4.29 Market Orders vs Limit Orders in FX

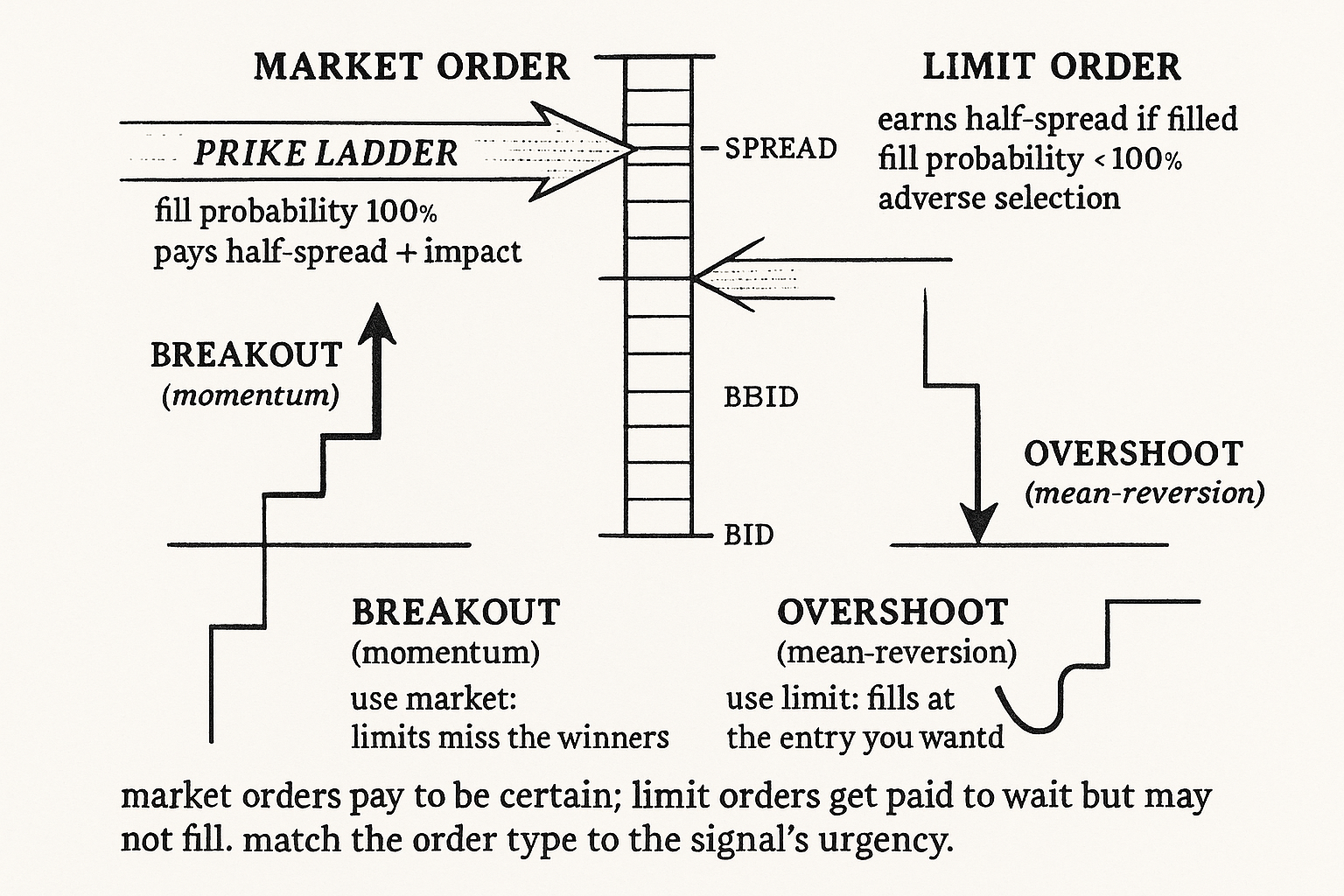

A market order pays the spread for a certain fill; a limit order earns the spread but may never fill and is adversely selected. Match it to the signal: market for momentum, limit for mean-reversion.

A breakout system fires a buy. Two ways to act on it. Send a market order and you cross the spread immediately, paying the offer, certain of a fill but starting the trade already down the spread. Send a limit order at the bid and you wait for the market to come to you, paying nothing to cross, but you only get filled if price dips to your level, and if the breakout is real it never does, so you miss the trade entirely. The choice between the two is not a detail. For a system that trades often, the order type can be the difference between a live edge and a dead one, because it determines whether you pay the spread or earn it, and whether you get filled when you most need to.

A market order takes liquidity and pays for immediacy; a limit order provides liquidity and gets paid for patience, at the cost of fill uncertainty. Every FX system makes this trade-off on every order, and the right answer depends on how urgent the signal is. Momentum needs to be in now and pays the spread; mean-reversion can afford to wait and can earn it. Picking the wrong order type for the signal is a quiet, recurring leak.

This article works the two order types and the costs each carries, building on the PnL mechanics in "How FX PnL Actually Works" and the execution tiers in "Why Retail FX Execution Is Not the Same as Interbank FX". It leads into the microstructure noise of "Why Bid/Ask Bounce Matters for Intraday FX Systems".

The market order: pay to be certain

A market order executes immediately at the best available price, which means crossing the spread: a buy pays the offer, a sell hits the bid. You are guaranteed a fill (in normal liquidity), and you pay for that certainty with the spread plus, for larger orders, market impact as you consume depth and leave a footprint.

$$ \text{Cost}_{\text{market}} \;\approx\; \tfrac{1}{2}\,s \;+\; \text{impact}(\text{size}), \qquad \text{fill probability} = 1 $$

The cost of a market order is about half the spread (the distance from mid to the offer you pay) plus a market-impact term that grows with order size, and the fill probability is one. You always trade, and you always pay. For a small order the cost is essentially half the spread; for a large order the impact term dominates and the real skill is working the order to minimize the footprint. The market order's defining feature is certainty: you will be in the trade, which is exactly what an urgent signal needs.

