4.56 A Short History of Floating FX and Why Central Banks Intervene

A floating currency is worth whatever the market believes today, with no commodity floor and no short-run fair value. Trade macro as a regime gate, and treat central-bank intervention as a jump risk your volatility estimate never saw.

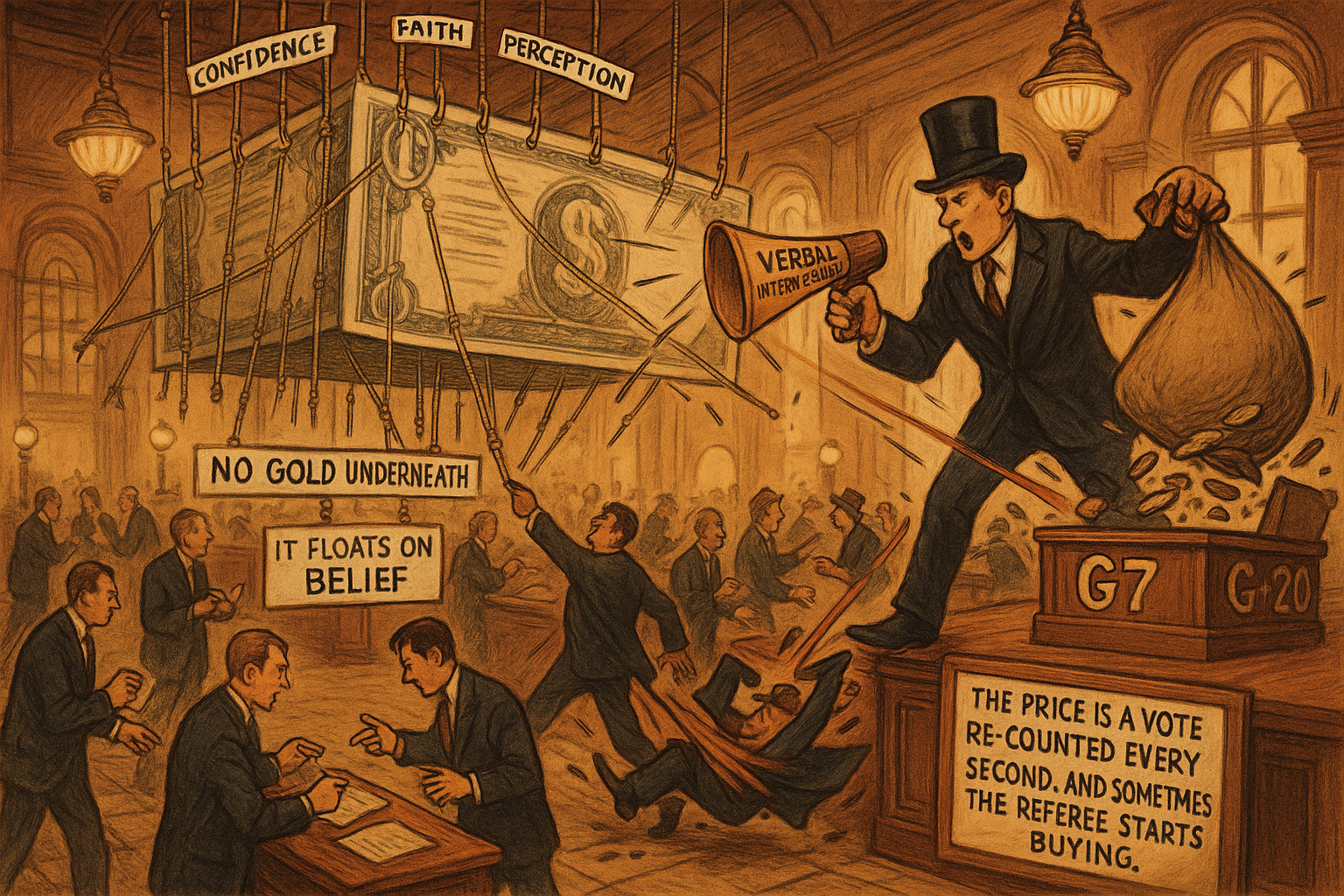

A dollar is worth something because the United States government says so, and enough of the world agrees to keep using it. There is no gold in a vault behind it, no commodity you can redeem it for, no intrinsic floor. The price of a currency is the market's running opinion of one country's relative value against another, and that opinion is the only thing holding the number up. A trader who forgets this builds models that assume a currency behaves like an asset with fundamentals. It does not. It behaves like a vote that gets re-counted every second, and occasionally the vote-counter steps onto the floor and starts buying.

This is worth understanding before you trade FX systematically, because two features of the modern currency system create risks that equity and futures models do not carry: the value is faith-based and floats freely, and a small set of very large players can intervene to move it on purpose. The first means there is no valuation anchor to lean on in the short run. The second means the price process has a jump risk that no historical volatility estimate will warn you about, because the jump is a policy decision and not a market event.

