4.60 The FX Clock: Sessions, Overlaps, and Fixes

FX runs on a clock set by who's at their desk and which forced orders fire when. The London-NY overlap is cheapest; the fixes are scheduled traps. Trade the session, not the chart.

A EURUSD chart looks like one continuous market. It is not. The same pair costs you a different spread at 03:00 GMT than it does at 14:00 GMT, prints fake volatility when Tokyo is the only desk awake, and lurches on a schedule that has nothing to do with anything you would find on a chart. The price runs on a clock, and the clock is set by which humans are at their desks and which mechanical orders are forced through at fixed times. Trade without knowing where you are on that clock and you pay the spread of a thin hour to capture an edge you only measured in a thick one.

The clock has two kinds of marks on it: sessions, which are slow tidal shifts in who is trading, and fixes, which are sharp spikes of forced flow at exact minutes. They matter for opposite reasons. Sessions decide your baseline cost and how much of a candle is signal versus noise. Fixes decide when you should not be holding a fresh position into a wall of price-insensitive orders.

The three desks and the one window that matters

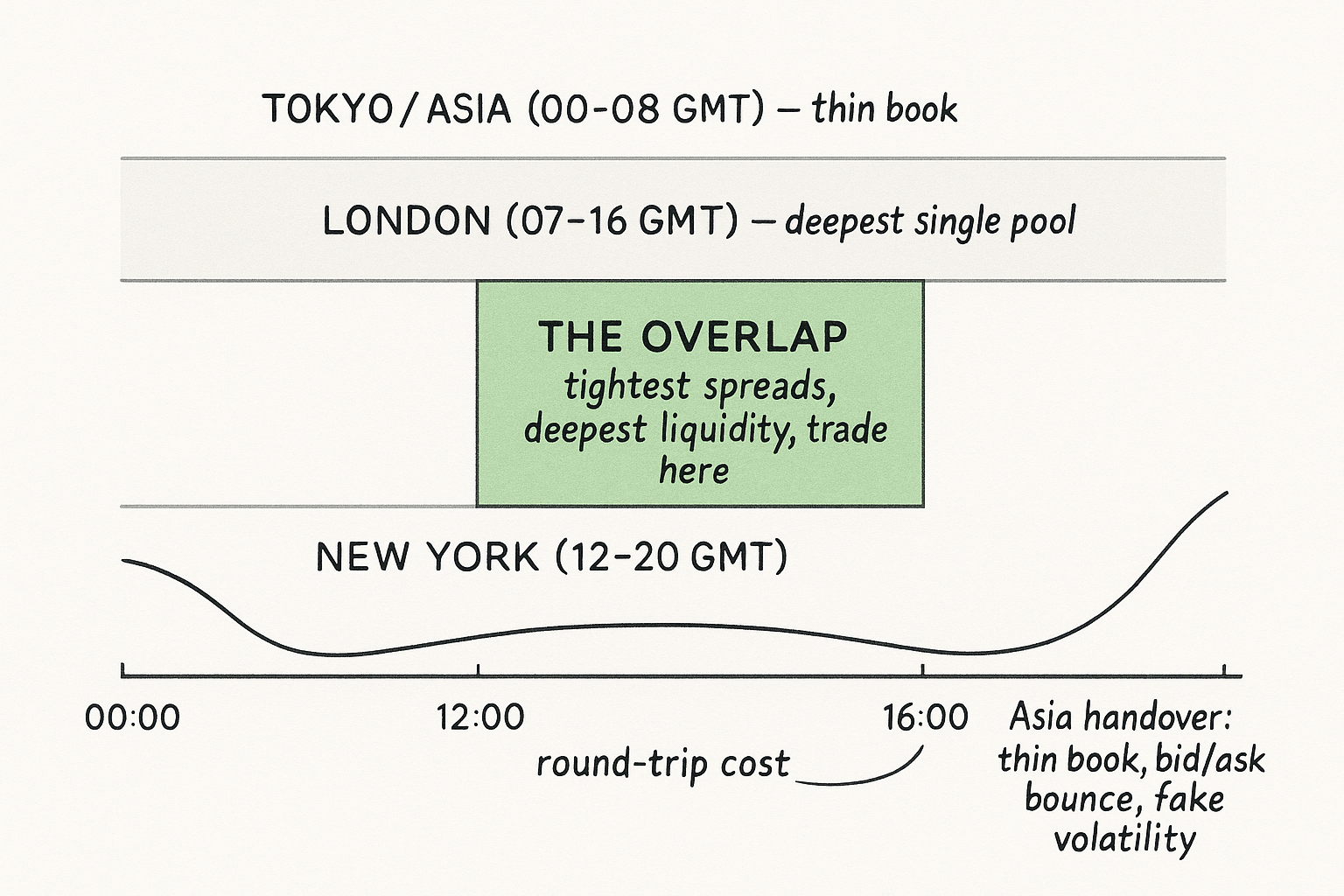

Liquidity in FX is a relay race between three regional hubs. Asia (Tokyo, then later China and Singapore) runs the overnight book, thin and prone to air pockets. London opens at 07:00 GMT and is the largest single pool of FX turnover on the planet. New York opens around 12:00 GMT and overlaps London until London winds down in the late afternoon. The window where both London and New York are live, roughly 12:00 to 16:00 GMT, is where the deepest book and the tightest spreads sit. The book is deepest precisely when the two biggest desks are both quoting.

