4.55 Currency Quoting Conventions: Numerator, Denominator, and the Priority Order

A currency pair is one ratio with two ways to write it, and the priority order decides which. Get the convention wrong and your backtest silently flips half your signs and converts your PnL into the wrong currency.

Two traders look at the euro. One has it at 1.0850, the other at 0.9217, and both are right. The first quotes EURUSD (dollars per euro), the second quotes USDEUR (euros per dollar), and the two numbers are reciprocals of the same exchange rate. A stock has one price. A currency pair has two ways to write the same price, and which way you write it decides where your profit lands, what your pip is worth, and whether your backtest computed a long or a short. Getting the convention wrong does not throw an error. It silently flips the sign on half your trades and you find out in the equity curve.

Every exchange rate is a ratio of two currencies, a numerator over a denominator, and the market settled on a fixed rule for which currency goes on top. The rule is not arbitrary taste. It exists so that one bank quoting to another never has to ask "which way are we quoting this," because the answer is already fixed by convention. This article makes that convention explicit, shows the priority order that decides every major pair, and connects it to the two places it bites a systematic trader: the sign of the position and the currency the PnL arrives in.

A pair is a ratio, and the order is not free

Write a pair as X/Y. The price is how many units of Y it takes to buy one unit of X. EURUSD at 1.0850 means one euro costs 1.0850 dollars. X (the euro) is the base currency, the thing you are pricing. Y (the dollar) is the quote currency, the thing you are pricing it in. Buy the pair and you are long X, short Y; you own euros financed by selling dollars.

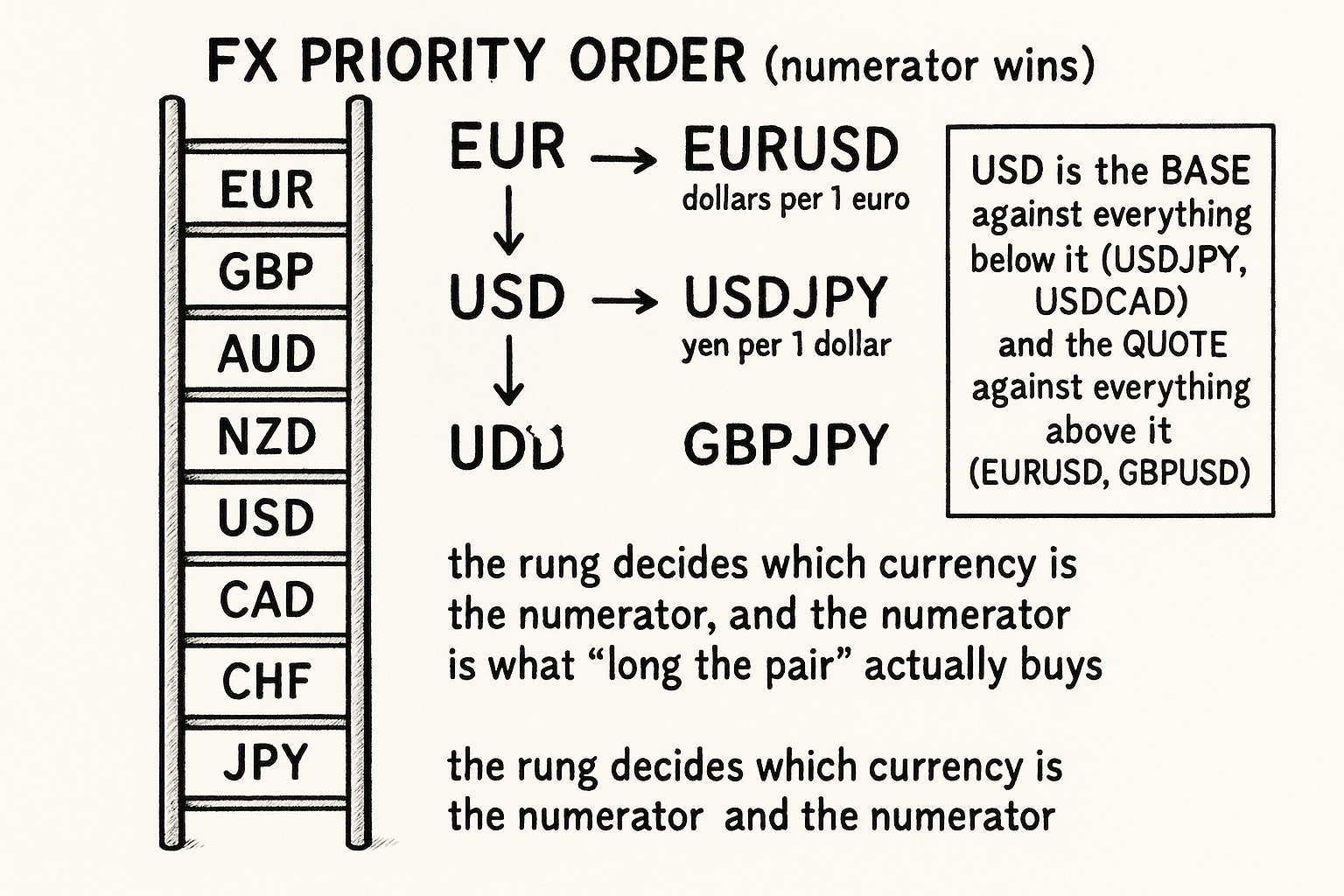

The decision of which currency becomes X and which becomes Y is fixed by a priority order. The stronger-ranked currency goes in the numerator. The market convention runs:

$$ \text{EUR} \succ \text{GBP} \succ \text{AUD} \succ \text{NZD} \succ \text{USD} \succ \text{CAD} \succ \text{CHF} \succ \text{JPY} $$

Read the ranking as "outranks." When you form a pair from two currencies, the one further left becomes the base (numerator) and the one further right becomes the quote (denominator). The euro outranks everything, so it is always the base: EURUSD, EURGBP, EURJPY. The yen sits at the bottom, so it is always the quote: USDJPY, GBPJPY, AUDJPY. The dollar sits in the middle, which is why it shows up as the base against the currencies below it (USDJPY, USDCAD, USDCHF) and as the quote against the currencies above it (EURUSD, GBPUSD, AUDUSD). The convention is what makes a trader say "cable" and know without asking that it means GBPUSD and not USDGBP.

