4.22 Cross-Asset Confirmation for Trend Systems

Confirmation makes a second related market second a trade before you act. A real trend moves both markets; a false breakout moves one. It cuts whipsaws, at the cost of fewer, later trades.

A moving-average trend system on the S&P fires a long. Left alone, it takes the trade. Add one rule: take the long only if T-bonds are also in an uptrend, confirming the move from the rate side. Over a long sample the unconfirmed system takes 100 trades a year at a 51% hit rate; the confirmed system takes 60 trades a year at a 56% hit rate, and the 40 trades it skipped were the ones where the equity chart was trending up while the bond market was already pricing the move to end. Confirmation did not improve the system's logic. It removed the trades that the rest of the macro picture was voting against.

Confirmation is the close cousin of the intermarket filter, with a different emphasis. A filter gates a whole strategy on or off by an external state, the way "Using Bonds to Filter Equity Signals" switched the equity book by the bond trend. Confirmation operates trade by trade: a signal in the traded market must be seconded by an agreeing signal in a related market before you act. The filter asks "is the regime friendly"; confirmation asks "does a second market agree with this specific trade". They overlap, and the distinction matters because confirmation is where trend systems win back their worst weakness, the whipsaw.

This article takes the confirmation idea from the intermarket templates in "Intermarket Analysis for System Traders" and applies it to the whipsaw problem that defines trend following. It pairs with "Why FX Traders Must Watch Gold, Rates, and Equities", which built the same confirmation count for currencies, and it leads into "Lead-Lag Relationships in Global Markets", which asks which market should be doing the confirming.

Why trend systems need a second opinion

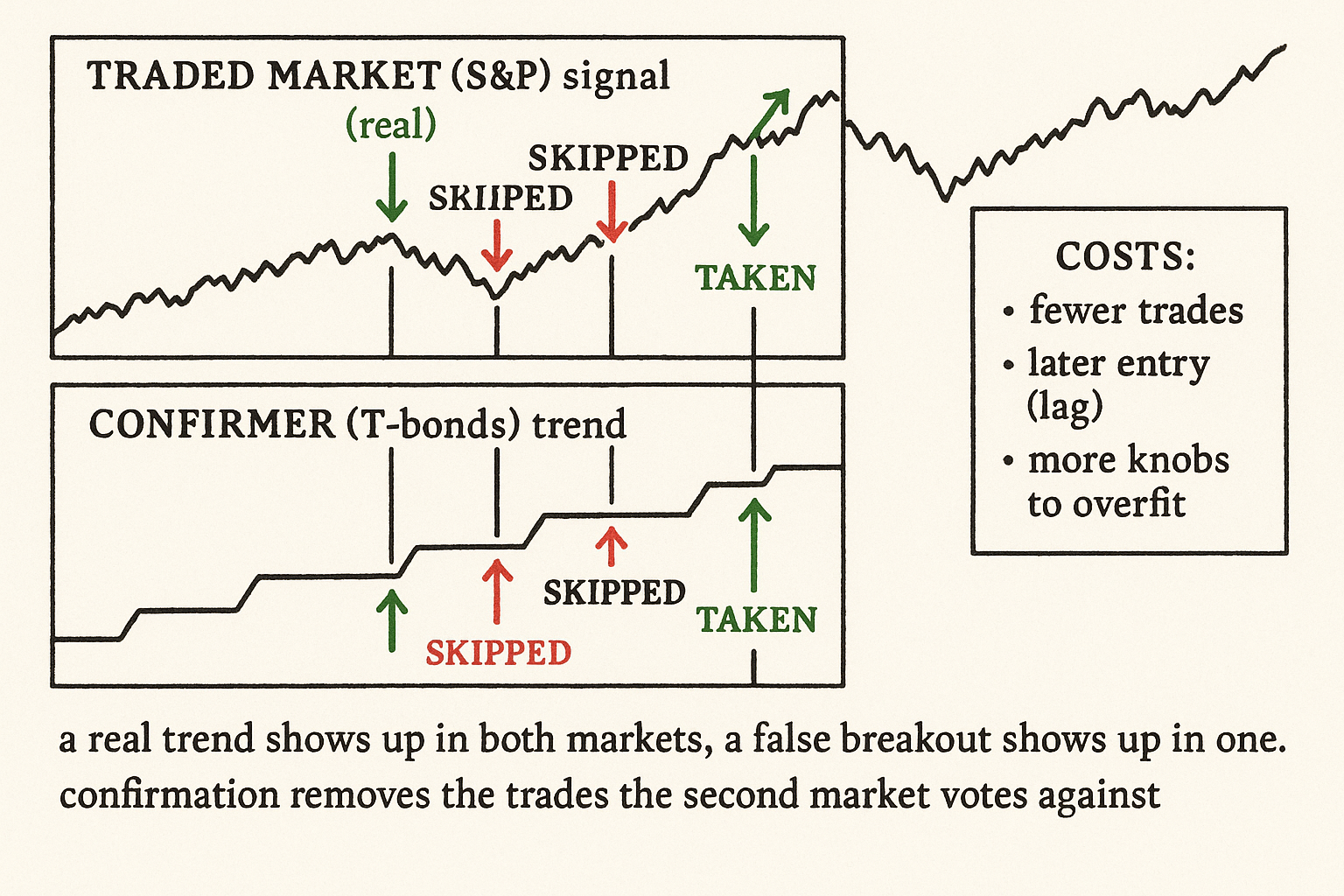

A trend follower's structural cost is the whipsaw: it enters on a breakout, the move fails, it exits at a loss, and it repeats this through every choppy stretch. The article "Why Breakout Systems Need Low Noise Environments" framed the noise side of this. Confirmation attacks it from the cross-asset side. The premise is that a real trend in one market usually shows up as a coordinated move across its related markets, while a false breakout is a local event that the related markets do not echo.

