4.26 The Real Heart of FX Liquidity

FX liquidity lives on a few primary interbank venues; every other price is a thinner copy. It runs inverse to volatility, so slippage is worst exactly when your breakout fires.

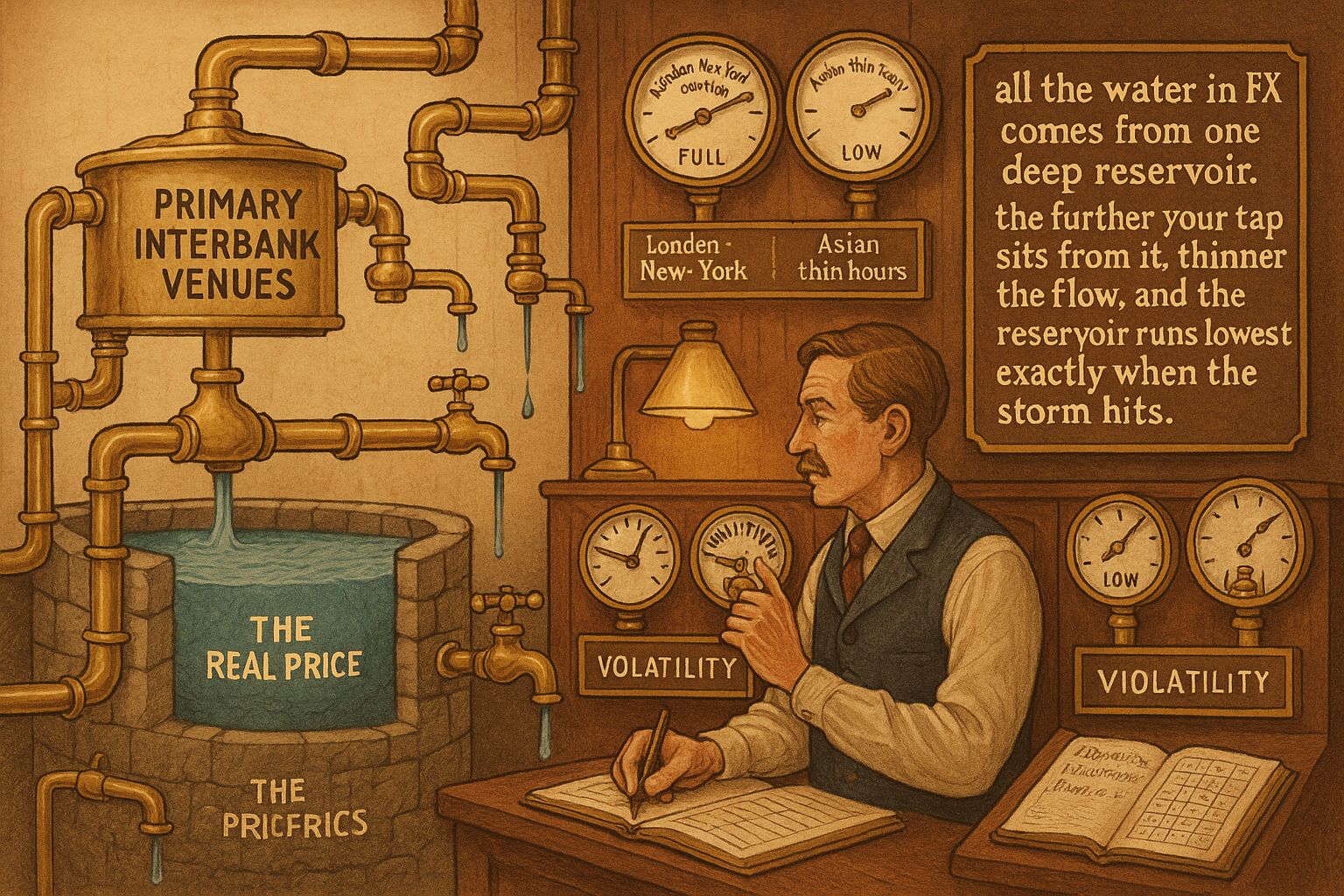

The price of EURUSD is not set in a retail app, on a charting platform, or in a data vendor's feed. It is set on a small number of primary interbank electronic venues where banks trade with each other, and historically two of them carried most of the flow: one that became the home of EUR and JPY liquidity, and another that anchored GBP, commodity, and emerging-market pairs. Every other price in the FX world (the retail quote, the broker feed, the platform chart) is a derivative of what happens on those primary venues. When a system trader talks about "the market," in FX that means these venues, and everything else is a copy with a delay and a markup.

Liquidity is the depth and tightness available to transact, and in FX it is concentrated at the wholesale tier and thins out as you move away from it. A retail trader's liquidity is whatever the broker chooses to show, sourced from the primary venues and reshaped. Understanding where the real liquidity lives, and how it changes by pair, by time of day, and by regime, is what separates a system that executes at the prices it assumed from one that bleeds slippage it never modeled.