Faith, not gold

The currencies you trade run on a fiat system. "Fiat" means the money is legal tender by government decree, backed by confidence in the issuing country rather than by any redeemable commodity. Before the 1970s the major currencies were pegged through a gold-anchored arrangement, and the exchange rate was a fixed administrative number. When that broke down the majors began to float, and their value has been set by the market ever since, rising and falling on the market's perception of relative value between two economies.

The practical consequence for a system is that a currency has no standalone fundamental to mean-revert toward on any tradeable horizon. A stock has earnings and a book value. A bond has a coupon and a face value. A currency pair is one economy priced against another, and the "fair value" anchors that exist, purchasing power parity and the like, operate on horizons of years and get overwhelmed by positioning and flow in the short run. A model that treats a currency level as cheap or rich the way it would treat a stock is fighting the float. The level can stay "wrong" far longer than any position can survive, which is the macro-but-systematic discipline argued in the old article "Why FX Traders Need Macro but Should Trade Systematically": use macro to read the regime, not to call a currency mispriced and wait for justice.

The players who can move it on purpose

The float is not a free-for-all. The G7 and the wider G-20 monitor currency levels, and when they judge a currency badly misaligned they intervene, either verbally or directly. This is the decentralized structure described in the old article "FX Is Not One Market: Retail vs Wholesale Structure" with one extra wrinkle: among the wholesale players sits a participant who is not trying to make money and does not face a risk limit. A central bank intervening to defend or weaken its currency will trade size that no profit-seeking desk would, in the direction it has chosen, for reasons that have nothing to do with your signal.

