4.27 Why Retail FX Execution Is Not the Same as Interbank FX

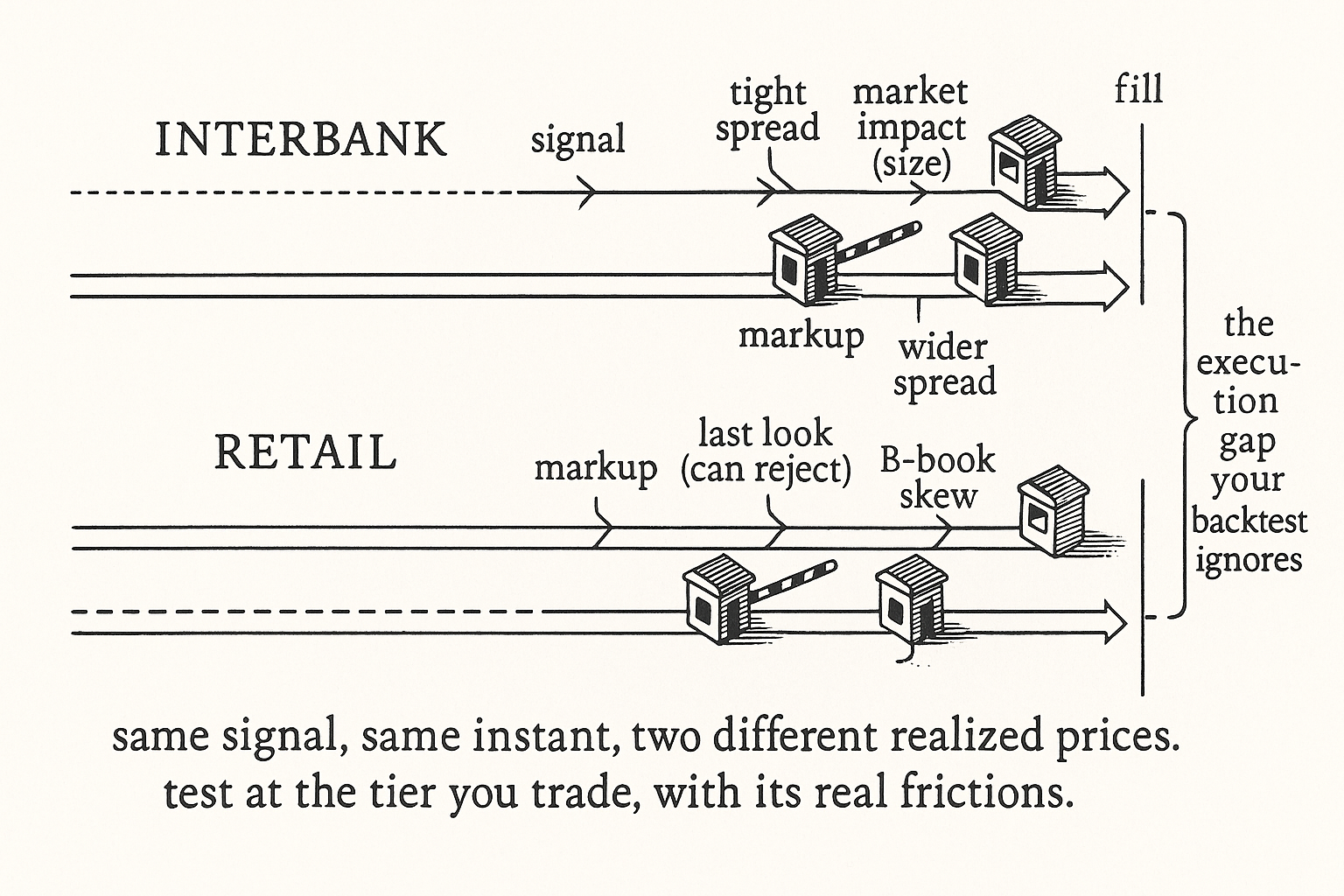

Interbank fills are tight and firm; retail adds markup, wider spreads, last look, and a B-book conflict. The same signal earns a different net edge by tier, so test with your tier's real frictions.

