1.1 Trading Systems Are Recipes, Not Predictions

Most traders think systems predict markets. They don’t. A trading system is closer to a recipe: a repeatable process with defined inputs, rules, and outputs. This article explains why the prediction mindset destroys traders, and why robust systematic trading starts with process, not prophecy.

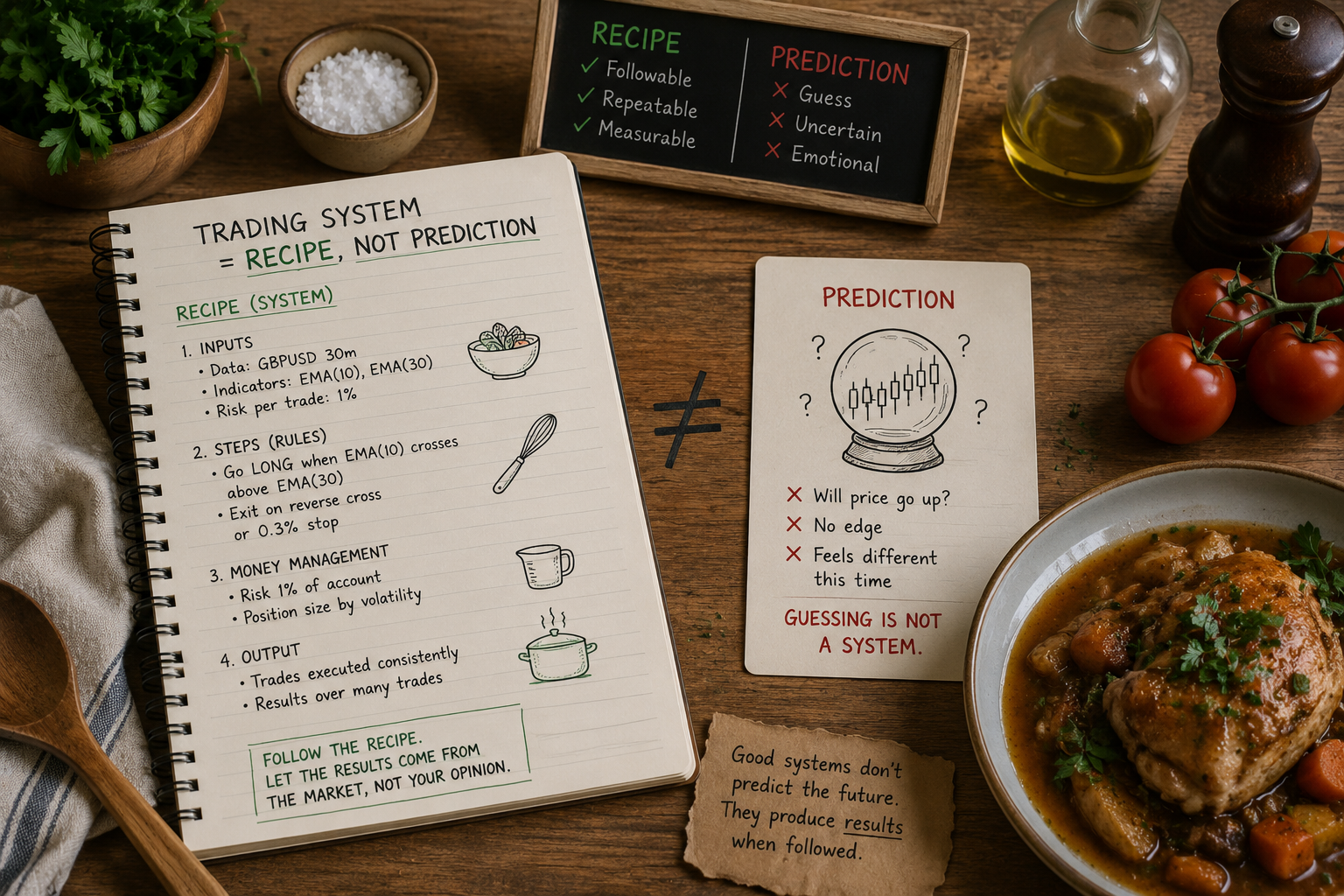

A trading system is a recipe. A list of instructions you follow without asking the stove for permission. You measure, you add, you wait, you serve. The food comes out edible or it doesn't. The recipe does not predict that the dish will be tasty. It produces the dish.

