1.15 Induction in Trading: Why Past Patterns Are Always Uncertain

Every trading claim is induction: a pattern inferred from past data and projected forward. The conclusion is never certain. A 70% hit rate from 1000 signals carries sampling uncertainty plus the deeper uncertainty that the future may not be drawn from the same distribution as the past.

Every claim a trader makes about the future is inductive. The trader observes past data, infers a pattern, and projects the pattern forward. That structure is the definition of induction, and induction is the form of inference whose conclusions are never certain.

This is not a technical limitation of any specific method. It is a property of the type of reasoning involved. Even a perfect backtest, on a complete sample, with infinite computational power, produces a conclusion that holds only with some degree of probability and only if the future resembles the past in the relevant ways.

The trader who claims certainty has either misunderstood the logical structure of the claim or is selling something.

Deduction versus induction

Two forms of inference run through every analytical argument. They behave differently.

Deduction starts with a general premise and derives a specific conclusion. If the premises are true, the conclusion is necessarily true. The classic example: all men are mortal, Socrates is a man, therefore Socrates is mortal. The conclusion adds no new information beyond what the premises already contain. Deduction is certain but does not produce new knowledge about the world.

Induction starts with specific observations and infers a general claim. The conclusion extends beyond what the premises strictly justify. The classic example: every healthy dog observed so far had four legs, therefore all healthy dogs have four legs. The conclusion is plausible but not certain. The next dog might have three legs. Induction adds new information about the world but pays for it in uncertainty.

Trading runs almost entirely on induction. The chart pattern, the seasonality, the moving average crossover, the Sharpe-1.4 strategy backtested over 20 years: each is a generalization from a finite set of past observations to a claim about unobserved future cases. The premises are facts about history. The conclusions are bets about a future no one has seen yet.

The standard inductive argument in trading

The structure of a typical trading claim is induction by enumeration. The argument has two parts.