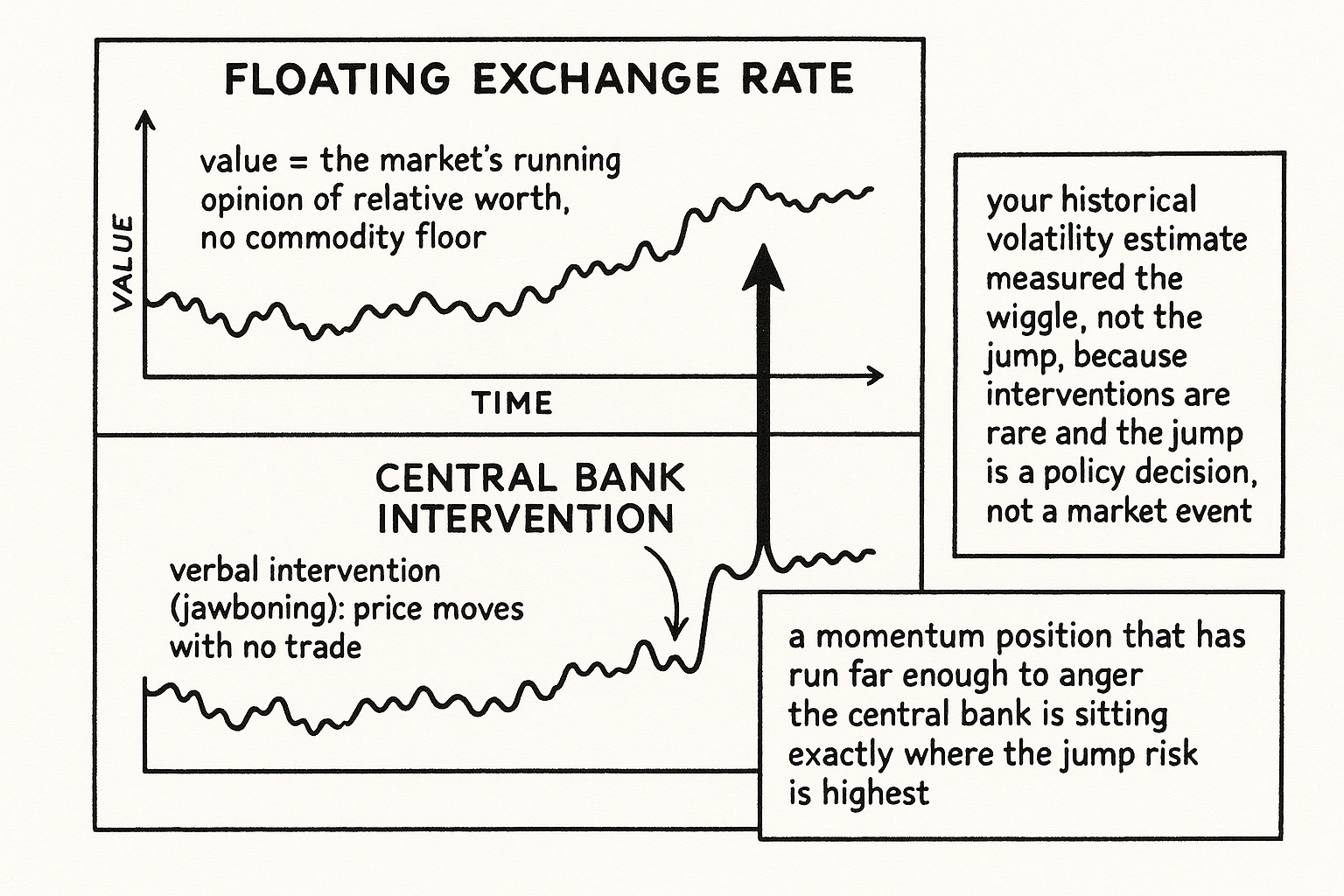

Intervention comes in two strengths. Verbal intervention, often called jawboning, is an official statement that a currency is too strong or too weak. It moves the price with no trade at all, because the market front-runs the threat of action. Direct intervention is the central bank actually buying or selling its currency in the market, sometimes alone, sometimes coordinated across several central banks at once. Coordinated intervention is the dangerous version, because the combined size can move a major pair several percent in minutes and reverse a trend that every momentum model was happily riding.

Why a system should treat intervention as jump risk

Model a currency price as a normal diffusion most of the time, with an occasional jump bolted on:

$$ \Delta P_t = \underbrace{\mu\,\Delta t + \sigma\,\varepsilon_t}_{\text{ordinary market}} \;+\; \underbrace{J_t}_{\text{intervention jump}} $$

The first part is the ordinary market: a drift term and a volatility term driven by normal flow, the part your historical volatility estimate measures. The second part is the jump, a sudden displacement that fires when a central bank acts or threatens to act. The jump is the problem, because it is absent from almost all of your sample (interventions are rare), so your estimated volatility carries almost no information about it, and it arrives precisely in the pairs and moments where a central bank has a policy reason to care, which is not random with respect to your positions. A momentum system long a currency that has run far enough to anger its central bank is sitting in the exact spot where the jump risk is highest, and the historical vol it used to size the position never saw the jump coming.

This is why intervention belongs in the risk model and not the signal model. You will not predict the jump, because it is a discretionary policy choice, so do not try to trade it as a forecast. You can defend against it. Cap position size in pairs with a history of intervention or an active policy band (the yen, the franc in its peg years, several emerging-market currencies), respect that a stop-loss is a market order that slips badly through a gap, the execution reality from the order-type discussion in this pillar, and treat any currency that has appreciated or depreciated into a level officials keep complaining about as carrying a fat left tail that your Gaussian sizing understates. The minor, optional payoff is that a credible verbal threat sometimes marks a usable turning point, but that is a discretionary macro read, not a systematic edge, and it sits inside the same regime gate the macro article insisted on.

Visualizing the float and the jump

KEY POINTS

- Modern currencies run on a fiat system: their value is backed by confidence in the issuing country, not by gold or any redeemable commodity, and the majors have floated freely since the 1970s.

- A floating currency has no standalone fundamental to mean-revert toward on a tradeable horizon. Valuation anchors like purchasing power parity work over years and get overwhelmed by positioning and flow in the short run.

- Use macro to read the regime, not to declare a currency mispriced and wait, because a floating level can stay "wrong" far longer than a position can survive.

- The G7 and G-20 intervene when they judge a currency badly misaligned, either verbally (jawboning, which moves price with no trade) or directly (the central bank buying or selling its own currency).

- Coordinated intervention across several central banks can move a major pair several percent in minutes and reverse a trend every momentum model was riding.

- Treat intervention as a jump risk in the risk model, not a signal. It is absent from most of your sample, so historical volatility understates it, and it fires in the pairs and moments where officials have a policy reason to act.

- Defend against it: cap size in intervention-prone pairs, respect that stops slip through gaps, and treat a currency that has run into a level officials keep complaining about as carrying a fat tail your Gaussian sizing misses.

References

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- The Microstructure of Foreign Exchange Markets

- Dollar Dominance in FX Trading

- Imperfect Exchange Rate Expectations

- The Global Factor Structure of Exchange Rates

- Foreign Exchange Intervention Redux

- Japanese Foreign Exchange Interventions, 1971–2018

- Foreign-Exchange-Market Operations in the Twenty-First Century

- Exchange Arrangements Entering the 21st Century: Which Anchor Will Hold?

- Exchange Rate Anchoring – Is There Still a de facto US Dollar Standard?

- Why Do Countries Peg the Way They Peg? The Determinants of Anchor Currency Choice

- Floating Exchange Rates, Expectations and New Information

- Empirical Studies of Exchange Rates: Price Behavior, Rate Determination and Market Efficiency