This article locates the source of FX liquidity and the rules it follows. It continues from "FX Is Not One Market: Retail vs Wholesale Structure", which established the two tiers, and it underpins the execution choices in "Market Orders vs Limit Orders in FX" and "Why Bid/Ask Bounce Matters for Intraday FX Systems".

Where the price is made

The heart of the FX market is a handful of primary electronic communication networks, the venues where interbank dealers post and take two-sided prices. These are the primary markets, the place price discovery actually happens. A second ring of smaller venues has grown over time, but the primary venues remain the reference, and the price on every downstream screen is sourced from them.

This matters for a system builder because it locates the real bid and offer. The tightest, deepest, most reliable price for a major pair is on the primary venue, and that price is the benchmark against which your execution should be measured. If your retail fills are consistently worse than the primary-venue mid by more than the expected spread and markup, you are paying for something (latency, last look, a wide B-book quote) that your backtest did not include, the tier gap the previous article made central.

Liquidity is not constant

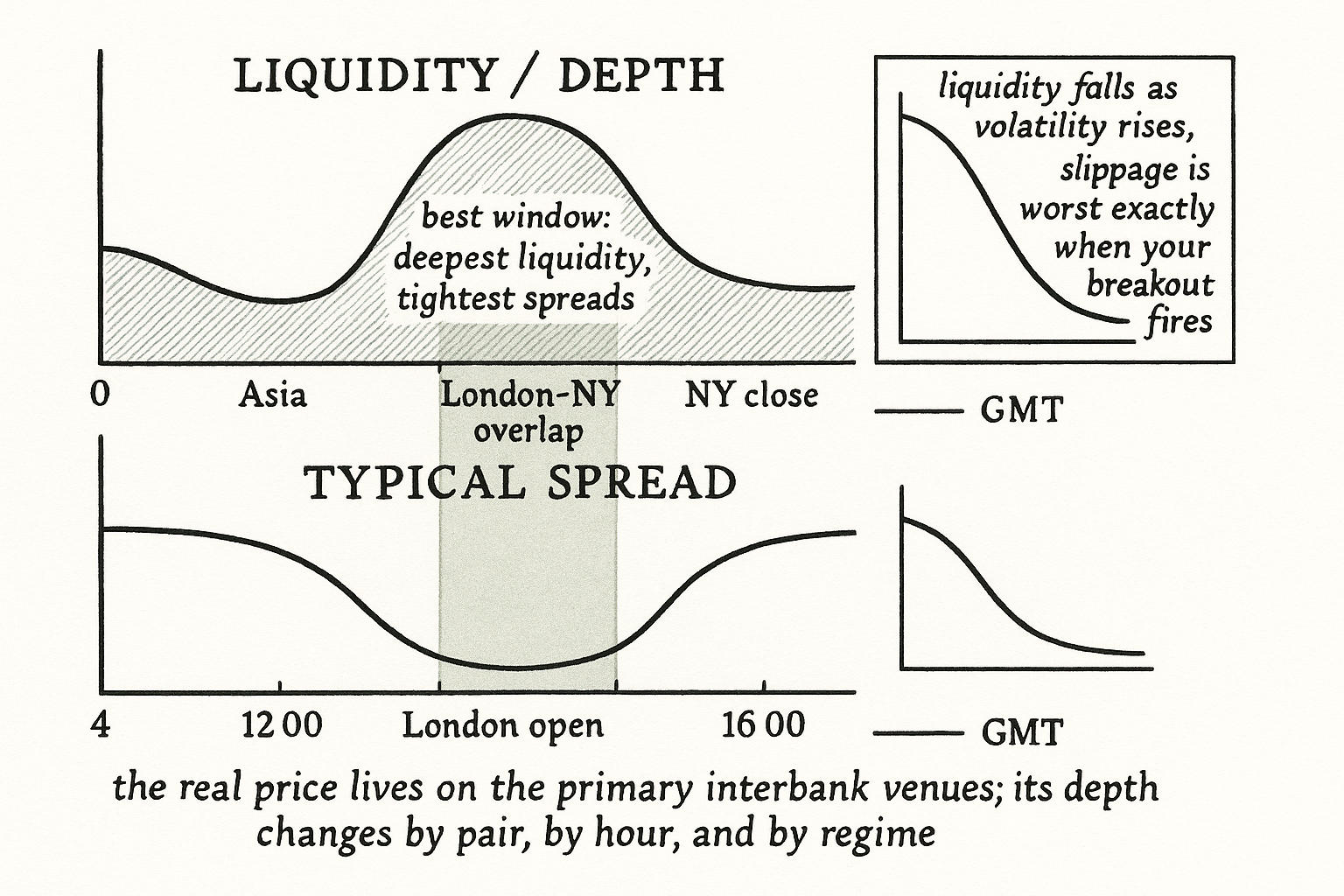

The single most important property of FX liquidity is that it moves, and it moves inversely to volatility. When markets are calm, spreads are tight and depth is good; when volatility spikes, liquidity evaporates exactly when you most want to trade. The two are inversely related, which is the cruel arithmetic of execution: the moments your system most wants to act (a violent breakout, a news shock) are the moments liquidity is thinnest and slippage is worst.

$$ \text{liquidity} \;\propto\; \frac{1}{\text{volatility}}, \qquad \text{expected slippage} \;\approx\; \frac{\text{order size}}{\text{available depth}} $$

Liquidity runs roughly inverse to volatility, so depth shrinks as volatility rises. Expected slippage is approximately your order size divided by the available depth, so the same order costs more to execute when depth has thinned. Put the two together and a fixed-size order suffers its worst slippage in the high-volatility, low-liquidity moments, which is precisely when momentum and breakout systems are firing. A backtest that assumes constant spread and instant fills is most wrong exactly where it matters most.

