4.31 Why FX Traders Need Macro but Should Trade Systematically

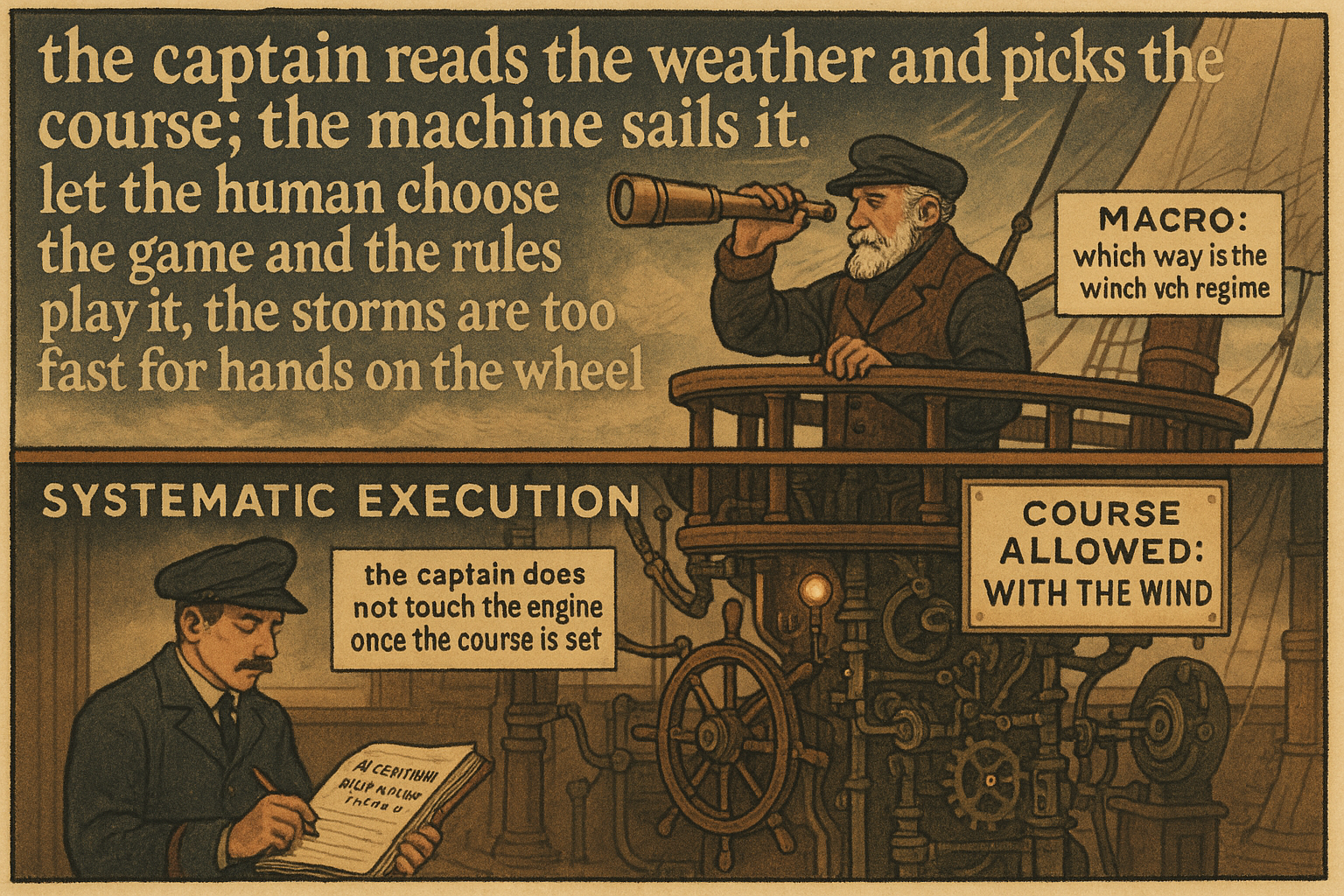

A correct macro view traded by hand still loses to your own cognitive defects. Keep macro as a regime gate and hand execution to rules: macro chooses the game and direction, the system plays it.

