4.25 FX Is Not One Market: Retail vs Wholesale Structure

FX is two markets, not one: a wholesale tier where price is discovered and a retail tier selling a marked-up, wider-spread copy. Backtest one and trade the other, and the gap eats your edge.

Two traders buy EURUSD at the same instant. One is a bank dealer hitting a price on a primary interbank venue; the other is a retail trader clicking buy in a broker app. They are not trading in the same market, and they are not getting the same price. The dealer trades on a centralized electronic venue against other professional liquidity, at a spread of a fraction of a pip in size. The retail trader trades against a broker that quotes a derived price with a markup, may decline the fill on a last look, and shows a spread several times wider. The EURUSD chart they both stare at hides the fact that "the price of EURUSD" is not a single number. It is a stack of different prices at different tiers.

FX is highly decentralized, with no single exchange, and it splits into two interacting segments: a wholesale interbank market where price discovery happens, and a retail market that consumes a derived version of that price. The two are connected, so they track each other, but they are structurally different markets with different prices, spreads, and execution rules. Treating them as one is the mistake behind most retail FX backtests that look profitable and lose money live.

This article maps the two-tier structure and draws the consequences for system builders. It opens the FX microstructure run of Pillar 4 that continues through "The Real Heart of FX Liquidity" and "Why Retail FX Execution Is Not the Same as Interbank FX", and it is the structural foundation the execution articles build on.

