4.59 The Volatility–Liquidity Tradeoff in FX

Volatility and liquidity run inverse in FX: the moves you want come with the thin books you don't, and liquidity vanishes the instant volatility spikes. Defend with volatility-normalized sizing and a hard default to the liquid majors.

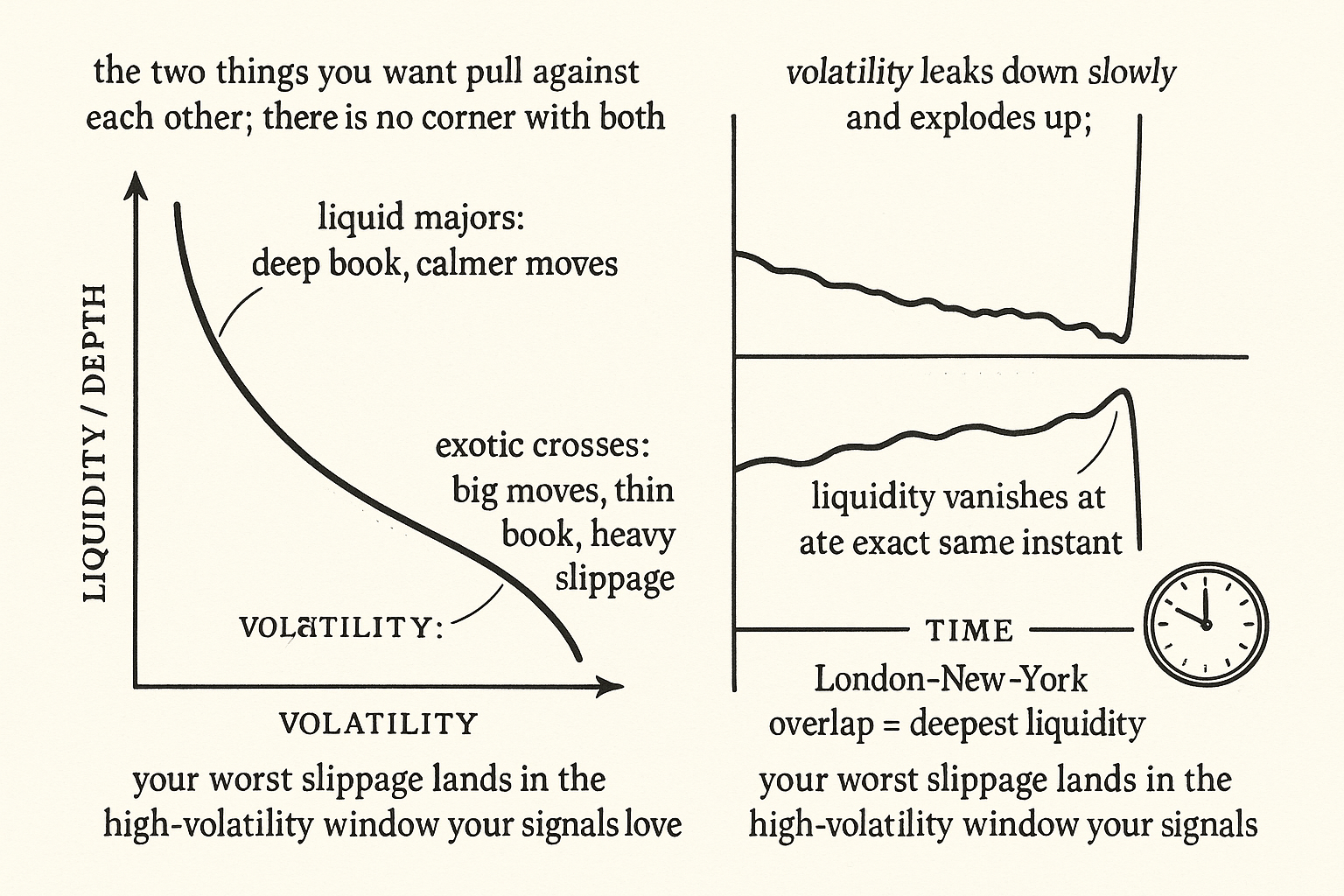

The two things a trader wants from a market pull against each other. You want volatility, because volatility is the movement your edge feeds on; a dead-flat currency offers nothing to capture. You want liquidity, because liquidity is what lets you get in and out without paying for the privilege; a thin currency charges you a fortune in slippage to take a position. In FX these two run inverse to each other. The pairs and the moments with the most movement have the least depth, and the pairs and moments with the most depth have the least movement. There is no corner of the market that hands you both at once, and the trader's job is to choose where on the tradeoff to sit rather than to pretend the corner exists.

This matters because the inverse relationship is not a static feature you can calibrate once. Both volatility and liquidity move over time and across regimes, and they move together in the worst way: when volatility spikes, liquidity evaporates in the same instant, so the cost of trading explodes exactly when your signals are firing hardest. A system that measures volatility and liquidity in a calm sample and assumes those numbers hold is mispricing its own execution in the only environment that decides whether it survives. This article works the tradeoff, the regime dependence, and the two defenses that follow: volatility-normalized sizing and a strong default toward the liquid majors.

The inverse relationship

Volatility measures how hard a price moves, computed from historical data, and higher volatility means higher risk by construction. Liquidity is harder to pin down but amounts to how much slippage you eat when you transact, and it tracks volume closely; high-volume currencies carry deep books and small slippage. The cleanest statement of the cost side is that expected slippage scales with the size you push through divided by the depth available to absorb it.

$$ \text{expected slippage} \;\approx\; \frac{\text{order size}}{\text{available depth}}, \qquad \text{and depth falls as volatility rises} $$

Slippage is roughly your order size over the depth in the book, the cost framing from the old article "The Real Heart of FX Liquidity." The tradeoff lives in the second clause: depth is not constant, it shrinks as volatility rises. Market makers widen spreads and pull size when the price is moving fast, because quoting tight in a fast market is how they get run over. So the denominator collapses precisely when volatility, the thing in your numerator's interest, is highest. A fixed-size order suffers its worst slippage in the high-volatility window, which is the window a mid-price backtest quietly assumes away by filling you at the midpoint in any size.