Liquidity varies by pair and by clock

Two more axes of variation a system has to respect.

By pair. Liquidity concentrates in the major, high-volume pairs, and there is a strong relationship between volume and liquidity: high-volume currencies have high liquidity and tight spreads, while exotic and emerging-market pairs have thin liquidity and wide, jumpy spreads. The practical rule is to stick to the liquid majors for any system sensitive to execution cost, because the wide spreads and slippage on illiquid pairs will eat an edge that looks fine on mid-price data. The best pairs to trade combine high liquidity with enough volatility to move, and there is a trade-off between the two.

By clock. FX liquidity follows the trading day. The overlap of the London and New York sessions is the deepest, most liquid window, when both major hubs are active and the major economic events, fixes, and option expiries cluster. The London open is a reflection point where big risk-takers process overnight information and aggressive trends often start; the New York open frequently extends a London move before it reverses. A system that trades the thin hours (the gap between the New York close and the Asian open) faces wider spreads and worse fills than the same system run in the London-New York overlap, the timeframe-and-timing point the article "How to Choose the Right Timeframe for a Strategy" made about matching a strategy to its conditions.

What this means for a system

The execution model has to be liquidity-aware, not a flat assumption. Three concrete habits follow.

Size to the available depth, not to a fixed lot. An order that is small relative to depth in the London-New York overlap can be large relative to depth in the thin Asian hours, and the slippage scales with that ratio. A liquidity-aware system shrinks size or stands aside when depth is thin.

Trade the liquid pairs and the liquid hours unless the strategy explicitly earns its keep elsewhere. The default is the majors during the overlap, because that is where the assumptions in a mid-price backtest are closest to true.

Model slippage as a function of volatility, not a constant. Since liquidity falls as volatility rises, the slippage your system pays should rise with volatility in the backtest, or you will systematically overstate the profitability of every signal that fires in turbulent conditions, the conditions a trend system depends on.

Visualizing liquidity through the day

KEY POINTS

- The price of a currency is set on a small number of primary interbank electronic venues where banks trade with each other. Every retail, broker, and platform price is a derivative of those primary venues.

- Locating the real bid and offer matters: the primary-venue price is the benchmark for your execution. Fills consistently worse than that mid beyond the expected spread and markup mean you are paying for latency, last look, or a wide B-book quote.

- FX liquidity is not constant and runs inverse to volatility. Spreads tighten and depth improves in calm markets and evaporate when volatility spikes, exactly when momentum and breakout systems fire.

- Expected slippage is roughly order size divided by available depth, so a fixed-size order suffers its worst slippage in the low-liquidity, high-volatility moments a mid-price backtest assumes away.

- Liquidity concentrates in high-volume major pairs; exotic and emerging pairs have thin, jumpy liquidity. Stick to the liquid majors for any cost-sensitive system. The best pairs combine high liquidity with enough volatility to move.

- Liquidity follows the clock. The London-New York overlap is the deepest window, where major events and fixes cluster. Thin hours between the New York close and the Asian open carry wider spreads and worse fills.

- Build a liquidity-aware execution model: size to available depth rather than a fixed lot, default to liquid pairs and liquid hours, and model slippage as a function of volatility rather than a constant.

- A backtest with constant spreads and instant fills is most wrong precisely where it matters most, in the turbulent conditions trend systems depend on.

References

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- The anatomy of the global FX market through the lens of the 2013 Triennial Survey

- FX Market Metrics: New Findings Based on CLS Bank Settlement Data

- The FX Race to Zero: Electronification and Market Structural Issues in Foreign Exchange Markets

- Why Tokenised Securities Need Authoritative Market Records, Not

- THE IMPACT OF FX CENTRAL BANK INTERVENTION IN A NOISE

- The bias of IID resampled backtests for rolling window mean

- Decomposing Equity Risk: The Case for Segment-Level Financial

- Identifying Noise Traders: The Head-And-Shoulders Pattern In U.S.

- The Foreign Exchange Market

- Microstructure of Foreign Exchange Markets

- Asymmetric Information in the Interbank Foreign Exchange Market

- The electronic trading systems and bid-ask spreads in the foreign exchange market

- Quantile liquidity connectedness in foreign exchange markets

- FX spot and swap market liquidity spillovers

- What is the impact of introducing a parallel OTC market? Theory and evidence from the Chinese interbank FX market

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.