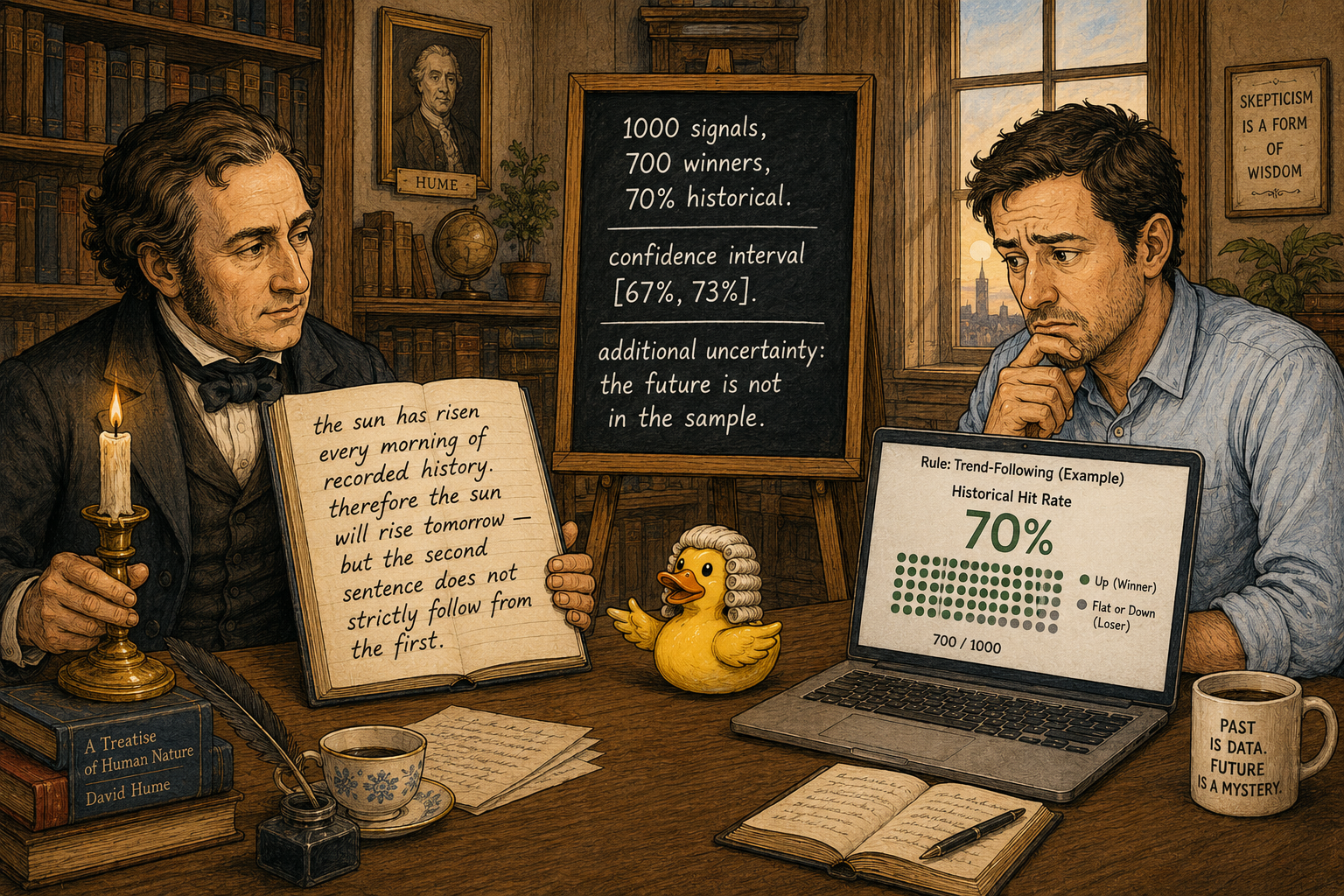

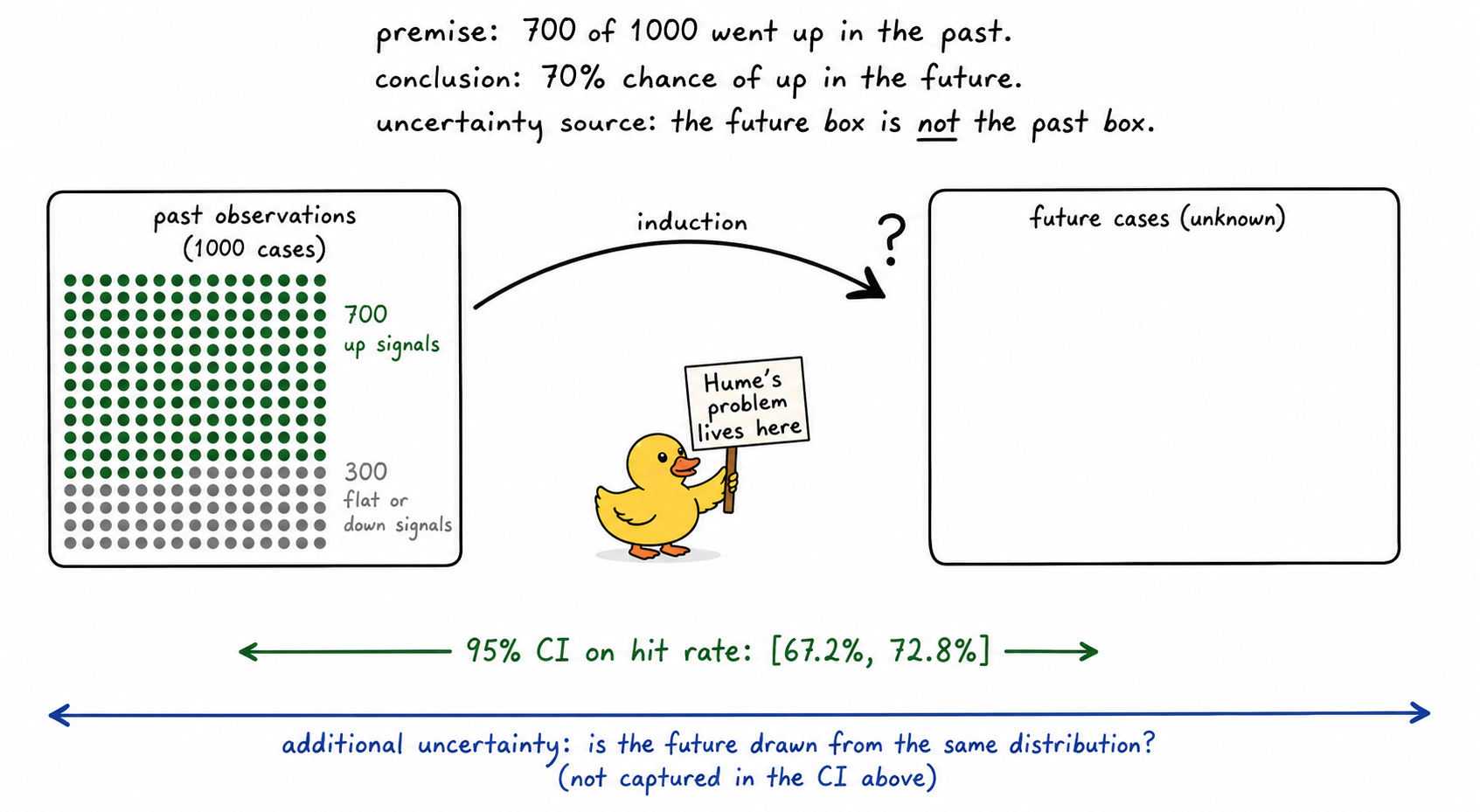

Premise: over the past 20 years, a specific rule fired 1000 times, and in 700 of those instances the market closed higher 10 days later.

Conclusion: in the future, when the rule fires, there is a 70% chance the market will close higher 10 days later.

The premise is true. The historical signals fired the number of times stated, and the historical hit rate is the number observed. The conclusion is uncertain. It extends a claim about 1000 past cases to an unknown number of future cases that have not yet been drawn.

The classical statistical machinery makes the uncertainty quantitative. The 95% confidence interval on the true hit rate, assuming the future is drawn from the same distribution as the past, is:

Where p̂ is the observed hit rate and N is the number of signals. For p̂ = 0.7 and N = 1000:

0.7 ± 1.96 × √(0.21/1000) = 0.7 ± 0.028 = [0.672, 0.728]

The interval says "with 95% confidence, the true hit rate is between 67.2% and 72.8% if the future is drawn from the same distribution as the past." That last clause is the catch. The interval captures sampling uncertainty. It does not capture the uncertainty about whether the same distribution still applies.

Hume's problem

The deeper uncertainty in induction is not statistical. It is logical.

To justify projecting past patterns into the future, the inductive reasoner has to assume that the future will resemble the past in the relevant ways. The standard name for this assumption is the uniformity of nature. Without it, no inductive conclusion follows.

The problem: there is no way to prove the uniformity of nature without using induction itself. Any argument that "the future has resembled the past in many cases, therefore the future will continue to resemble the past" is itself an inductive argument that depends on the very assumption being defended. The justification is circular.

This problem is not new and does not go away with more data or better methods. Every scientific field deals with it. Every scientific field accepts induction as the only way to make new claims about the world while accepting that the resulting claims are not certain.

What changes from field to field is how badly induction fails when the assumption breaks down. In physics, the uniformity of nature holds extremely well. In markets, it does not.

Two dimensions of inductive strength

Some inductive arguments are stronger than others. The strength depends on two factors.