The best currencies to trade are the ones with both high liquidity and high volatility, and the reason that phrase contains a "tradeoff" is that the two rarely coexist. You pick liquid majors and accept calmer movement, or you chase the movement in thinner crosses and pay for it in slippage. Pretending you can have deep books and big clean moves in the same instrument is the assumption that kills small per-trade edges.

It changes by regime

Neither side of the tradeoff sits still. All historical measures of volatility are backward-looking, and the future can differ sharply from the past, so a volatility number is a statement about yesterday, not a guarantee about tomorrow. FX volatility tends to move in sync with global asset-market volatility, though not always; there are stretches where equities are wild and FX is calm, and the reverse. The characteristic shape is the dangerous part: volatility drifts lower in slow motion during calm regimes, then skyrockets when a disturbance hits. It leaks down and explodes up.

That asymmetry is why you cannot get comfortable in one environment. A system tuned to the slow calm drift, sized and costed for the depth available in that regime, meets a volatility spike that arrives in a single session and finds its execution assumptions inverted: wider spreads, thinner books, larger slippage, all at once. The instruction that follows is to stay alert to changes in market microstructure so that when the regime shifts you are already positioned for it rather than discovering it through fills. The same regime non-stationarity runs through every relationship in this pillar, the acceptance that systems work until they don't.

Liquidity also varies by pair and by clock

The tradeoff has a cross-sectional version and an intraday version on top of the regime version. Cross-sectionally, liquidity concentrates in the major pairs and thins out in the exotics, which are jumpy and expensive to trade in size. Intraday, liquidity follows the clock: the overlap of the London and New York sessions is the deepest window by a wide margin, because the two largest trading hubs are both open and the major events, US economic data, options expiries, and the benchmark fixes, cluster in that period. The thin Asian hours carry wider spreads and shallower books, so the same order costs more and moves the market more outside the overlap.