This framing kills most of the noise around quant trading. Retail content frames a system as a prediction engine: "EMA crossover predicts the next swing." A prediction engine implies a fortune teller, and traders evaluate fortune tellers by how many times they were right. Wrong question. A recipe is judged on whether the kitchen runs, the inputs are repeatable, the output is consistent, and the cost of cooking does not exceed the price you charge for the meal.

What a system is

A trading system is a precise set of rules that defines entries and exits without any human discretionary intervention. Two words are doing the load-bearing work: precise and automatic. If you cannot hand the rules to a stranger and have them generate the same trades on the same data, you do not have a system. You have a vibe.

The recipe analogy holds because both objects share three properties:

- Inputs are specified (data, parameters, instruments).

- Steps are specified (entry rule, exit rule, sizing).

- Output is reproducible across cooks.

Take a moving-average crossover. Long when the 10-bar EMA crosses above the 30-bar EMA on GBPUSD 30-minute bars. Exit on the reverse cross or on a 0.3% stop. Position sized to 1% of account risk per trade. Hand that to ten people with the same data feed and you get the same equity curve. Hand "I look for trend confirmation with momentum" to ten people and you get ten different equity curves and ten arguments.

Why "prediction" is the wrong word

Predicting price is a hopeless framing for three reasons.

The first reason is that prediction implies you know direction. You do not. You have a conditional expectation: given this signal, the empirical distribution of forward returns shifts a small amount in a measurable direction. A rule's predictive power is the component of return left over after you strip out long bias and market trend. From 1976 to 2004 the SPX returned 4.22% annualized, or 0.035% per day. A system long 40% of the time captures about 1.7% of that drift for free, with zero predictive content. Long 90% of the time captures 3.8%. Calling either number "prediction" is a scam against yourself.

The second reason is that the word makes you defensive about losing signals. If your job is to predict, every losing trade is a failed prediction and an ego event. If your job is to follow a recipe, a losing trade is a stove producing a charred steak under conditions allowed by the recipe. The fix is not self-flagellation. The fix is to check whether the recipe still serves more steaks than it burns over a meaningful sample.

The third reason is that prediction language collapses two distinct objects: the rule and the position. They are separate machines. The rule outputs a forecast, a scaled number on a stable distribution centered around an absolute value of around 10. The portfolio layer translates that forecast into a position sized by volatility and capital. The forecast is the recipe step that says "add three grams of salt." It is not a claim about how the customer will feel.

You are the broken instrument

Algorithms beat experts not because algorithms are smart. The reason is that humans, including you, carry cognitive defects that show up at full strength the moment live money is on the line.

Two failures wipe out most discretionary traders. You take small wins to confirm your decision was right. You hold large losses because closing them admits the decision was wrong. Get-even-itis. Run any backtest of your own discretionary trade log against the same rules executed mechanically. The mechanical version wins more often than not, and the gap is the cost of running your brain in the loop. Trading systems work, system traders don't. The system traders break because they edit the recipe mid-cook.

The recipe framing handles this. Once you commit to the rules, your job stops being "decide." Your job becomes execution and monitoring. Position sizes are not yours to argue with. Exits are not yours to override because the chart "feels different." If you discover the rules are wrong, you change them between sessions, with data, not in the middle of a trade.

Recipes assume the cuisine still exists

The analogy has a sharp edge. A recipe for cassoulet works if duck fat is still available. A recipe for an FX breakout system on 30-minute GBPUSD works if intraday volatility, liquidity, and order-flow structure resemble the period the recipe was built on. Markets change. The standard arc for any working system is the same: in-sample build, a stretch of out-of-sample survival, then years of slow decay as the regime it was fitted to dissolves.

