4.58 The Carry Trade: Up the Escalator, Down the Elevator

Carry pays you the yield differential and rides crowded appreciation up a smooth escalator, then gives it all back down the elevator in a risk-off panic. The killer detail: inverse-volatility sizing maxes your position right before the crash.

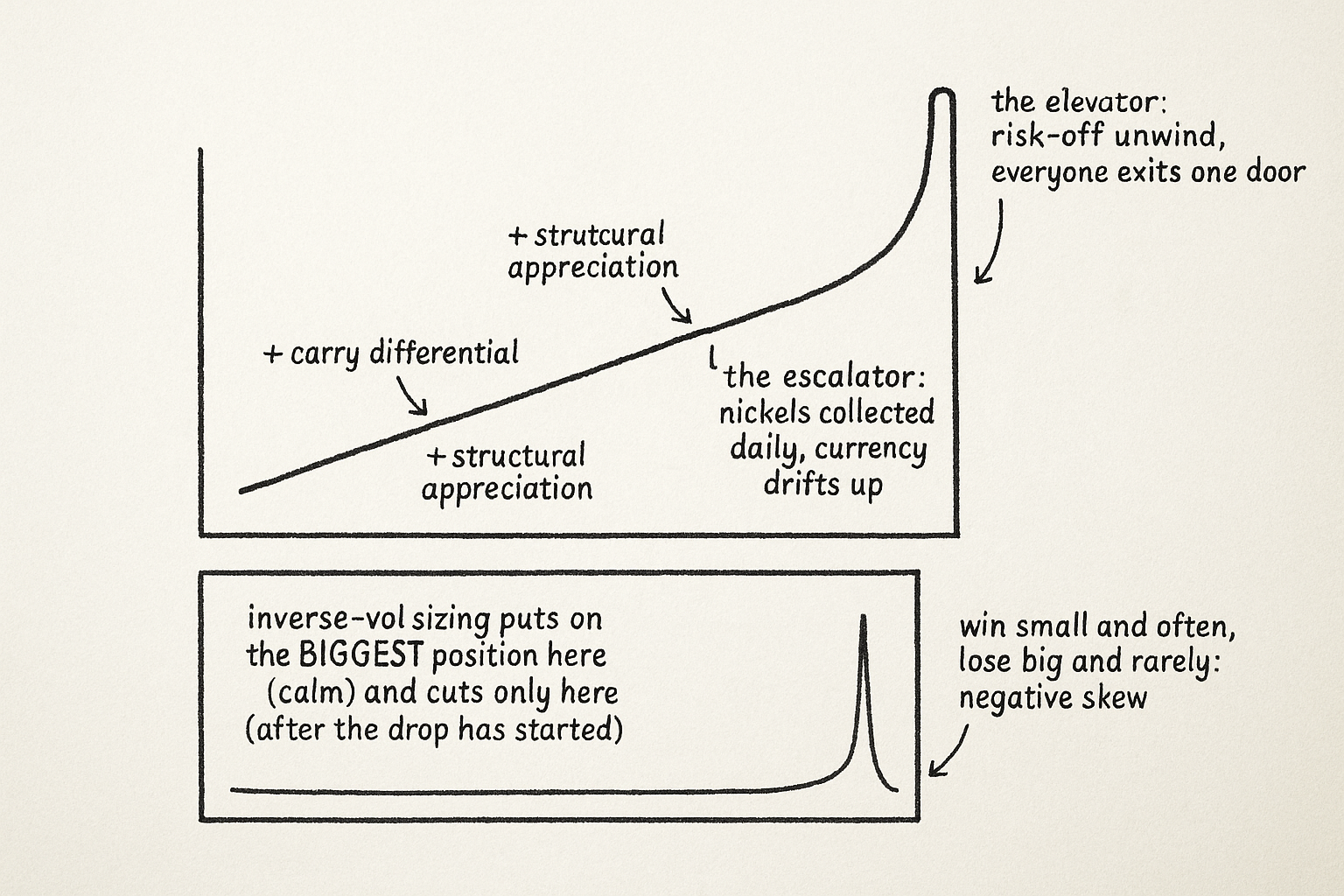

Borrow yen at half a percent, buy the Australian dollar at five, pocket the four-and-a-half-percent gap, and watch the Australian dollar slowly appreciate on top of the yield you are already collecting. The position pays you every day to hold it. The equity curve climbs a smooth, gentle slope for two or three years, the Sharpe ratio looks like something you would frame, and then over four sessions in a risk-off panic the whole thing gives back eighteen months of gains. Carry goes up the escalator and down the elevator. The escalator is the slow grind of the yield pickup and the structural appreciation it drives. The elevator is the unwind, and it does not stop at your floor.

The carry trade is the most important structural force in FX and the most dangerous payoff profile a systematic trader can hold without understanding it. The danger is not that it loses money on average. It makes money on average, which is exactly the trap: a strategy with a high hit rate, a smooth ride, and a fat negative tail looks like a great strategy right up until the tail arrives, and the standard tools that should size it down actually size it up at the worst moment. This article works the mechanics, the skew, and the specific way volatility-targeting betrays the carry trader.

What the trade actually earns

The return on a carry position has two parts: the interest differential you collect for holding the high-yielder against the low-yielder, and the change in the spot rate over your holding period.

$$ r_{\text{carry}} \;=\; \underbrace{(r_{\text{high}} - r_{\text{low}})}_{\text{interest differential (the carry)}} \;+\; \underbrace{\Delta S}_{\text{spot change}} $$

The first term is the carry itself, the yield gap between the currency you are long and the currency you funded with, and it accrues steadily as long as you hold. The second term is the spot move. Theory says the spot should move against you by roughly the differential (the high-yielder should depreciate enough to cancel the yield advantage), and in the long run and across the cleanest samples it partly does. In practice, for long stretches, it does not. The high-yielding currency appreciates instead of depreciating, so the spot term adds to the carry term rather than offsetting it. You get paid the differential and the currency goes up. Both terms positive, month after month.