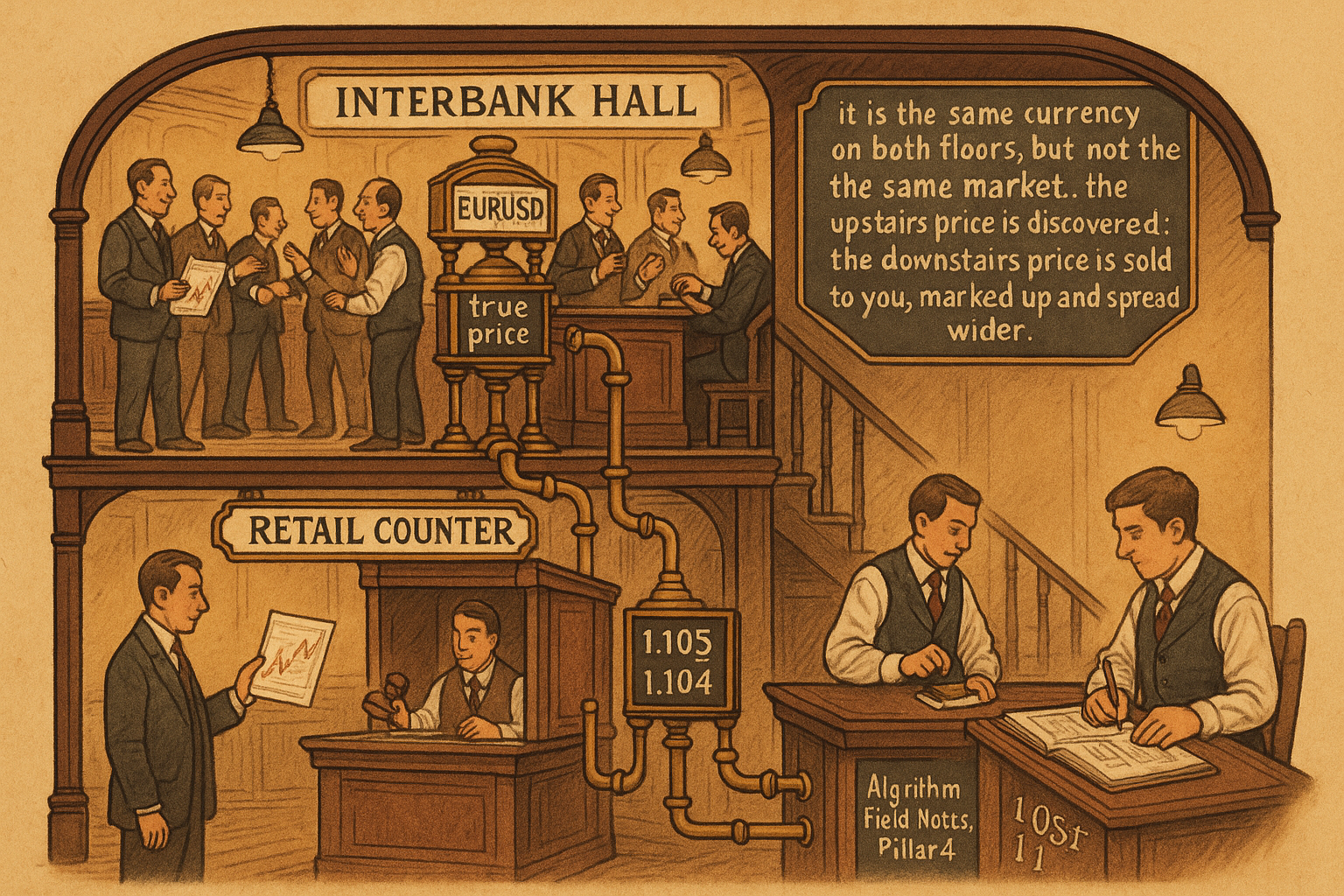

The two tiers

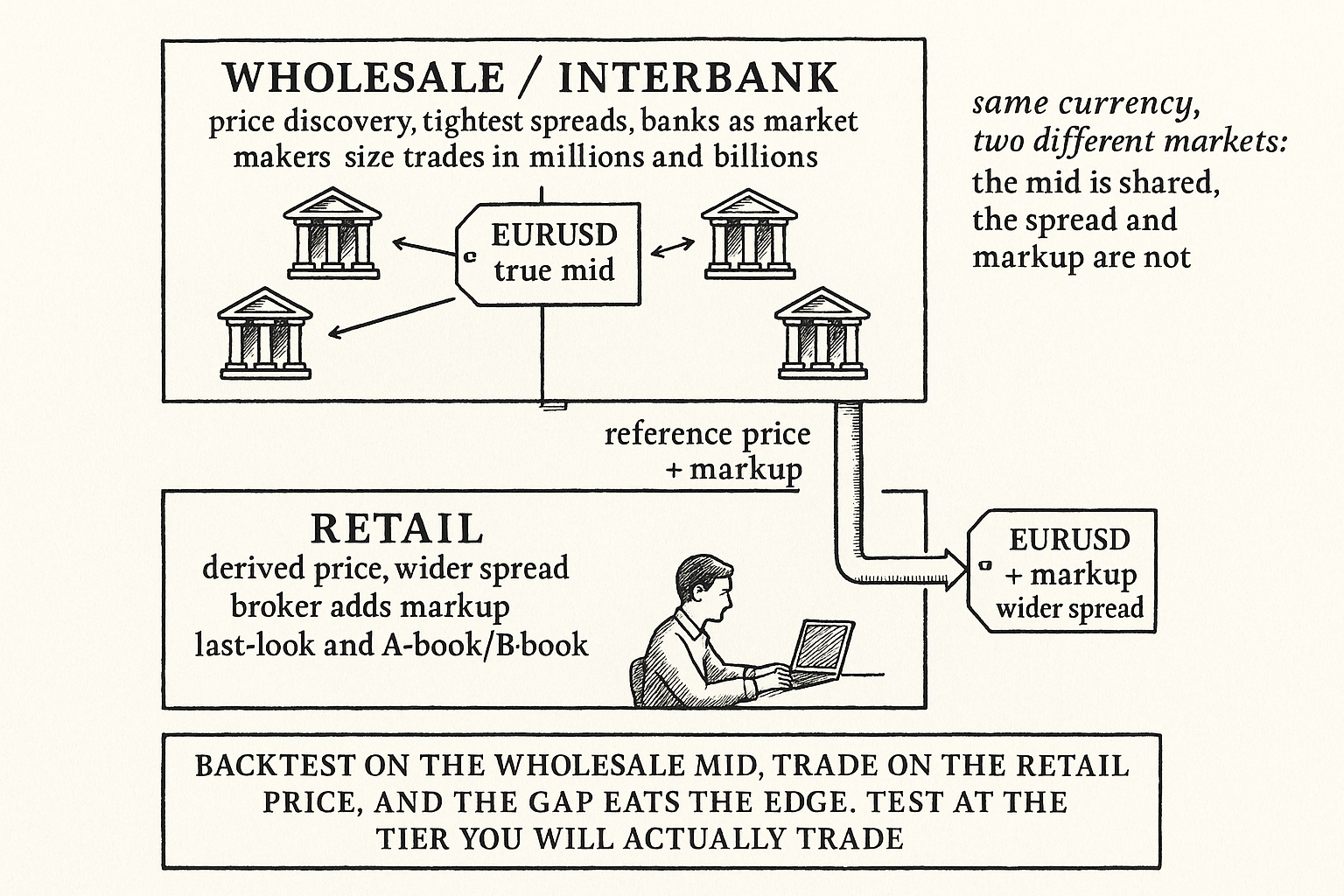

The wholesale tier is the interbank market, where banks and large institutions trade with each other and where the real price of a currency is discovered. Bank dealers act as market makers, quoting two-sided prices, and they also take directional risk in anticipation of client flow. This is where size trades, where spreads are tightest, and where the reference price that everything else hangs off is set. The participants are professionals trading in millions and billions; in dealer slang a "buck" is one million and a "yard" is one billion.