That overlap is the only part of the day a price-taker should treat as cheap. Everything outside it costs more, and the further you drift toward the Asia handover the worse it gets. The reason is mechanical, not mystical: spread and market impact both scale inversely with the depth of resting liquidity, and depth is just a headcount of who is quoting.

$$ \text{round-trip cost} \;\approx\; \text{spread} \;+\; k\,\frac{Q}{L} $$

Read it plainly. Your cost to get in and out is the quoted spread plus an impact term, where Q is your order size, L is the resting liquidity available at the top of the book, and k is a constant that depends on the pair. When London and New York are both on, L is large, so the same order Q barely moves the price and the spread term is small too. Drag the same trade into the Asia handover and L collapses, so both terms inflate and an edge that looked real at 14:00 GMT quietly evaporates at 23:00 GMT. This is the same machinery the old article "TWAP and VWAP Are Execution Models, Not Just Indicators" leaned on: you slice a large order into the thick part of the day because that is where L is biggest and your footprint is smallest.

The Asia book deserves its own warning. Thin liquidity does not just widen the spread, it manufactures motion. The old article "Why Bid/Ask Bounce Matters for Intraday FX Systems" showed how alternating buyer and seller prints make a spread-sized move every tick with no information behind it. That effect is worst exactly where the book is thinnest, so overnight candles carry the most bounce per unit of real movement. A volatility reading or an indicator crossing computed on the Asia session is mostly microstructure artifact, and any intraday system that does not condition on the session is averaging a clean overlap regime together with a junk overnight one.