For a system this means execution quality is a function of which pair and which hour, not a constant. A signal that fires in the liquid majors during the London–New York overlap is cheap to act on; the same signal in an exotic cross during thin Asian hours can cost several times as much to fill, enough to flip a positive expected edge negative. Defaulting to the liquid pairs and the deep hours is not timidity, it is refusing to donate the edge to slippage.

The two defenses

The first defense is volatility-normalized sizing. Scale each position inversely to the instrument's volatility so that a wild pair gets a small position and a calm pair gets a larger one, equalizing the risk each contributes, the discipline from the old article "Why Volatility-Adjusted Position Sizing Matters."

$$ \text{position size} \;=\; \frac{\text{risk target} \times \text{capital}}{\sigma_{\text{instrument}}} $$

The position is the risk you are willing to take times your capital, divided by the instrument's volatility, so doubling the volatility halves the size and the dollar risk stays put. This is what lets a thin, volatile cross and a deep, calm major sit in the same book without the volatile one dominating the P&L. The catch, the same one the sizing article and the carry article flagged, is that volatility is estimated and lags, so when it jumps you are briefly oversized into the spike, which is the same moment liquidity has vanished. Faster estimators and floors soften it; nothing removes it.

The second defense is the default that most traders should hold to the liquid majors, the G10. The thin pairs offer more apparent movement, but the slippage and the gap risk in their low-liquidity windows take back more than the extra movement gives, especially for anything trading at higher frequency where the cost is paid often. The honest version of "trade where the edge is" in FX is "trade where the edge survives execution," and for most strategies that is the deep, liquid pairs in the deep, liquid hours, sized by volatility, with the acceptance that the calm you measured can skyrocket without notice.

Visualizing the tradeoff

KEY POINTS

- Volatility (the movement your edge feeds on) and liquidity (the depth that keeps slippage small) run inverse to each other in FX. No instrument or moment hands you both at once.

- Expected slippage is roughly order size over available depth, and depth shrinks as volatility rises, so a fixed-size order suffers its worst slippage in exactly the high-volatility window a mid-price backtest assumes away.

- Both sides move by regime. Volatility is backward-looking, tends to track global asset volatility, and drifts down slowly then skyrockets, so calm-regime execution assumptions invert in a single session when a disturbance hits.

- Liquidity varies cross-sectionally (concentrated in majors, thin and jumpy in exotics) and intraday (deepest in the London–New York overlap, thin in Asian hours), so execution quality depends on which pair and which hour, not a constant.

- The same signal can be cheap to fill in a liquid major during the overlap and expensive enough in a thin cross during Asian hours to flip its expected edge negative.

- First defense: volatility-normalized sizing, position equal to risk target times capital over instrument volatility, so a wild pair gets a small position. The catch is that volatility lags, so you are briefly oversized into a spike when liquidity has vanished.

- Second defense: default to the liquid majors in the deep hours. The extra movement in thin pairs is taken back by slippage and gap risk, so "trade where the edge survives execution" beats "trade where the movement is."

References

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- The Microstructure of Foreign Exchange Markets

- Foreign Exchange Volume: Sound and Fury Signifying Nothing?

- Order Flow and Exchange Rate Co-movement

- High-Frequency Trading, Asset Pricing, and Market Microstructure

- Liquidity in the Global Currency Market

- Market Microstructure Noise and Liquidity

- Constrained Liquidity Provision in Currency Markets

- Fixed versus Flexible: Lessons from EMS Order Flow

- Trades Outside the Quotes: Reporting Delay, Trading Option, or Trade Through?

- Hidden Liquidity, Displayed Depth, and Execution Risk During a Limit Order Book Regime Change

- Central bank intervention and the intraday process of price formation

- Order flow, dealer profitability, and price formation - ScienceDirect