Every system has to be switched off at some point. The hard part is knowing when. A trader who thought he was running a prediction engine fights this. He keeps re-optimizing, adding filters, tightening stops, telling himself the model is "almost there." A trader who knows he was running a recipe shrugs, marks the system dead, and writes a new one. The intellectual humility is built into the framing.

Two operational habits follow. Run multiple recipes at once, not a single best system. The decay curve is a forecast of every system you will ever build.

Diversification across uncorrelated rule families is your only protection against the day one of them stops working. Set a kill criterion on every live system before you turn it on. Drawdown beyond a historical 95% confidence band. Average trade collapsing under transaction cost. Equity below a defined regression line. When the criterion fires, you switch the system off. You do not negotiate with it.

Backtesting and optimization are sharp knives

Backtesting and portfolio optimization are powerful tools that are also dangerous.

The danger lives in how often they cut the cook. Three knives, three cuts.

Selection bias. Pick the best Sharpe out of 40 variations on the same idea and you get a rule that shines on training data and reverts to the Sharpe of a coin flip out of sample. With 100 random rules and a few years of history, you can surface a Sharpe above 1 by luck alone. The cure is to stop selecting. Run an equal-weighted blend of variations and let volatility-scaling shrink dead variants down, not stock-picking the backtest.

Overfitting. The count of rules and conditions plus the data they consume should not exceed 10% of the data sample. A system using a 30-day moving average needs at least 300 days of history to estimate its parameters defensibly. Five parameters at ten settings each gives you 10,000 variants, enough variation to manufacture a beautiful equity curve from pure noise. If your in-sample Sharpe is 3 and your out-of-sample Sharpe is 0.4, the rule is dead before it goes live.

Curve-fit stops. Optimizing the stop-loss distance to the value that maximizes net profit is the trap most retail systems die in. Plot the distribution of intraday drawdowns against final P&L for every closed trade. Place the stop where it cuts losing trades without amputating winners. The right stop sits inside a stable region of the optimization surface, where moving it 100 pips in either direction barely changes net profit. A stop that sits on a spike, where moving it 10 pips halves the result, is curve-fit and will die in live trading.

How this article sets up the rest

Every article that follows operates inside the recipe framing. The next one diagnoses the human-error layer in more detail. After that comes the modular vocabulary: rule, strategy, portfolio. Later pieces pull apart the inductive uncertainty in a single sample of price history, force every rule to declare what would prove it dead, and defend the equal-blend approach against the temptation of complex models. Each one is a check on the recipe before you trust it with capital.

None of them treats trading as fortune-telling.

KEY POINTS

- A trading system is a recipe. Inputs, steps, and outputs are precise enough that a stranger reproduces the same trades on the same data.

- Precise and automatic are the load-bearing words. Discretionary inputs disqualify a system.

- Prediction framing makes you defensive, ego-driven, and prone to edit the rules mid-trade.

- Strip long bias and market trend from any backtest before you claim predictive power. SPX 1976-2004 ran at 4.22% annualized. A 40% long-biased rule captures 1.7% of that for free.

- Your brain is the unreliable instrument under live P&L. Get-even-itis closes the wrong trades and lets the wrong trades run.

- Every recipe assumes the kitchen still exists. Markets change. Every system gets switched off.

- Diversify across rule families and write a kill criterion before going live.

- Cap degrees of freedom at 10% of the sample, blend variants instead of selecting the best, place stops on stable regions of the surface, not spikes.

References

- Evidence-Based Technical Analysis - David Aronson (Amazon)

- Systematic Trading - Robert Carver (Amazon)

- Evidence-Based Technical Analysis: Applying the Scientific Method and Statistical Inference to Trading Signals

- Systematic Testing of Systematic Trading Strategies

- Evaluating Trading Strategies

- Comparing Discretionary and Systematic Hedge Fund Performance

- Traditional Traders vs. Quant Traders: A Comparative Analysis of Strategies, Performance, and Market Interactions

- How to Evaluate Trading Strategies: Single Agent Market Replay or Multiple Agent Interactive Simulation?

- Applications of the Chi-Square Distribution in Quantitative Finance

- Hypothesis Testing | CFA Institute