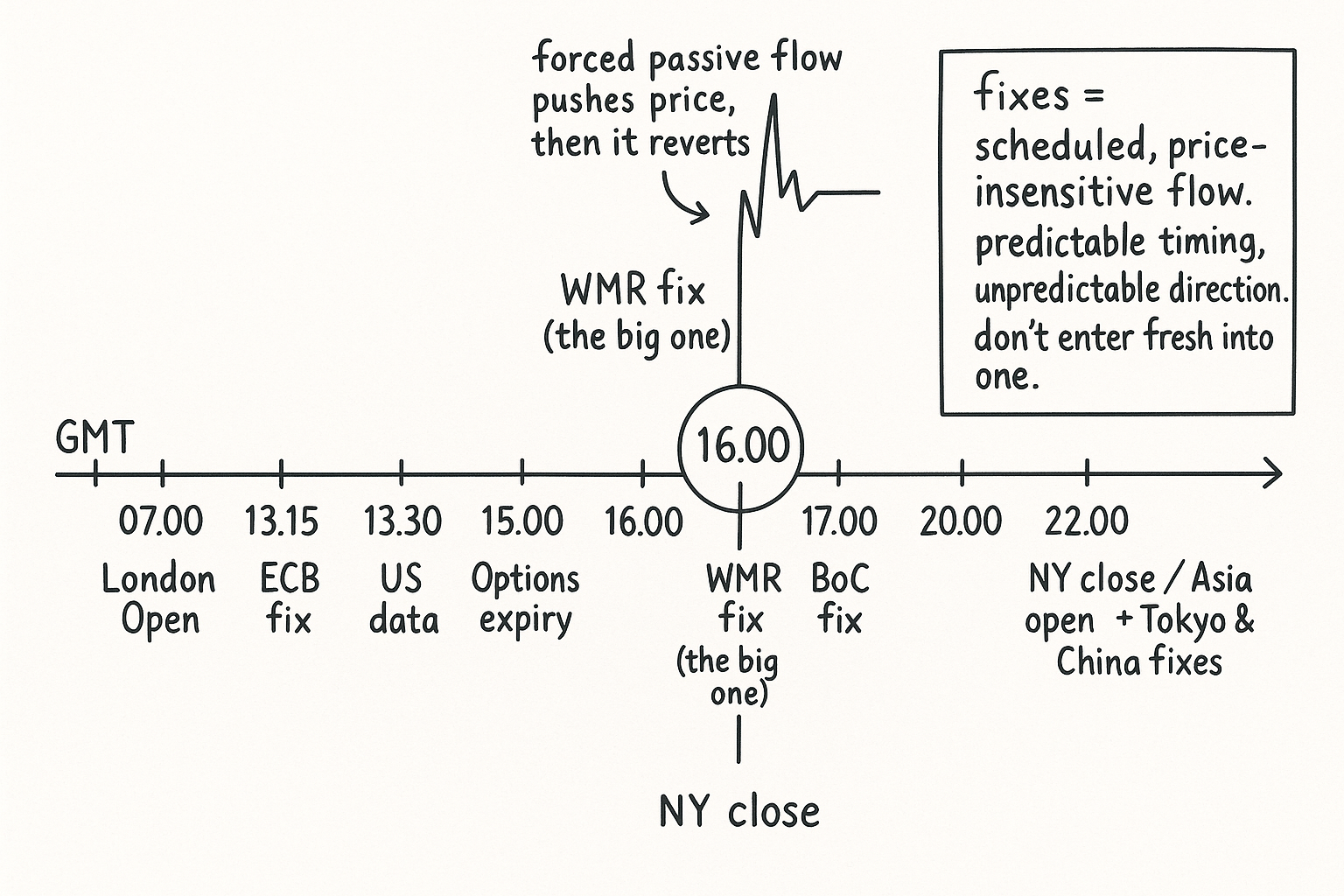

The fixes: scheduled walls of price-insensitive flow

A fix is a benchmark price struck at a fixed time, and around that time a crowd of orders that do not care about price gets pushed through to be filled at the benchmark. Index funds, corporates hedging cash flows, and option desks all reference these marks, so the flow is large, one-sided, and indifferent to where the price already is. That combination produces a short, sharp distortion that mean-reverts once the forced orders clear. The fix is not a trade signal. It is a hazard you schedule around.

The ones that move the G10 book, in GMT order through the European-into-New-York day:

- ECB fix, 13:15 GMT. The European Central Bank reference rate. Matters most for EUR crosses.

- US economic data, 13:30 GMT. Not a fix, but the heaviest scheduled news slot of the day. Payrolls, CPI, and the rest land here and the overlap is liquid enough to absorb the reaction.

- Options expiry and second-tier data, ~15:00 GMT. Large option strikes expiring pin or repel the spot price as dealers hedge their books into the cut.

- WMR benchmark fix, 16:00 GMT. The 4pm London WM/Reuters fix is the single most important mark in FX. Vast passive flows reference it, so the minutes around 16:00 GMT routinely show a sharp directional push that reverses afterward.

