4.32 Using Gold as an FX Indicator

Gold is the dollar seen in a mirror, reading the common factor inside every USD pair. Use it as a dollar confirmer, cross-check real yields, and respect the crisis regime where the mirror breaks.

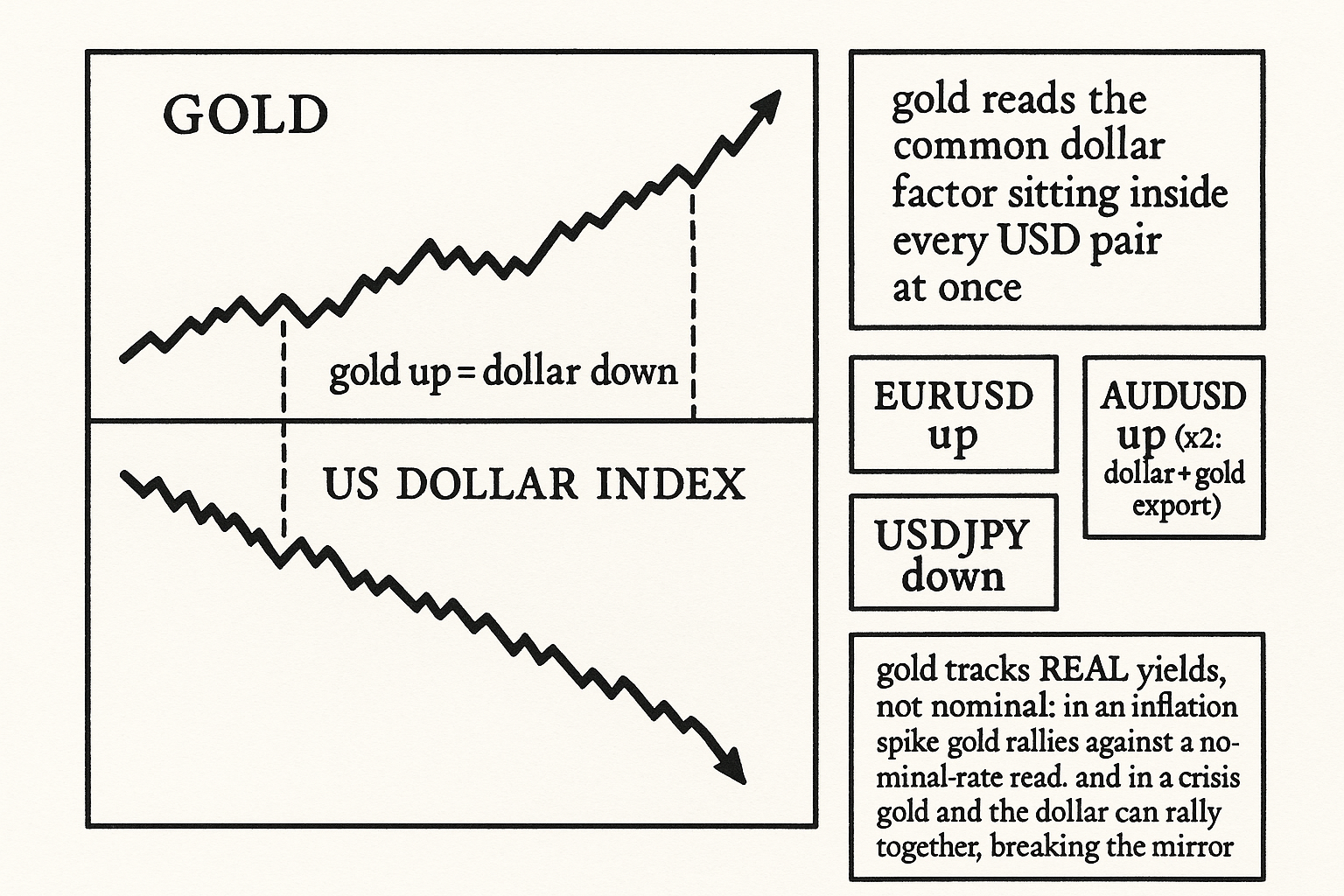

Pull up the driver list for almost any major currency pair and gold is on it. EURUSD, USDJPY, USDCHF, AUDUSD, USDCAD: gold shows up again and again, which is strange at first glance, because gold is not a currency and most of these pairs have no direct gold connection. The reason gold belongs on all of them is that gold reads the one thing every USD pair shares: the dollar. Gold trades inverse to the dollar, so a move in gold is a move in the dollar seen from a different angle, and that makes gold a single instrument you can watch to read the common factor sitting inside every dollar pair at once.

Gold carries a second signal on top of the dollar one. It anticipates inflation and tracks real yields, so gold strength flags either a weakening dollar or a rising inflation-and-easing backdrop, both of which matter for FX. For one currency, the Australian dollar, gold is also a direct export, so it acts through a second channel as a commodity input. One instrument, three overlapping readings: the dollar, the inflation-and-rate backdrop, and the commodity terms of trade for the gold exporters.

This article turns gold into a concrete FX indicator, drawing the dollar link from "Gold, Dollar, and Rates: A Practical Intermarket Map" and the driver framing from "Why FX Traders Must Watch Gold, Rates, and Equities". It is the gold-specific deep cut of the FX-macro arc, and it leads into the cross-pair and currency-strength articles that close the pillar.

Gold as the dollar barometer

The cleanest use of gold in FX is as a dollar proxy. Gold is priced in dollars and competes with the dollar as a store of value, so the two trade inverse across most regimes. When gold rises, the dollar is usually weakening, and that weakening shows up across every dollar pair at once.

$$ \text{gold} \uparrow \;\Rightarrow\; \text{USD} \downarrow \;\Rightarrow\; \{\,\text{EURUSD} \uparrow,\;\; \text{AUDUSD} \uparrow,\;\; \text{USDJPY} \downarrow\,\} $$