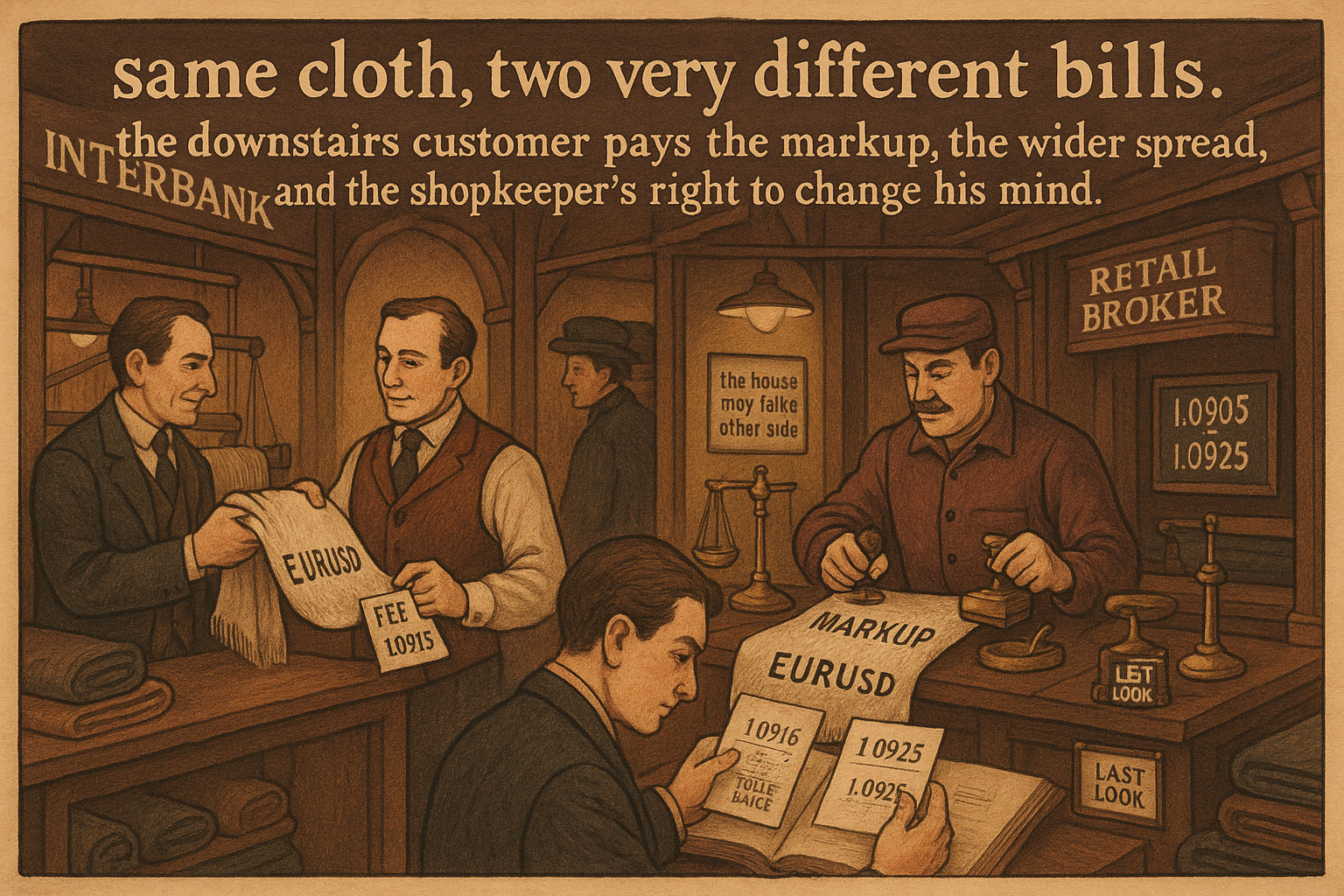

A backtest fills every order at the mid-price, instantly, in any size, at any time. Interbank execution comes close to that ideal for a professional: tight firm spreads, deep liquidity, fills that stick. Retail execution does not come close. A retail trader faces a marked-up spread, a broker that may hold the order for a last look and reject it if the market moved, possible requotes, and a counterparty that is often the broker itself rather than the market. The same signal, the same pair, the same instant, produces a different realized price depending on which door you walk through, and the retail door costs more.