- Bank of Canada noon fix, ~17:00 GMT. A CAD-specific mark.

- Tokyo and China fixes, around the 22:00 GMT Asia open / NY close handover. The marks that govern the JPY and CNY books as the day rolls back to Asia.

The WMR 16:00 GMT fix is the one that catches systematic traders out. It sits at the tail end of the overlap, the book is still deep enough to look safe, and then a wave of passive month-end or index rebalancing flow shoves the price in one direction for a few minutes before it snaps back. A momentum system that reads the push as a breakout buys the top of a move that was never about value. A mean-reversion system can sometimes fade it, but only if it has sized for the fact that the reversal arrives on no fixed timetable.

The practical rule is the same across all of them: know the fix calendar in GMT, and do not let an entry signal fire you into a fresh position in the minutes straddling a major fix unless your strategy is explicitly built to trade that flow. The fixes are predictable in timing and unpredictable in direction, which is the worst combination to be surprised by.

How to actually use the clock

Treat the session as a regime label on every bar before you compute anything. Tag each timestamp as Asia, London-only, the overlap, or New York-only, and let your backtest report performance per session instead of blending them. Most intraday FX edges live in the overlap and die in Asia, and a single aggregate number hides that. If a signal only works in the overlap, that is fine, but you need to see it so you do not trade it overnight where the cost term and the bounce eat the edge.

Schedule execution, not just signals. If you have a large order, the old TWAP and VWAP logic says push the bulk of it through the overlap where L is largest. If your signal fires in the Asia session, the honest options are to widen your cost assumptions, wait for London, or skip it.

Put the fix calendar in your code as a hard filter. A simple no-trade buffer of a few minutes on either side of the WMR, ECB, and Asia fixes removes a class of losses that has nothing to do with whether your idea is right. You are not predicting the fix, you are declining to be standing in front of it.

The clock does not give you an edge by itself. It tells you when the edge you already have is cheap to harvest and when it is a trap dressed as a candle.

KEY POINTS

- FX is not one continuous market. It is a relay between Tokyo, London, and New York, and the London-New York overlap (roughly 12:00 to 16:00 GMT) is the deepest book and cheapest spread of the day.

- Round-trip cost is spread plus an impact term that scales as order size over resting liquidity. Liquidity is largest in the overlap and collapses into the Asia handover, so the same trade costs far more overnight.

- The thin Asia book manufactures fake movement through the bid/ask bounce covered in the old article "Why Bid/Ask Bounce Matters for Intraday FX Systems," so volatility and indicator readings on overnight candles are mostly artifact.

- Fixes (ECB 13:15, options expiry ~15:00, WMR 16:00, BoC 17:00, Tokyo/China around 22:00 GMT) are scheduled walls of price-insensitive flow with predictable timing and unpredictable direction. The 16:00 WMR fix is the one that traps systematic traders.

- Tag every bar with its session and report backtest performance per session, push large orders through the overlap as in the old article "TWAP and VWAP Are Execution Models, Not Just Indicators," and hard-code a no-trade buffer around the major fixes.

References

- The Art of Currency Trading - Brent Donnelly (Amazon)

- WM/Reuters benchmark fix (Wikipedia)

- Foreign exchange market trading sessions (BIS Triennial Survey)

- The 4pm London fix and FX market manipulation (Bank for International Settlements)

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- Intraday Seasonality in Activities of the Foreign Exchange Markets

- Trading Patterns and Prices in the Interbank Foreign Exchange Market

- Intraday Seasonality in Activities of the Foreign Exchange Markets

- Informativeness of Trades Around Macroeconomic Announcements in the Foreign Exchange Market

- Macroeconomic Announcement and Price Discovery in the Foreign Exchange Market

- Liquidity in the Global Currency Market

- Do Reuters Spreads Reflect Currencies’ Differences in Global Trading Activity?

- Foreign Exchange Liquidity in the Americas (BIS Papers No 90)