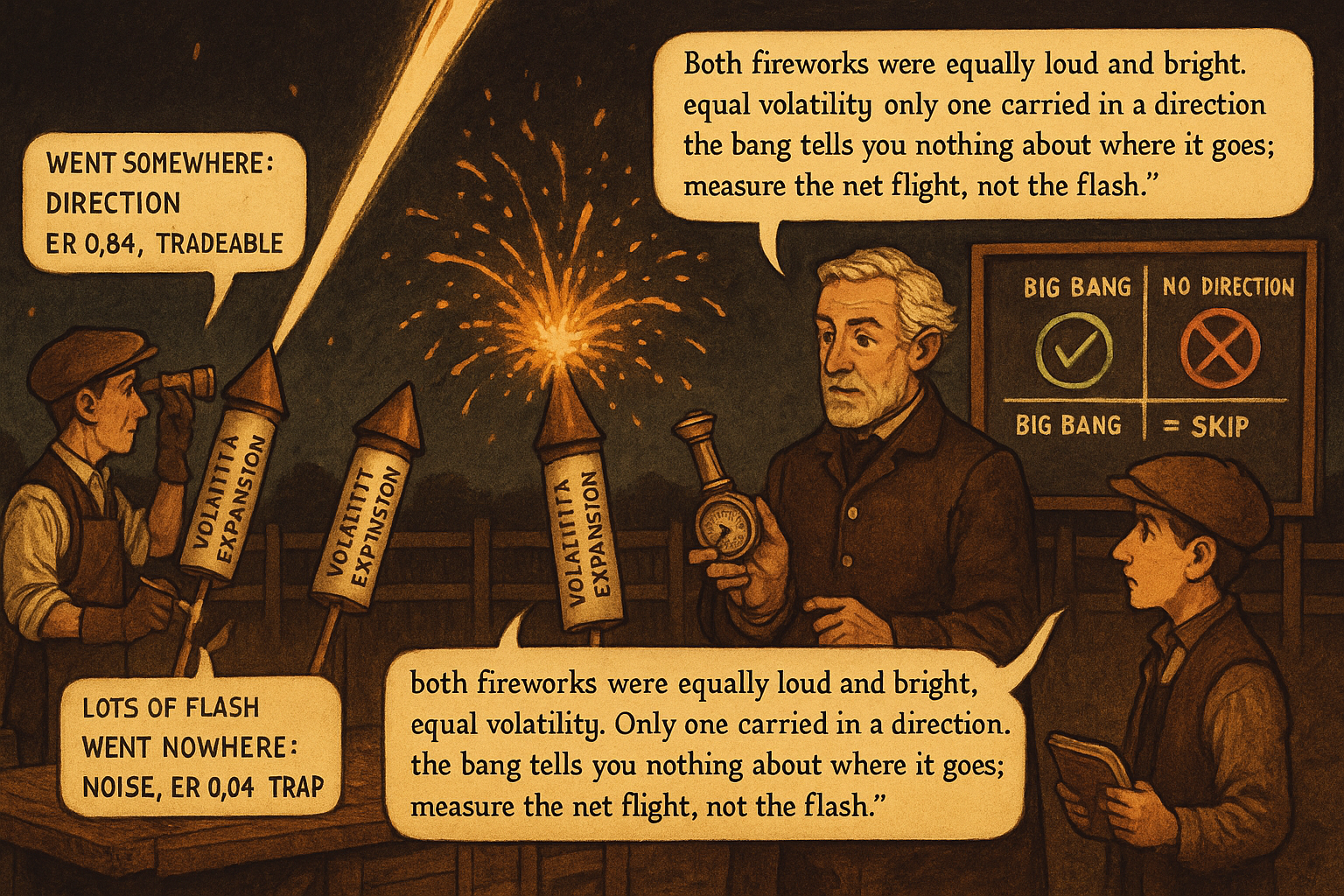

Quantify the two days from the opening. Both expand from an average true range of 1.0 to a range of 3.0 on the signal day, identical volatility expansion.

Crude oil day: the 3.0 range is covered mostly in one direction, the close is 2.7 above the open, and the next two bars add another 1.5 in the same direction. Measure the efficiency ratio over the three bars: net change about 4.2, total path about 5.0, efficiency ratio 0.84. High. This was directional opportunity wearing a volatility expansion.

SPX day: the 3.0 range is covered by a violent up-then-down whipsaw, the close is 0.2 above the open, and the next two bars oscillate another 4.0 of path while ending near where they started. Efficiency ratio over the three bars: net change about 0.3, total path about 7.0, efficiency ratio 0.04. Near zero. This was volatility expansion with no directional opportunity at all.

$$ \text{ER}_{\text{event}} = \frac{|P_{\text{end}} - P_{\text{start}}|}{\sum |P_i - P_{i-1}|} \quad\Rightarrow\quad \text{crude: } \frac{4.2}{5.0} = 0.84, \quad \text{SPX: } \frac{0.3}{7.0} = 0.04 $$

Same volatility expansion, an efficiency ratio of 0.84 versus 0.04 around the event. The efficiency ratio measured over the bars following the expansion is what separates the tradeable expansion from the trap. A volatility-breakout system that adds this filter, only act on an expansion if the immediate efficiency ratio confirms direction, takes the crude trade and skips the SPX trade, which is the entire difference between the strategy working and not.

Why this matters for sizing, not just entries

The distinction also breaks a common position-sizing error. Volatility-targeting sizing scales positions inversely to volatility, so it cuts size when volatility expands. That is correct for risk control and silent about opportunity. In the top-left cell (violent trend), cutting size because volatility expanded means under-betting the best directional opportunity available, the moment you most want exposure. In the top-right cell (violent chop), the volatility-targeting cut is appropriate because there is no opportunity to size into. Volatility targeting treats both cells identically, sizing down, when one deserves more conviction and the other deserves none.

