6.3 Why Volatility-Adjusted Position Sizing Matters

Equal dollars isn't equal bets; the loudest instrument owns your P&L. Size inversely to volatility so each position carries the same risk, and the volatility you scale by is only an estimate.

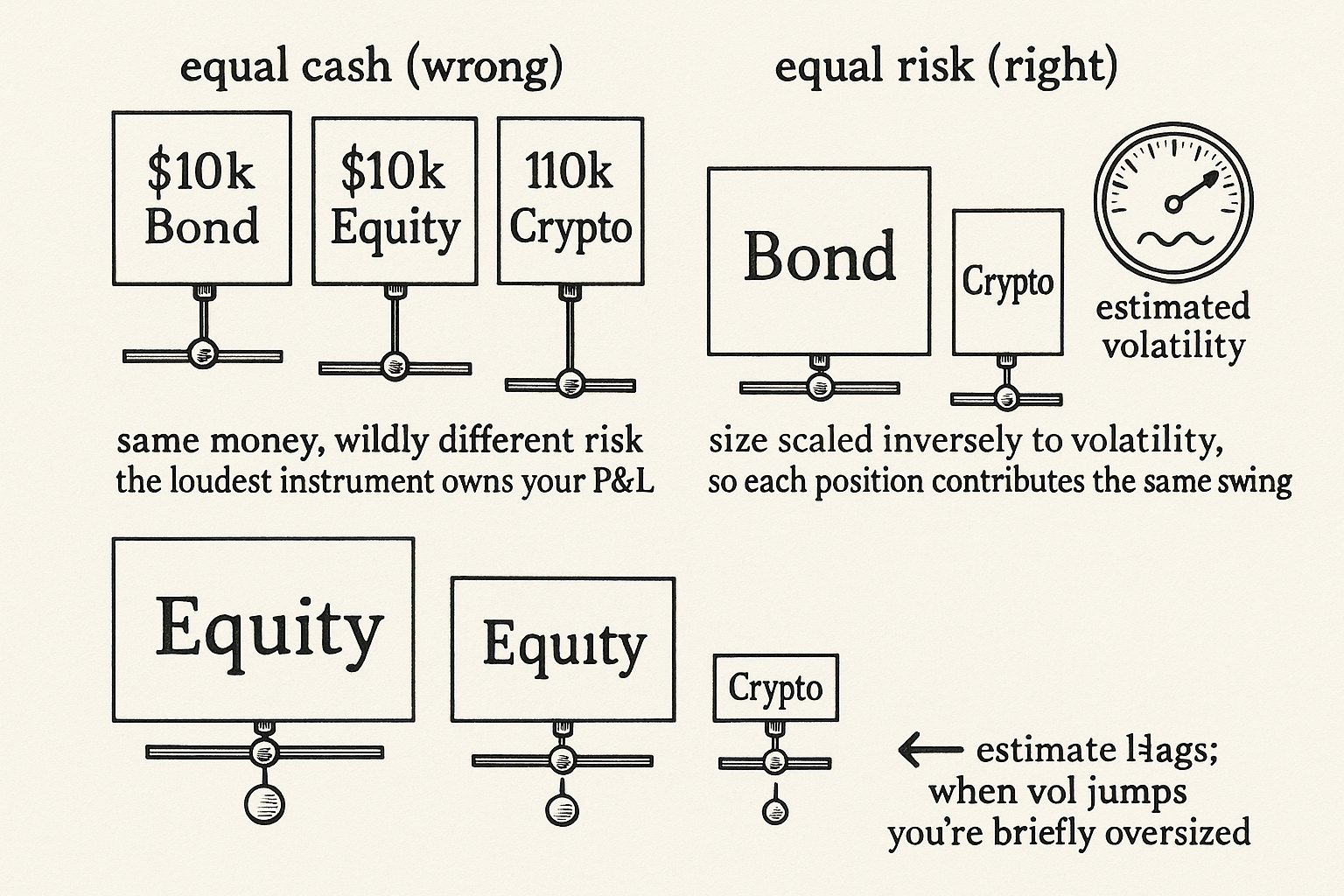

Put the same dollar amount into a Treasury future and a Bitcoin perp and you have not made two equal bets. You have made one tiny bet and one enormous one, because the Bitcoin position swings ten or twenty times harder per day than the bond. Equal dollars is the most common sizing mistake in retail trading, and it guarantees that your risk, your profit, and your pain all come from whichever instrument happens to be the most volatile, regardless of which one you actually had a view on. Volatility-adjusted sizing fixes this by sizing in units of risk instead of units of cash.