The reason is flow, not fundamentals. The market prefers owning high-yielders and shorting low-yielders, so capital piles into the trade, and that buying pressure pushes the high-yielder up. The appreciation is structural, a crowd leaning the same way, and it persists because the carry keeps paying people to keep leaning. That is the escalator: the yield pickup plus the self-reinforcing appreciation the yield pickup creates.

The elevator

The structural appreciation is the same thing as crowded positioning, and crowded positioning unwinds violently. When risk appetite turns, traders cut the carry trade to reduce risk, which means selling the high-yielder and buying back the low-yielding funding currency. Everyone is on the same side, so the exit is a stampede through one door, and the spot term that spent two years quietly adding to your return flips to a large negative number in days. The low-yielders that funded the trade (the euro, the franc, the yen in recent cycles) are exactly the safe havens that get bought back in a panic, so the funding side and the risk-off flow reinforce each other. Down the elevator.

This produces the defining feature of carry: negative skew. The trade wins small and often and loses big and rarely. Picking up the differential day after day is collecting nickels; the unwind is the steamroller. Picking up nickels in front of a steamroller is a fine living until the day you misjudge the steamroller, and the strategy's smoothness is what lulls you into standing in front of it with size. A high Sharpe computed over a sample that has not yet contained a crash is measuring the escalator and pricing the elevator at zero.

Why volatility-targeting makes it worse

Here is the part that catches careful traders. The instinct from the old article "Why Volatility-Adjusted Position Sizing Matters" is to scale the position inversely to volatility, sizing up when the currency is calm and down when it is wild, so that every position contributes equal risk. For most strategies that discipline is the foundation. For carry it is a trap, because of when carry's volatility is low.