A trader reads everything: the central-bank statements, the rate-differential charts, the risk-appetite gauges, the gold and crude tape. The macro view is sharp and correct, the dollar should weaken. Then the trader sits at the screen and discretionarily trades that view, and loses money, because the view was right about the destination and wrong about the path, and the trader's brain closed the winners early and held the losers waiting for vindication. Macro told the truth and discretion squandered it. The resolution is not to drop the macro and not to trust the gut. It is to keep the macro as context and hand the execution to rules.

FX sits in a hard spot. The market is non-stationary, the rules of the game keep changing, and a technique that works for a while stops working, so no fixed system is permanent. Macro understanding is what tells you which regime you are in and which way the structural forces lean. But macro understanding executed by hand collides with the same cognitive defects that wreck every discretionary trader. The synthesis is macro-informed, systematically-executed: let the macro set the context and the gates, and let a rule-based system pull the trigger.

This article closes the FX run of Pillar 4 by reconciling the macro content of "Why FX Traders Must Watch Gold, Rates, and Equities" with the systematic discipline of "Trading Systems Are Recipes, Not Predictions". It is the bridge between the intermarket and microstructure halves of the pillar and the trader's actual workflow.

Why you need the macro

A currency is a relative macro object with no standalone fundamentals, so the forces that move it are macro by nature: rate differentials, risk appetite, commodity terms of trade, capital flows. Ignoring them and trading EURUSD off the chart alone is trading the shadow, the point the FX-drivers article made. The macro view tells you which way the structural wind blows and, more importantly, which regime you are in, because the driver that matters rotates: in a risk-off panic, domestic fundamentals become irrelevant and global risk appetite drives everything; in calm times, local rate expectations take over.

Macro also sets the time horizon honestly. In the short run the market is a voting machine, driven by positioning and momentum and emotion; in the long run it is a weighing machine, pulled toward fundamental value. Valuation measures like purchasing power parity only matter over the super-long term and are nearly useless for trading horizons, because a currency can stay cheap or rich far longer than you can hold the position. Macro's job is not to time entries; it is to tell you which regime and horizon you are operating in, so you run the right system.

Why you should not trade it by hand

The macro view is necessary and discretionary execution of it is where the money leaks, for the reasons the article "Trading Systems Are Recipes, Not Predictions" laid out. A correct macro thesis still has to survive a noisy path, and the human in the loop systematically mishandles the path: taking small profits to feel right, holding losers to avoid being wrong, oversizing the trades they feel strongest about (which are not the ones that pay best), and abandoning the thesis at the worst moment. The macro can be right and the discretionary P&L still negative, because the errors are in the execution, not the analysis.

The non-stationarity makes it worse. Because the rules change and techniques decay, a discretionary trader is constantly tempted to override the plan with the latest narrative, and the override is usually the cognitive defect wearing a macro costume. "This time the dollar will ignore rates because of the new narrative" is exactly the kind of mid-trade rationalization that a systematic process exists to prevent. Adapt or die is true at the level of redesigning systems between sessions with data; it is a disaster as a license to improvise inside a live trade.