Quantity. The more independent observations supporting the generalization, the tighter the confidence interval on the sample statistic. The binomial CI shrinks proportional to 1/√N. Going from 100 to 10,000 observations narrows the interval by a factor of 10. There is no exception to this in any well-behaved estimator.

Quality. The degree to which the observed cases are representative of the future cases the trader wants to predict. A rule tested only in low-volatility bull markets has bad quality evidence for high-volatility bear markets. A signal tested only on the SPX has bad quality evidence for emerging-market equities. The CI calculated from the sample does not capture this dimension. The CI assumes the sample is representative. When it is not, the CI is wrong in a direction that cannot be detected from the sample alone.

Quantity is easy to measure. Quality requires judgment about what the future will look like and which features of the past are relevant. Most retail induction is high-quantity and low-quality. The number of observations is large. The diversity of regimes those observations cover is small.

Visualizing the induction problem

The diagram shows the two layers of uncertainty. The narrow bar is sampling variability, which standard statistics handles. The wider bar is the inductive leap from past to future, which standard statistics cannot reach.

Why induction fails harder in trading than in physics

Three properties of markets weaken inductive inference relative to fields like physics.

Non-stationarity. The underlying data-generating process changes over time. The volatility regime that produced the 1990s data is not the regime that produced the 2008–2009 data, which is not the regime that produced the 2020 covid data. Each chunk of history is a sample from a different population. Pooling them increases nominal N but breaks the assumption that all observations come from the same distribution.

Active participants. When a pattern is published, traders act on it. The act of trading on the pattern changes the data-generating process. An edge that existed before publication may not exist after publication. This feedback is unique to social and financial systems and absent from physics.

One history. There is no second universe to replay. Even if the same data-generating process were running, the trader has only one realization to study. Article 14 covered this problem. It interacts with induction by making the quality dimension of inductive evidence harder to assess from the data alone.