The retail tier sits downstream. A retail broker takes the interbank price as a reference, adds a markup, and shows the client a quote. The broker either passes the client's trade through to the wholesale market (agency, or A-book) or takes the other side itself (principal, or B-book). The retail price is a function of the wholesale price, but it is not the wholesale price: it carries a markup, a wider spread, and execution terms the client does not control.

$$ P_{\text{retail}} = P_{\text{interbank mid}} \;\pm\; \tfrac{1}{2}\,s_{\text{retail}} \;+\; m, \qquad s_{\text{retail}} > s_{\text{interbank}} $$

The retail price equals the interbank mid-price, plus or minus half the retail spread depending on whether you buy or sell, plus a markup m. The retail spread is wider than the interbank spread. The mid is shared (the two tiers track each other), but the spread and the markup are the retail trader's added cost, and they are the gap between the price on the chart and the price you actually transact at.

Why this breaks naive backtests

The structural split has one dominant consequence for systems: the data you backtest on and the prices you execute at come from different tiers, and the gap between them is where the edge dies.

A backtest run on a clean mid-price series (or an interbank feed) measures an edge available in the wholesale market. Trade the same system through a retail broker and you pay the wider retail spread and the markup on every round trip, costs the backtest never saw. A strategy with a small per-trade edge, common for any high-frequency or mean-reversion FX system, can be net positive on interbank costs and net negative on retail costs, the threshold problem the article "Why Transaction Costs Should Be Added Before You Fall in Love" made central. The tier mismatch is the single most common reason a profitable-looking FX backtest loses money in a retail account.

The fix is to backtest at the tier you will trade at. If you execute retail, model the retail spread and markup, not the mid. If you execute interbank, you still pay the spread and face market impact for size. Either way, the costs are tier-specific, and a backtest that uses one tier's prices to estimate another tier's profits is measuring a market you cannot access.

The same currency, different liquidity

The two tiers also differ in how much you can trade and how the price reacts. In the wholesale market, large orders move the price (market impact), and the cost of size is the footprint your order leaves, handled in "Market Orders vs Limit Orders in FX". In the retail market, the broker absorbs small clicks easily but controls the terms: it can widen spreads in volatility, requote, or decline a fill on last look, so the retail trader's effective liquidity is whatever the broker chooses to offer at that moment.

The practical upshot for a system builder is that the same EURUSD signal has different economics at different tiers, the FX-specific version of the point "Why FX Traders Must Watch Gold, Rates, and Equities" made about a currency being a relative object. A scalping system that needs sub-pip spreads can only live in the wholesale tier; a slower swing system that trades a few times a week can survive retail spreads. Matching the strategy's cost sensitivity to the tier's cost structure is a design decision that comes before any signal work.

Visualizing the two tiers

KEY POINTS

- FX has no single exchange. It splits into two interacting segments: a wholesale interbank market where price is discovered, and a retail market that consumes a derived version of that price.

- In the wholesale tier, banks act as market makers and take directional risk anticipating client flow. This is where size trades, spreads are tightest, and the reference price is set. A "buck" is a million, a "yard" a billion.

- The retail tier sits downstream: a broker takes the interbank price, adds a markup and a wider spread, and either passes the trade to the wholesale market (A-book) or takes the other side (B-book).

- The retail price equals the shared interbank mid plus or minus half the wider retail spread plus a markup. The mid is common; the spread and markup are the retail trader's added, tier-specific cost.

- The dominant consequence for systems: backtest data and execution prices come from different tiers, and the gap is where the edge dies. A small per-trade edge can be positive on interbank costs and negative on retail costs.

- Backtest at the tier you will trade. Retail execution means modeling retail spread and markup, not the mid; interbank execution still pays the spread and faces market impact for size.

- Liquidity differs too: the wholesale market charges size through market impact, while the retail broker controls the terms and can widen, requote, or decline on last look.

- Match the strategy's cost sensitivity to the tier: sub-pip scalping can only live wholesale, while a slower swing system can survive retail spreads. Tier choice is a design decision before any signal work.

References

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Stochastic Structure of Brokered Foreign Exchange Auctions

- The FX Race to Zero: Electronification and Market Structural Issues in Wholesale FX Markets

- Lead-Lag Relationships in Market Microstructure⋆

- EVIDENCE FROM UTILITY REGULATION - NBER

- Pricing, Demand, and Product Design of Innovative Securities

- High-Frequency Trading, Asset Pricing, and Market Microstructure

- Regulating Competition in Wholesale Electricity Supply by ... - NBER

- Full article: Pricing in practice in consumer markets - Taylor & Francis

- Microstructure of Foreign Exchange Markets

- Foreign Exchange Market Structure, Players and Evolution

- Search Frictions in Over-the-Counter Foreign Exchange Markets

- Order Flow and the Bid–Ask Spread: An Empirical Probability Model of Screen-Based Trading

- Dealer Behavior and Trading Systems in Foreign Exchange Markets

- Should Retail Investors’ Leverage Be Limited? Evidence from the U.S. Retail FX Market

- Strategic Insider Trading in Foreign Exchange Markets

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.