The synthesis: macro sets the gate, rules pull the trigger

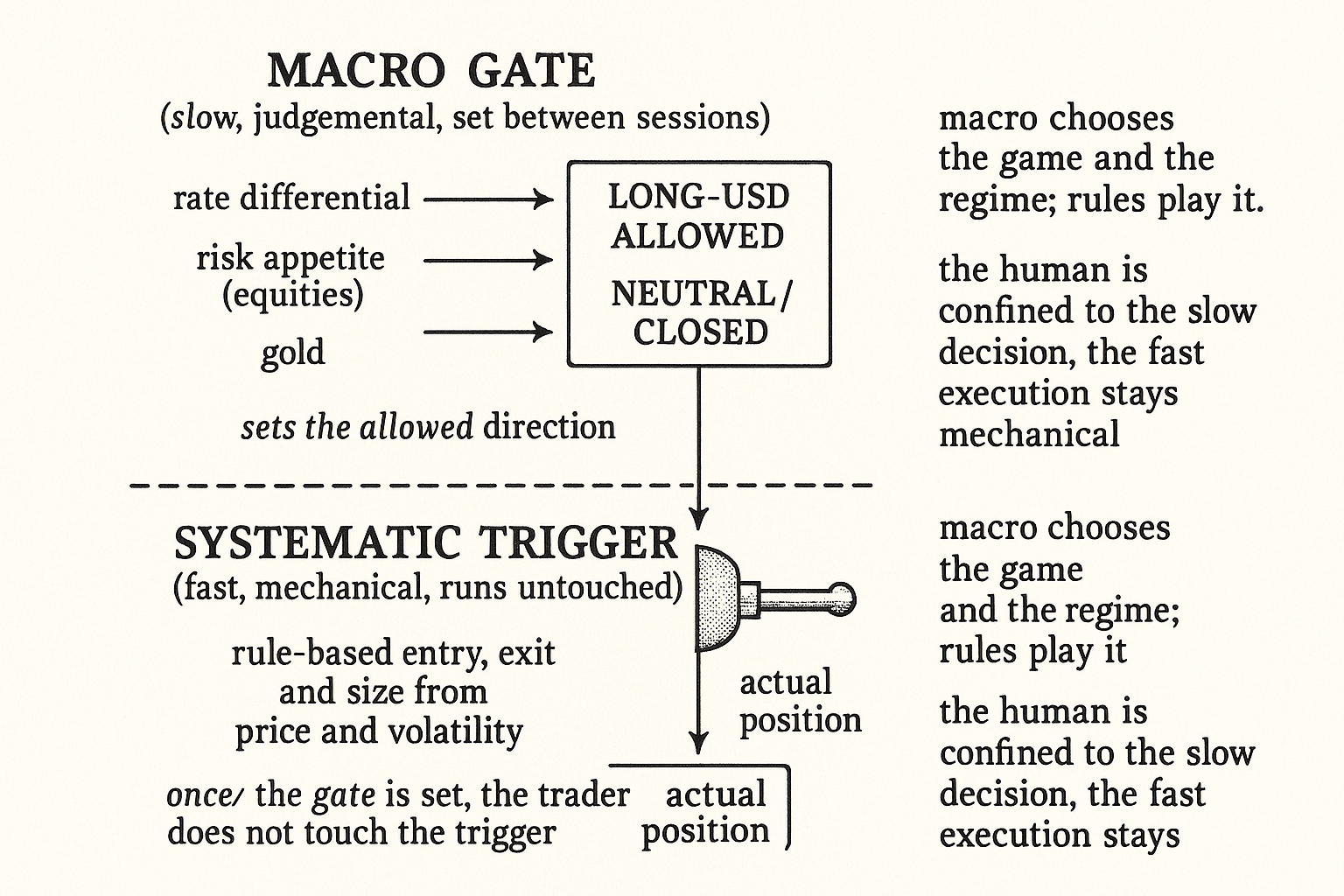

The workable structure separates the two jobs cleanly. Macro analysis defines the regime and the allowed direction; a rule-based system generates the entries, exits, and sizing within that allowance. Macro is the gate; the system is the trigger.

$$ \text{Position}_t = \text{Gate}_{\text{macro}}(\text{regime, direction}) \times \text{Signal}_{\text{rules}}(\text{price, vol}) $$

The position is the macro gate (a regime-and-direction allowance, often just a plus-one, zero, or minus-one that says which way you are permitted to trade) multiplied by the systematic signal (the rule-based entry and size from price and volatility). When the macro gate says "dollar bearish regime," the system is allowed to take its short-dollar signals and forbidden from going long; when the macro is neutral or conflicted, the gate narrows or closes. The macro never sets the entry price or the stop; the rules never decide the regime. Each does the job it is good at, and neither is allowed to do the job it is bad at.