The combined effect is that historical regularities in markets carry less inductive weight than historical regularities in repeatable, stationary, participant-independent domains. Trading is the hard mode of induction.

The hypothetico-deductive method

Science deals with the problem of induction by combining inductive observation with deductive testing.

The five-stage process:

- Observation. Notice a pattern in the data. This step is inductive.

- Hypothesis. State the pattern as a precise, falsifiable claim about the world. This step is creative.

- Deductive prediction. Derive a specific testable consequence of the hypothesis. If the hypothesis is true, this consequence must hold.

- Test. Compare the prediction to new evidence. The new evidence either supports or contradicts the prediction.

- Conclusion. If the prediction holds, the hypothesis survives this round. If the prediction fails, the hypothesis is rejected.

The method does not make induction certain. It makes inductive hypotheses falsifiable. A hypothesis that survives many rigorous tests is more credible than one that has survived none. A hypothesis that fails any rigorous test is rejected. The process accumulates evidence without ever achieving certainty.

For trading, the hypothetico-deductive method is the same machinery covered in earlier articles: state the rule, define a null hypothesis, run a test, get a p-value or confidence interval, decide. The framework treats every trading claim as a falsifiable hypothesis whose acceptance is provisional and revisable.

Practical implications

The point of recognizing induction's structure is not to abandon induction. There is no alternative. The point is to handle inductive conclusions with the appropriate level of confidence.

Treat point estimates as midpoints of intervals. A backtested hit rate of 70% with 1000 observations is not "the strategy has a 70% hit rate." It is "the strategy had a 70% hit rate on this sample, and the true rate, conditional on the future resembling the past, sits somewhere between 67% and 73%."

Build inductive arguments with multiple kinds of evidence. Cross-section across instruments, cross-period across decades, synthetic data via simulation. Each is an independent inductive argument. Conclusions supported by all of them are stronger than conclusions supported by one.

Watch for regime shifts in live trading. The strongest inductive argument can be invalidated by a structural change. Position sizing and drawdown controls protect against the case where the underlying distribution has moved and the historical data no longer applies.

Be ready to abandon hypotheses on evidence. The defining feature of a scientific (versus dogmatic) inductive belief is willingness to revise it when the data demands. A trader who refuses to update beliefs in light of contradicting evidence is no longer doing induction. They are doing decoration.

KEY POINTS

- Every claim a trader makes about the future is inductive. The trader observes past data, infers a generalization, and projects it forward.

- Induction's conclusions are inherently uncertain because they extend beyond what the premises strictly justify. This is true even with perfect data and infinite computation.

- The standard trading argument is induction by enumeration: "rule fired 1000 times, 700 went up, therefore 70% hit rate going forward." The premise is true. The conclusion is uncertain.

- The 95% confidence interval on a 70% sample hit rate from 1000 observations is roughly [67.2%, 72.8%]. This captures sampling uncertainty under the assumption that the future is drawn from the same distribution as the past.

- The deeper uncertainty (the assumption itself) is Hume's problem. The uniformity of nature cannot be proven without circular reasoning. Every scientific field accepts this.

- Two factors govern inductive strength: quantity (more observations tighten the sampling CI) and quality (how representative the observations are of future cases). The CI captures quantity. Quality requires separate judgment about regime coverage.

- Markets weaken induction more than physics does. Non-stationarity shifts the underlying distribution. Active participants change the process when patterns are published. One realized history limits quality evidence.

- The hypothetico-deductive method handles induction by combining inductive observation with deductive, falsifiable tests. It does not make conclusions certain. It makes them revisable in light of evidence.

- Practical response: treat point estimates as interval midpoints, use multiple kinds of evidence, watch for regime shifts, abandon hypotheses when data demands.

References

- Evidence-Based Technical Analysis - David Aronson (Amazon)

- Systematic Trading - Robert Carver (Amazon)

- Evidence-Based Technical Analysis: Applying the Scientific Method and Statistical Inference to Trading Signals

- Comparing Discretionary and Systematic Hedge Fund Performance

- Systematic Funds Outperform Discretionary Funds

- Traditional Traders vs. Quant Traders: A Comparative Analysis of Effectiveness, Risk-Adjusted Returns, and Market Interactions

- A Comprehensive Review of Statistical Methods in Quantitative Finance

- The Power of Price Action Reading

- Increase Alpha: Performance and Risk of an AI-Driven Trading Strategy with Dynamic Holding Periods

- 1 Hypothesis Testing Ordinary Meaning Daniel Keller – Northern