Retail FX is enormous (in Japan alone there are on the order of a million active retail accounts, against far fewer in the US), and the entire retail apparatus is built on an execution model that differs from interbank in ways that directly determine whether a system is profitable. A strategy can clear interbank costs and fail retail costs, or be designed so its trade frequency and edge survive the retail markup. Knowing the difference is a prerequisite to backtesting honestly.

This article details the execution gap between the two tiers, continuing from "FX Is Not One Market: Retail vs Wholesale Structure" and "The Real Heart of FX Liquidity". It sets up the order-mechanics detail in "Market Orders vs Limit Orders in FX" and "How FX PnL Actually Works".

What interbank execution looks like

In the interbank market a dealer trades against firm, executable quotes on a primary venue. The spread is a fraction of a pip for the major pairs in normal conditions, the quotes are committed, and the main cost of trading in size is market impact: a large order moves the price as it consumes depth, leaving a footprint. The dealer's execution problem is to work a large order without revealing it and pushing the market away, a size problem, not a fairness problem. The price is real and the fill is honest; what you pay for is depth.

The interbank trader's costs are therefore the spread (small) plus market impact (rising with size). For a system trading modest size, interbank costs are close to the mid-price assumption a backtest makes, which is why institutional FX backtests can use tight cost models and be roughly right.

What retail execution adds

The retail trader inherits the interbank price and then pays for a stack of frictions the interbank trader does not.

The markup and wider spread. The broker quotes the interbank price plus a markup and a wider spread, so every round trip starts in a deeper hole than interbank. This is the tier cost from the structure article, paid on entry and exit.

Last look. Many retail and aggregated venues hold a submitted order for a brief moment and reserve the right to reject it if the price moved against the liquidity provider in that instant. The asymmetry is the problem: fills that would have moved in your favor get rejected, fills that move against you stick. Last look quietly worsens your realized fill distribution in a way no mid-price backtest captures.

B-book conflict. When the broker takes the other side of your trade (B-book) rather than passing it to the market (A-book), the broker profits when you lose. That conflict shows up as requotes on winning setups, slippage skewed against you, and spreads that widen at the worst moments. Not every broker B-books every client, but the system builder has to assume the execution terms are set by a counterparty whose interests may oppose theirs.

$$ \text{Edge}_{\text{net}} = \text{Edge}_{\text{gross}} - s_{\text{tier}} - \text{impact}_{\text{tier}} - c_{\text{tier}}, \qquad c_{\text{retail}} \gg c_{\text{interbank}} $$

Net edge is the gross edge minus the tier's spread, minus the tier's market impact, minus a tier-specific extra cost that bundles markup, last-look rejection, and adverse fill skew. That extra cost is small for interbank and large for retail. Two traders with the same gross signal edge end up with different net edges because the subtracted costs differ by tier, and a gross edge that survives interbank's small deductions can be wiped out by retail's large ones.

What this does to a strategy

The execution gap reshapes which strategies are viable at each tier, the same cost-versus-frequency logic the article "Why Transaction Costs Should Be Added Before You Fall in Love" applied to all systems, sharpened for FX tiers.

High-frequency and scalping strategies depend on capturing a tiny edge many times, and the retail markup plus last look devours that edge. These strategies are interbank-only; on retail they are a fee-generation machine for the broker. A scalping backtest that ignores retail execution is the most dangerous backtest in FX, because it looks the most profitable and fails the hardest.