The limit order: get paid to wait

A limit order rests at a chosen price and executes only if the market trades to it. A buy limit at or below the bid does not cross the spread; if filled, you bought at your price rather than paying the offer, effectively earning the spread instead of paying it. The cost is not in the spread but in two other places: the order may never fill (opportunity cost), and the fills you do get are adversely selected.

$$ \text{Cost}_{\text{limit}} \;\approx\; -\tfrac{1}{2}\,s \;+\; \text{adverse selection}, \qquad \text{fill probability} < 1 $$

The nominal cost of a limit order is negative half the spread (you earn rather than pay it), offset by an adverse-selection term, and the fill probability is below one. Adverse selection is the catch that kills naive limit strategies: your buy limit fills when sellers are hitting it, which is disproportionately when the price is about to keep falling, so the fills you get are the ones you would rather not have, and the fills you wanted (when price rallies away) never happen. You earn the spread on the trades that go against you and miss the trades that go for you, which is the opposite of what the headline "earn the spread" suggests.

Matching order type to signal

The decision rule is to match the order type to the urgency and direction-dependence of the signal.

Momentum and breakout signals need market orders. The whole premise is that price is about to move in your direction and keep going, so a limit order resting behind the move never fills, and you miss precisely the trades the system exists to catch. You pay the spread because the alternative is no position, and the expected move is large relative to the spread, so paying it is worth it. A breakout system that tries to save the spread with limit orders systematically captures only the failed breakouts (the ones that came back to fill the limit) and misses the winners, an adverse selection that inverts the edge.

Mean-reversion and range signals suit limit orders. The premise is that price has overshot and will come back, so resting a limit at the extreme both earns the spread and expresses the thesis: you want to be filled exactly when price spikes to your level, because that is the entry you were waiting for. Here the adverse selection partly works for you, because the fill happens at the overshoot you intended to fade. A mean-reversion system using market orders pays the spread on every trade and gives back a chunk of a naturally small edge.

This is the execution layer of the strategy-family map from "Matching Strategy Families to Market Conditions": the same noise axis that picks trend versus reversion also picks market versus limit, because trend needs immediacy and reversion needs patience.

The traps

Where the order-type choice goes wrong.

Limit orders in fast markets give a false sense of cost saving. In a breakout, the limit that does not fill is not a saved spread; it is a missed trade, and the opportunity cost of missing the winners dwarfs the spread you saved on the losers. Counting only the spread saved on filled orders and ignoring the trades you missed is a measurement error that makes limit strategies look better than they are.

Market orders in thin liquidity pay far more than the quoted spread. The cost formula assumes normal depth; in the thin hours or a volatility spike, a market order walks the book and pays slippage well beyond half the spread, the liquidity-volatility inverse from "The Real Heart of FX Liquidity". An urgent market order during a news shock can cost many times its calm-market spread.

Stop orders are market orders in disguise. A stop-loss triggers a market order when hit, so it pays the spread and the slippage at the worst possible moment, when price is moving against you fast. Sizing and placing stops without accounting for that slippage understates the realized loss, the gap between a backtest's clean stop fill and a live stop's slipped fill.

Visualizing the order-type trade-off

KEY POINTS

- A market order takes liquidity and pays for immediacy; a limit order provides liquidity and gets paid for patience, at the cost of fill uncertainty. Every FX order makes this trade-off.

- A market order crosses the spread (buy pays the offer, sell hits the bid), costs about half the spread plus size-dependent market impact, and fills with certainty. Its defining feature is that you will be in the trade.

- A limit order rests and fills only if price reaches it. It nominally earns half the spread instead of paying it, offset by adverse selection, and fills with probability below one.

- Adverse selection is the limit-order catch: your buy fills when sellers are hitting it, disproportionately when price keeps falling. You earn the spread on the trades that go against you and miss the ones that go for you.

- Match order type to signal. Momentum and breakout need market orders, because a resting limit never fills on a real breakout and captures only the failed ones, inverting the edge.

- Mean-reversion and range signals suit limit orders, because you want to fill exactly at the overshoot you intend to fade, and the adverse selection partly works for you.

- This is the execution layer of the strategy-family map: the noise axis that picks trend versus reversion also picks market versus limit, since trend needs immediacy and reversion needs patience.

- Traps: limit orders in fast markets hide missed-trade opportunity cost as fake spread savings; market orders in thin liquidity pay far beyond the quoted spread; and stop-losses are disguised market orders that slip at the worst moment.

References

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Lead-Lag Relationships in Market Microstructure⋆

- Order Flow and Exchange Rate Co-movement

- OPTIMAL EXECUTION HORIZON

- Converse trading strategies, intrinsic noise and the stylized facts of

- High-Frequency Trading, Asset Pricing, and Market Microstructure

- News and Intraday Retail Investor Order Flow in Foreign Exchange

- Price Clustering Asymmetries in Limit Order Flows - jstor

- Identifying Noise Traders: The Head-And-Shoulders Pattern In U.S.

- The submission of limit orders or market orders: The role of timing

- How are they determined in a limit order market?

- Limit Order Book as a Market for Liquidity

- The information content of a limit order book: The case of an FX market

- Foreign exchange markets: Price response and spread impact

- Importance of transaction costs for asset allocation in foreign exchange markets

- Foreign Exchange Order Flow as a Risk Factor

- Limit order books

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.