Carry's volatility is lowest during the long calm grind up the escalator, and it spikes only when the unwind has already begun. Inverse-volatility sizing therefore tells you to hold the largest position during the calm appreciation, which is precisely when the crowd is most leaned-in and the elevator is most loaded, and to cut only after volatility has jumped, which is after the crash has started. The sizing rule maximizes exposure into the steamroller and trims after the first wheel has passed.

$$ \text{position} \;\propto\; \frac{1}{\hat{\sigma}_t} \quad\Rightarrow\quad \hat{\sigma}_t \text{ low during the calm grind} \;\Rightarrow\; \text{position largest right before the unwind} $$

The position is set proportional to one over the estimated volatility, so when the estimate is low the position is large, and because carry's volatility is lowest just before the unwind, the rule puts on its biggest size at the worst possible moment. This is the lag problem the sizing article warned about, sharpened by carry's specific structure: volatility is an estimate that trails the truth, and for a negatively-skewed trade the gap between the calm estimate and the coming reality is the whole risk. The honest fixes are to cap carry exposure regardless of how calm volatility looks, to size off a stressed or floored volatility rather than the realized calm, and to treat the carry differential as the signal while letting a risk-off filter (the macro regime gate from "Why FX Traders Need Macro but Should Trade Systematically") pull exposure down before the volatility spike confirms what the macro already said.

Is it a strategy worth running

Carry has a real, persistent edge: it is compensation for bearing crash risk, a risk premium, and risk premia do not arbitrage away because someone has to be paid to hold the tail. Against this kind of strategy, run with naive sizing and no regime gate, I am skeptical, because the backtest that has not eaten a crash overstates the Sharpe and understates the drawdown, and the standard volatility-targeting that would protect a normal strategy actively harms this one. Run with crash awareness baked in (capped size, stressed-volatility sizing, a risk-off gate, diversification across funding and target currencies so the whole book is not one risk-appetite bet), it is a legitimate premium harvest. The difference between the two is not the signal. It is whether you respected the elevator while you were riding the escalator.

Visualizing the escalator and the elevator

KEY POINTS

- A carry trade borrows a low-yielding currency to buy a high-yielding one, earning the interest differential plus whatever the spot rate does over the holding period.

- Theory says the high-yielder should depreciate to cancel the yield edge. For long stretches it appreciates instead, because crowded positioning into the trade pushes it up, so both the carry term and the spot term pay you. That is the escalator.

- The structural appreciation is crowded positioning, and it unwinds violently when risk appetite turns. Selling the high-yielder and buying back the safe-haven funding currency happens through one door, so the spot term flips to a large loss in days. That is the elevator.

- Carry has negative skew: it wins small and often, loses big and rarely. Picking up the differential is collecting nickels in front of a steamroller, and the smooth ride is what lulls you into standing there with size.

- A high Sharpe measured over a sample with no crash is pricing the escalator and ignoring the elevator.

- Volatility-targeting betrays carry. Carry's volatility is lowest during the calm grind and spikes only after the unwind starts, so inverse-vol sizing holds the largest position right before the crash and cuts only after it begins.

- Run carry with crash awareness: cap exposure regardless of calm, size off stressed or floored volatility, use a risk-off macro gate to cut before the volatility spike confirms, and diversify funding and target currencies so the book is not one risk-appetite bet.

References

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Carry Trades and Currency Crashes

- The Global Factor Structure of Exchange Rates

- Currency Factors

- Common Factors in Currency Characteristics

- Carry Trades and Risk

- The Carry Trade: Risks and Drawdowns

- Carry Trades and Currency Crashes

- The Carry Trade and Fundamentals: Nothing to Fear But FEER Itself

- Carry Trades, Order Flow and the Forward Bias Puzzle

- Carry Trade and Systemic Risk: Why are FX Options so Cheap?

- The Carry Trade and Implied Moment Risk

- Jumps in Foreign Exchange Rates and Stochastic Unwinding of Carry Trades