Rising gold signals a weaker dollar, which lifts the pairs where the dollar is the quote currency (EURUSD, AUDUSD rise) and lowers the pairs where the dollar is the base (USDJPY falls). The direction flips with the dollar's position in the pair, but the underlying read is one number: gold up means dollar down, applied to whichever side of the pair the dollar sits on. A trader watching gold is watching the dollar's common factor without having to average a basket of dollar pairs by hand.

This makes gold a natural confirmer for any dollar trade, the confirmation logic from "Cross-Asset Confirmation for Trend Systems" applied to the dollar leg. A short-dollar signal taken while gold is breaking higher is backed by the gold tape; the same signal with gold falling is fighting it, the divergence read from "Intermarket Divergence as a Trading Filter".

The inflation and real-yield reading

Gold's second signal is the inflation-and-rate backdrop, and it carries the same subtlety the triangle article flagged: gold tracks real yields, not nominal ones. Rising real yields (nominal rates climbing faster than inflation) hurt gold, because the opportunity cost of holding a zero-yield asset rises. Falling or negative real yields help it.

For FX this matters because real yields drive currencies through the rate-differential channel. A gold rally on falling real yields is consistent with a dovish, currency-weakening backdrop for the dollar; a gold selloff on rising real yields is consistent with a hawkish, dollar-strengthening one. The trap is the inflation-spike case: nominal yields can rise while real yields fall, and gold rallies against what a trader watching the nominal ten-year expects. A gold-based FX read built on nominal rates misfires in exactly the high-inflation regimes where the signal matters most, so the honest version uses a real-yield or breakeven proxy alongside gold.

The commodity-currency channel

For the Australian dollar, gold is not only a dollar barometer but a direct export, so it acts through a second, reinforcing channel. Rising gold improves Australia's terms of trade and supports the currency on top of the dollar-weakness effect, which is why AUDUSD is one of the more gold-sensitive pairs. The gold-miner equity index sits adjacent to this: miner stocks track gold and, historically, the European currency too, because they discount the future gold price the currency-and-commodity complex responds to.