This is the same two-layer structure as the confirmation count in "Why FX Traders Must Watch Gold, Rates, and Equities" and the regime gate in "Matching Strategy Families to Market Conditions", generalized to the macro-versus-systematic split. The macro layer is slow, judgmental, and updated between sessions; the systematic layer is fast, mechanical, and runs without intervention. The discipline is that once the gate is set, the trader does not touch the trigger.

Making the gate itself systematic

The honest extension: the more of the macro gate you can encode in rules, the fewer places discretion can leak in. The drivers from the FX-macro article (the rate differential, the risk-appetite proxy, gold) are measurable, so the gate can be a rule too: dollar-bearish regime when the rate differential is narrowing and gold is rising and equities are firm, for instance. Encoding the gate turns the whole stack systematic and lets you backtest the macro overlay instead of trusting it on faith, the testability the article "Optimization Comes After Testing, Not Before" demanded.

Some macro judgment resists encoding (a genuine geopolitical regime break, a central-bank stance shift the data has not yet shown), and there the human still sets the gate. That residual discretion is the smallest possible surface for error: a slow, between-sessions regime call, not a fast, in-trade override. The goal is not to eliminate the human, which is impossible in a non-stationary market that requires adaptation, but to confine the human to the slow, high-level decision and keep the fast, error-prone execution mechanical. Macro to choose the game, rules to play it.

Visualizing the two-layer workflow

KEY POINTS

- A correct macro view executed by hand still loses money, because the human mishandles the noisy path: taking profits early, holding losers, oversizing favorite trades, and abandoning the thesis at the worst time. Macro can be right and discretionary P&L still negative.

- A currency is a relative macro object, so you need the macro: rate differentials, risk appetite, commodities, and flows. The driver that matters rotates by regime, and macro's job is to tell you which regime and horizon you are in.

- In the short run the market is a voting machine (positioning, momentum, emotion); in the long run a weighing machine (fundamental value). Valuation like purchasing power parity only matters over the super-long term and is useless for trade timing.

- You should not trade the macro by hand. Non-stationarity tempts constant overrides, and the override is usually a cognitive defect in a macro costume. "Adapt or die" means redesigning systems between sessions with data, not improvising inside a live trade.

- The synthesis: macro sets the gate (regime and allowed direction), and a rule-based system pulls the trigger (entry, exit, size). The position is the macro gate times the systematic signal.

- Each layer does what it is good at: macro is slow, judgmental, updated between sessions; the system is fast, mechanical, and runs without intervention. Once the gate is set, the trader does not touch the trigger.

- Encode as much of the gate as possible in rules, since the drivers are measurable, which makes the macro overlay backtestable instead of faith-based and shrinks the surface for discretionary error.

- Residual judgment that resists encoding (a geopolitical break, an un-priced policy shift) stays human, but confined to the slow, high-level regime call. Macro to choose the game, rules to play it.

References

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Market Macrostructure: Institutions and Asset Prices

- The FX Race to Zero: Electronification and Market Structural Issues

- FX 101 – Technical Analysis of the Currency Market (chapter on FX market structure)

- Market Microstructure Across Centralised and Decentralised Trading Venues

- A Panel Project on Purchasing Power Parity: Mean Reversion within and between Countries

- Purchasing Power Parity (PPP) in the Long Run

- Market Microstructure Noise and Volatility

- Technical Trading Rule Profitability and Foreign Exchange Intervention

- Macroeconomic announcements and price discovery in the foreign exchange market

- Informed trade in spot foreign exchange markets: An empirical investigation

- The Foreign Exchange Market (Handbook of Fixed-Income Securities chapter)

- Local information in foreign exchange markets

- Asymmetric information risk in FX markets

- Markov switching regimes in a monetary exchange rate model

- Machine Traders, Human Behavior, and Model (Mis)Specification

- Human vs. Machine: Rationality in Algorithmic Decision-making

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.