Lower-frequency swing and position strategies trade rarely enough that the retail cost per trade is small relative to the per-trade edge. A system that holds for days and targets a move many times the spread can absorb the retail markup and still be net positive. Matching trade frequency to tier cost is the design lever: the higher the per-trade cost, the larger and rarer the moves the strategy must target.

The honest test is to backtest with the actual tier's costs, including a realistic last-look rejection rate and a markup, not the mid. If the edge only exists on mid-price fills, it is not an edge you can trade retail. Model the frictions, then decide.

What you can and cannot control

A closing dose of realism on what the retail system builder actually governs.

You control pair choice, time of day, order type, and trade frequency, and these are the levers that keep you on the cheaper side of the retail cost structure: liquid majors in the London-New York overlap, order types that do not pay unnecessary spread, and a frequency that respects the markup. You do not control last look, the markup, or whether the broker B-books you. The system has to be robust to costs you cannot remove, which means leaving a margin between the gross edge and the worst plausible retail cost, not designing to the mid and hoping.

The broker choice itself is part of the system. An honest A-book broker with tight markups and no last look changes the math; a wide B-book broker can make the same strategy unviable. Treating the broker as a fixed input and stress-testing the strategy against pessimistic execution is the discipline that keeps a retail FX system from dying on contact with live fills, the recipe-versus-reality gap the article "Trading Systems Are Recipes, Not Predictions" flagged for every live system.

Visualizing the execution gap

KEY POINTS

- A backtest fills at the mid instantly in any size. Interbank execution approximates that for a professional; retail execution does not, and the gap determines whether a system is profitable.

- Interbank execution is firm, tight-spread, and honest. Its main cost is market impact: large orders move the price and leave a footprint. For modest size, interbank costs are close to the mid assumption.

- Retail execution adds a stack of frictions: a markup and wider spread, last look (the right to reject a fill if the price moved, asymmetrically against you), and a possible B-book conflict where the broker profits when you lose.

- Net edge is gross edge minus the tier's spread, impact, and a tier-specific extra cost bundling markup, last-look rejection, and adverse fill skew. That extra cost is small for interbank and large for retail.

- High-frequency and scalping strategies depend on a tiny repeated edge that the retail markup and last look devour. They are interbank-only; a scalping backtest ignoring retail execution is the most dangerous in FX.

- Lower-frequency swing strategies trade rarely enough that retail cost per trade is small relative to the per-trade edge. Match trade frequency to tier cost: higher cost demands larger, rarer target moves.

- Backtest with the actual tier's costs, including a realistic last-look rejection rate and markup. An edge that only exists on mid-price fills is not tradeable retail.

- You control pair, time of day, order type, and frequency; you do not control last look, markup, or B-booking. Leave a margin between gross edge and worst plausible retail cost, and treat the broker choice as part of the system.

References

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Trading Costs in the Foreign Exchange Market: A Microstructure Analysis of the Bid–Ask Spread

- Microstructure Evidence from the Polymarket Order Book - arXiv

- Identifying Noise Traders: The Head-And-Shoulders Pattern In U.S.

- Decomposing Equity Risk: The Case for Segment-Level Financial

- Reframing Financial Markets as Complex Systems

- Search Frictions in Over‐the‐Counter Foreign Exchange Markets

- Why Tokenised Securities Need Authoritative Market Records, Not

- Triangular Arbitrage, Market Microstructure, and Correlation

- Microstructure of Foreign Exchange Markets

- The Foreign Exchange Market*

- Bid-Ask Spreads in Foreign Exchange Markets

- Trading Patterns and Prices in the Interbank Foreign Exchange Market

- Search Frictions in Over‐the‐Counter Foreign Exchange Markets

- The anatomy of the global FX market through the BIS Triennial Survey

- Should Retail Investors' Leverage Be Limited? Evidence from the U.S. Retail FX Market

- Dealer Networks, Client Sophistication and Pricing in OTC Currency Derivatives

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.