This is also the origin of the American-versus-European terms distinction. A pair quoted with the dollar in the denominator (EURUSD, GBPUSD) is in American terms: the price is dollars per unit of foreign currency. A pair quoted with the dollar in the numerator (USDJPY, USDCHF) is in European terms: the price is foreign currency per dollar. Same dollar, two sides of the ratio, and the priority order is what decides which side it lands on for any given pair.

The sign trap in a backtest

The convention matters to a system because the base currency defines the direction of a long. Long EURUSD is long euros against dollars. Long USDJPY is long dollars against yen. If your signal generator decides "buy the dollar" and you express it by going long whatever pair the dollar appears in, you will be correct on USDJPY (dollar is the base, long the pair is long the dollar) and exactly backward on EURUSD (dollar is the quote, long the pair is short the dollar). The same dollar view produces opposite positions depending on where the priority order parked the dollar in each pair.

This is the mechanical reason a currency-strength view has to be translated through the quoting convention before it becomes an order, the same decoupling problem worked in the old article "Currency Strength Models from Pair Decomposition." A strength model hands you a view on the currency. The convention tells you the sign to trade in each pair that contains it. Skip the translation step and the backtest runs clean, throws no error, and reports a sign-scrambled equity curve that looks like noise because half the trades are inverted.

The defense is boring and non-negotiable: store every pair in a canonical orientation, decide the sign of the position in terms of the base currency, and never let the signal code touch a pair without knowing which currency sits in the numerator.

Where the PnL lands

The second consequence is that profit accrues in the quote currency, the denominator, which is not always your account currency. This is the mechanics worked in full in the old article "How FX PnL Actually Works," and the quoting convention is what determines it. PnL comes out in units of Y, and you may have to convert.

$$ \text{PnL} = \text{Position size} \times \Delta P \quad \text{(in units of the quote currency Y)} $$

Take EURUSD for a dollar-denominated account. A one-million-euro position that moves 20 pips earns 0.0020 times one million, or 2,000 dollars, and because the quote currency is the dollar the profit is already in your account currency. One step. Now take USDJPY for the same dollar account. A ten-million-dollar position that moves five pips earns 0.05 times ten million, or 500,000 yen, because the quote currency is the yen. To know that in dollars you divide by the current rate: 500,000 divided by roughly 101.65 is about 4,956 dollars. Two steps, and the pip is not even worth a constant number of dollars over the life of the trade, because the conversion rate moves while you hold.

The systematic consequence is that "dollars per pip" is not a property of the pair, it is a property of the pair times your account currency times the current rate. A book that sizes every pair off one fixed dollars-per-pip number is not running equal risk across pairs, it is running whatever risk the quoting convention and the conversion rate happen to hand it. Equal-risk sizing has to convert each pair's pip value into the account currency first, which is the input the volatility-scaling in the old article "Why Volatility-Adjusted Position Sizing Matters" assumes you already computed correctly.

Visualizing the priority ladder

KEY POINTS

- Every exchange rate is a ratio X/Y, read as units of the quote currency Y per one unit of the base currency X. EURUSD at 1.0850 means one euro costs 1.0850 dollars.

- Which currency becomes the base is fixed by a priority order, EUR over GBP over AUD over NZD over USD over CAD over CHF over JPY, with the higher-ranked currency taking the numerator.

- The dollar sits in the middle of the ladder, so it is the base against the currencies below it (USDJPY, USDCAD, USDCHF) and the quote against the currencies above it (EURUSD, GBPUSD, AUDUSD). That split is the American-versus-European terms distinction.

- Long a pair means long the base, short the quote. A single "buy the dollar" view produces a long in USDJPY and a short in EURUSD, so a strength view must be translated through the convention before it becomes an order.

- The sign trap is silent: trading the dollar long in every dollar pair inverts half your positions, runs without error, and shows up only as a scrambled equity curve.

- PnL accrues in the quote currency. EURUSD profit lands in dollars in one step; USDJPY profit lands in yen and needs a second conversion step, and the pip value drifts with the conversion rate.

- "Dollars per pip" is not a constant of the pair. Equal-risk sizing has to convert each pair's pip value into the account currency before volatility scaling, or the book quietly over-weights whatever pair the convention favored.

References

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- The Microstructure of Foreign Exchange Markets

- Dollar Dominance in FX Trading

- The Global Factor Structure of Exchange Rates

- Foreign Exchange Volume: Sound and Fury Signifying Nothing?

- Introduction to Foreign Exchange (excerpt from "FX Derivatives Trader School")

- Just Another Day in the Inter-Bank Foreign Exchange Market

- Liquidity in the Global Currency Market

- Does the Law of One Price Hold in International Financial Markets? Evidence from Tick Data

- Price Discovery in Currency Markets

- Analysis of Spreads in the Dollar/Euro and Deutschemark–Dollar Foreign Exchange Markets

- Order Flow and Exchange Rate Comovement

- Short-Term Trading Strategy on G10 Currencies