The practical caution is not to double-count. For AUDUSD a gold rally pushes the same direction through both the dollar channel and the export channel, so the signal is strong but the two channels are correlated, not independent, the confirmation-count caveat from "Why FX Traders Must Watch Gold, Rates, and Equities". For a pair with no commodity link to gold (EURUSD), only the dollar channel operates, so gold is a pure dollar read there and nothing more. Knowing which channels apply to which pair is what keeps the indicator honest.

Building the indicator

The operational version is a normalized gold trend used as a dollar-direction input. Compute a volatility-normalized momentum on gold (the CMMA-style primitive from "CMMA: A Better Momentum Primitive Than Price-minus-MA Alone" works), and read its sign and strength as the dollar signal: positive gold momentum implies dollar weakness, scaled by how strong the gold trend is. Apply that dollar read to each USD pair with the correct sign for the dollar's position in the pair.

Three disciplines keep this from becoming noise. Use a real-yield cross-check so the inflation-spike case does not flip the read. Re-estimate the gold-dollar correlation on a rolling window, because in a genuine crisis gold and the dollar can both rally as safe havens and the inverse link breaks, the regime caveat from the triangle article. And treat gold as a confirmer or tilt, not a standalone entry, because it explains the dollar's common factor and not the pair-specific move, the same modest-edge texture every cross-asset signal in this pillar carries. Gold tells you where the dollar is leaning; it does not tell you the entry price.

Visualizing gold as the dollar's mirror

KEY POINTS

- Gold appears on nearly every major currency pair's driver list because it reads the one thing every dollar pair shares: the dollar. Gold trades inverse to the dollar, so a gold move is a dollar move seen from another angle.

- Watching gold lets you read the dollar's common factor across all USD pairs at once, without averaging a basket by hand.

- Gold up means dollar down, applied with the correct sign for the dollar's position in the pair: EURUSD and AUDUSD rise, USDJPY falls. This makes gold a natural confirmer for any dollar trade.

- Gold's second signal is the inflation-and-real-yield backdrop. It tracks real yields, not nominal, so a gold rally on falling real yields is a dovish, dollar-weakening read.

- The inflation-spike trap: nominal yields can rise while real yields fall and gold rallies against a nominal-rate expectation. Use a real-yield or breakeven proxy so the read does not flip in the regime that matters most.

- For the Australian dollar gold is also a direct export, adding a second reinforcing channel, which makes AUDUSD gold-sensitive. The two channels are correlated, not independent, so do not double-count.

- For a pair with no commodity link to gold, only the dollar channel operates and gold is a pure dollar read. Knowing which channels apply to which pair keeps the indicator honest.

- Build it as a volatility-normalized gold momentum read as a dollar-direction input, cross-checked against real yields, with a rolling correlation check (gold and the dollar can both rally in a crisis), used as a confirmer or tilt rather than a standalone entry.

References

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Gold and the Dollar

- The Dollar and Commodities Trend in Opposite Directions

- The Relationship between Commodity Prices and Currency Exchange Rates

- The Global Factor Structure of Exchange Rates

- Currency Factors

- Common Factors in Currency Characteristics

- Oil Fundamentals in the Currency Market (chapter in ‘Intermarket Trading Strategies’)

- Macro and Micro Factors Determining Fluctuations in Gold and Silver Prices

- Can gold hedge and preserve value when the US dollar depreciates?

- Does the value of US dollar matter with the price of oil and gold? A dynamic analysis from time–frequency space

- Nonlinear dynamics of gold and the dollar

- Gold and inflation(s) – A time-varying relationship

- Is gold an inflation-hedge? Evidence from an interrupted Markov-switching cointegration model

- Information transmission between gold and financial assets: Mean, volatility, or risk spillovers?

- Causality and volatility patterns between gold prices and exchange rates

- Is gold a hedge or a safe haven against stock markets? Evidence

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.