The richer sizing rule conditions on both axes: size to volatility for risk, then tilt by the efficiency ratio for opportunity. When volatility expands with high directional confirmation, the volatility cut and the directional tilt partly offset, leaving meaningful exposure into the violent trend. When volatility expands with no directional confirmation, both the volatility cut and the absent tilt point the same way, toward little or no exposure. The article "Market Personality" listed vol-conditioned sizing as a fit for several families; the two-axis refinement is to condition on direction as well as magnitude, because magnitude alone mis-sizes the violent-trend cell.

The misdiagnosis this prevents

The error this article kills is "my volatility breakout system has a low win rate, so volatility breakouts do not work". Often the truth is that the system traded both top cells indiscriminately, won in the violent-trend cell, lost in the violent-chop cell, and the blended low win rate hid a strong conditional edge. Split the historical signals by the post-expansion efficiency ratio and the picture usually clarifies: the high-efficiency-ratio expansions were profitable, the low-efficiency-ratio expansions were the losers, and the strategy was never broken, it was unconditioned. This is the same stratification discipline the article "Regime Coverage: Why Your Backtest Needs Different Market States" applied to regimes, here applied to the volatility-direction split within the signal set.

The forward caveat is the usual one. The post-expansion efficiency ratio confirms direction only after a few bars have printed, which means the confirmation costs you the first part of the move. You trade a slightly later, more reliable entry for the earlier, noisier one. That trade-off is real and there is no free version: requiring directional confirmation reduces whipsaw and also reduces the captured move, and the right balance depends on the instrument's noise structure, which is why you measure the efficiency ratio per instrument rather than assuming.

Decision summary

| Volatility | Post-event efficiency ratio | Regime | Action |

|---|---|---|---|

| Expanding | High (above ~0.5 on the event) | Violent trend | Trade the breakout, tilt size up despite vol cut |

| Expanding | Low (below ~0.2 on the event) | Violent chop | Skip; volatility without direction is a trap |

| Contracting | High | Quiet grind | Trend with small size |

| Contracting | Low | Quiet range | Fade environment |

Volatility expansion is a necessary but not sufficient condition for a directional trade. Confirm with the efficiency ratio around the event before treating the expansion as a signal, and condition size on direction, not magnitude alone.

Visualizing the two events

KEY POINTS

- Volatility expansion (how far price moves per bar) and directional opportunity (net displacement per unit of motion) are different events that share a symptom: both can produce a large bar.

- A large bar in a trend is direction; a large bar in a chop is a wide oscillation that reverses. Bar size alone cannot distinguish them, which is why a volatility-magnitude signal is an incomplete trade trigger.

- Crossing volatility (expanding/contracting) with direction (high/low efficiency ratio) gives four regimes. Expanding volatility with direction is the violent trend (best for breakouts); expanding volatility without direction is the violent chop (worst, pure whipsaw).

- A system that triggers on volatility expansion alone takes both top cells and cannot tell which it is in until after the loss. Require directional confirmation (rising efficiency ratio, close near the extreme, follow-through) before treating an expansion as a signal.

- Worked example: two days expand identically from ATR 1.0 to range 3.0; the crude day reads efficiency ratio 0.84 over the following bars (direction), the SPX day reads 0.04 (no direction). The event-window efficiency ratio separates the tradeable expansion from the trap.

- Volatility-targeting sizing cuts size when volatility expands, which under-bets the violent-trend cell (the moment you most want exposure) and correctly cuts the violent-chop cell. It treats both identically. The fix: size to volatility for risk, then tilt by the efficiency ratio for opportunity.

- The misdiagnosis this prevents: "volatility breakouts do not work" usually means the signals were unconditioned, winning in the trend cell and losing in the chop cell, with the blend hiding a strong conditional edge. Split signals by post-expansion efficiency ratio to see it.

- Directional confirmation costs the first part of the move: a later, more reliable entry trades against an earlier, noisier one. The right balance depends on the instrument's noise structure, so measure it per instrument.

- The next article, "Why Breakout Systems Need Low Noise Environments", applies this directly to breakout design: why a breakout signal is only as good as the noise environment it fires into.

References

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- The Microstructure of Foreign Exchange Markets

- Lead-Lag Relationships in Market Microstructure⋆

- THE IMPACT OF FX CENTRAL BANK INTERVENTION IN A NOISE

- Price Movement Forecasting via Locality-Aware Attention and ... - arXiv

- Microstructure Evidence from the Polymarket Order Book - arXiv

- High-Frequency Trading, Asset Pricing, and Market Microstructure

- Identifying Noise Traders: The Head-And-Shoulders Pattern In U.S.

- Online learning of order flow and market impact with Bayesian

- A Framework for Predictive Directional Trading Based on Volatility-Driven Lead-Lag Relationships

- Move-Occurrence Predictability, Directional Efficiency, and Regime Clustering in High-Frequency Markets

- On the Correlation Structure of Microstructure Noise: A Financial Economic Approach

- Realized Variance and Market Microstructure Noise

- Local Mispricing and Microstructural Noise: A Parametric Perspective

- Testing if the Market Microstructure Noise is Fully Explained by the Observed Characteristics of the Trading Process

- Measuring Relative Volatility in High-Frequency Data Under the Directional Change Approach

- Incorporating Improved Directional Change and Regime Change Detection into FX Trading Strategies

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.