This is the sizing layer that "Ranking Beats Forecasting for Many Trading Problems" deliberately left out. Ranking picks what to hold; this decides how much.

Equal risk, not equal cash

The fix is to scale each position inversely to its volatility, so a more volatile instrument gets a smaller position and a calmer one gets a larger position, and both end up contributing the same risk to the book. You decide once how much risk you want each position to carry, expressed as a target volatility, and then you back out the position size that delivers it.

$$ N_i = \frac{\tau \cdot \text{Capital}}{\sigma_i \cdot \text{(price} \times \text{point value)}_i} $$

The position size in contracts is the risk target (an annualized volatility you want the position to run, say 20%) times your capital, divided by the instrument's annualized price volatility times the cash value of one point of price movement. The numerator is how much risk in dollars you are willing to spend on this position; the denominator is how much risk one contract delivers. Divide and you get the number of contracts that hits your target. A high-volatility instrument has a large volatility, which shrinks the position; a low-volatility one has a small volatility, which inflates it. Every position, after the scaling, contributes the same expected swing.

Why this is the foundation, not a refinement

Without volatility scaling, every other part of your system is quoting into the dark. A ranked long/short book that sizes by equal cash is not actually market-neutral, because the high-volatility names dominate both the long and short legs and the supposed hedge is lopsided. A forecast that says "lean twice as hard on copper as on gold" means nothing in dollar terms until you express both in the same risk units, which is exactly why a disciplined framework standardizes every forecast to a common volatility scale before combining them. Volatility scaling is the common currency that lets you compare a bond signal to a crypto signal to an equity signal on one desk. Skip it and the comparisons are meaningless, no matter how good the underlying signals are.

The catch: volatility is estimated, and it moves

Volatility scaling rests on the volatility estimate, and you never know the true volatility; you estimate it from recent history, and the estimate is always a little stale and a little wrong. When volatility jumps, your estimate lags, so for a window you are running larger positions than your target intends, right when the market is most dangerous. When volatility collapses, you lever up into calm that may be the eye of a storm. The standard mitigations, an exponentially weighted estimate that reacts faster, a blend of recent and long-run volatility, a floor under the estimate so a quiet patch does not let you take grotesque size, all help and none of them make the estimate correct. You are sizing off a moving target, and the discipline is to respect that the number is an estimate, not to pretend a fancier estimator makes it exact.

Visualizing volatility scaling

KEY POINTS

- Equal dollars is not equal bets. A high-volatility instrument swings many times harder than a calm one, so equal cash makes your risk and P&L come from whichever instrument is loudest, not the one you had a view on.

- Volatility-adjusted sizing scales each position inversely to its volatility so every position contributes the same risk. You pick a volatility target once and back out the position size that delivers it.

- The size in contracts is the risk target times capital, divided by the instrument's price volatility times the cash value of a one-point move. Numerator is risk you will spend; denominator is risk one contract delivers.

- This is the foundation, not a refinement. Without it a ranked book is not really neutral, and forecasts that say "lean twice as hard here" are meaningless until expressed in common risk units.

- Volatility scaling is the common currency that lets you compare a bond, an equity, and a crypto signal on one desk. Skip it and the comparisons are meaningless.

- The catch: volatility is estimated and lags. When it jumps you are briefly oversized into danger. Faster estimators, blends, and floors help but never make the estimate exact, so respect that it is an estimate.

References

- Systematic Trading - Robert Carver (Amazon)

- Trading Systems - Urban Jaekle Emilio Tomasini (Amazon)

- Trade Sizing Techniques for Drawdown and Tail Risk Control

- Optimal Portfolio Strategy to Control Maximum Drawdown

- Leverage for the Long Run

- Factor Investing and Asset Allocation

- Behavioral Finance: Theories and Evidence

- Behavioral Finance

- Maximum Drawdown, Recovery, and Momentum

- A Primer for Investment Professionals: Portfolio Construction and Analytics

- Kelly, VIX, and Hybrid Approaches in Put-Writing on Index Options

- Volatility-Parity Sizing (section in: Small-Cap Stock Trading Strategies for Retail)

- Trend Following, Risk Parity and Momentum in Commodity Futures

- Risk Parity: Equal Risk Contributions in Practice

- The Carry Trade: Risks and Drawdowns

- The Common Stock Investment Performance of Individual Investors

- Kelly, VIX, and Hybrid Approaches in Put-Writing on Index Options

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.