A dollar rally that is real shows up in falling gold and a widening rate differential at the same time. A dollar rally that is noise shows up on the dollar chart alone, with gold and rates indifferent. Requiring the related market to confirm filters the second kind of move, because the noise breakout has no macro second.

$$ \text{Trade}_t = \text{Signal}_{\text{traded},t} \;\wedge\; \big[\,\text{sign}(\text{trend}_{\text{confirm},t}) = \text{expected sign}\,\big] $$

A trade fires only when the traded market's own signal and the confirming market's trend both point the agreed way (the logical AND of the two conditions). For a positively linked confirmer the expected sign matches the traded signal; for a negatively linked one it is flipped. The whole mechanism is this AND: two markets must agree, and the trades that die are the ones where the second market refused to second the first.

The cost of confirmation

Nothing in trading is free, and confirmation has three costs you pay for the cleaner trades.

Fewer trades. Requiring agreement throws out every signal the confirmer disagrees with, and a thinner sample is a less reliable sample. Confirm too hard, with several markets that all must agree, and you arrive at a handful of trades a year and a hit rate you cannot trust, the small-sample fragility the article "Trade-Count Thresholds for Backtest Reliability" warned about.

Lag. The confirming market has to establish its own trend before it can confirm, so the confirmed entry arrives later than the raw signal. For a fast trend system that captures most of its profit in the first days of a move, the lag eats the edge. Confirmation suits slower trend systems where the move lasts long enough that a late entry still pays.

More parameters to overfit. The confirmer adds a market choice and a trend-definition length, and every added knob is another way to fit the backtest. A confirmation rule found by searching which of thirty markets and which moving-average length best improves the equity curve is data-mined, the trap "Why Works on All Markets Is Usually a Red Flag" described. The confirmer must be chosen for an economic reason before the test, not selected for its backtest contribution.

What to confirm with

The confirming market should be the one with the tightest economic link to the traded market, not the one that scores best in-sample. For an equity trend, bonds and the rate complex are the natural confirmers, because they share the discount rate. For a currency trend, the rate differential, gold, and the risk-appetite proxy from "Why FX Traders Must Watch Gold, Rates, and Equities" are the natural confirmers. For a commodity-currency trend, the underlying commodity confirms, the link worked in "Crude Oil, Inflation, and FX".

A second design choice is how many confirmers and how strict. A single confirmer with a simple agree/disagree test is robust and cheap. A confirmation count across two or three related markets, taking the trade when a majority agree, is steadier but spends more degrees of freedom. The conservative default is one well-motivated confirmer, because the marginal confirmer adds correlation, not independence: related markets agree with each other, so the third confirmer rarely says anything the first two did not.

When confirmation backfires

The honest failure modes, because confirmation is not a free upgrade.

The link inverts. Confirmation assumes the sign of the relationship, and when stock-bond or dollar-gold correlation flips regime, the confirmer starts vetoing the right trades and approving the wrong ones. A confirmation rule needs the same rolling correlation check that every relationship in this pillar needs, or it will confidently filter you into the losing half during the regime where the sign is backward.

Both markets are wrong together. In a correlated panic every market moves the same way, so they all confirm each other into the same bad trade. Confirmation protects against idiosyncratic noise in one market; it offers nothing against a systemic move that drags every confirmer along. The diversification of signal source the intermarket overview promised is exactly the thing that fails when correlations spike to 1.

The confirmer leads, so it has already moved. If the confirming market leads the traded market, by the time it confirms it may be near the end of its own move, and you are entering the traded market just as the driver exhausts. This is why confirmation and lead-lag are two sides of one question, and why the next article, "Lead-Lag Relationships in Global Markets", treats the timing of the confirmer as the real problem.

Visualizing confirmation

KEY POINTS

- Confirmation requires a second related market to agree with a trade before you take it. A filter gates a whole strategy by regime; confirmation operates trade by trade.

- The premise: a real trend shows up as a coordinated move across related markets, while a false breakout is a local event the related markets do not echo. Confirmation removes the local noise.

- The mechanism is a logical AND: the traded market's signal and the confirmer's trend must both point the agreed way (matched sign for a positive link, flipped for a negative one).

- Confirmation attacks the trend follower's core weakness, the whipsaw, from the cross-asset side, complementing the noise-based defenses.

- It costs three things: fewer trades (a thinner, less reliable sample), lag (the confirmer must establish its own trend first, hurting fast systems), and more parameters to overfit (a market choice and a length).

- Choose the confirmer for the tightest economic link before testing, not for its backtest contribution. Bonds confirm equities; rates, gold, and risk appetite confirm currencies; the underlying commodity confirms a commodity currency.

- One well-motivated confirmer is the robust default. Extra confirmers add correlation, not independence, because related markets already agree with each other.

- Failure modes: the link inverts across regimes and the confirmer vetoes the right trades; a correlated panic makes every confirmer agree into the same bad trade; and a leading confirmer may have already exhausted its move by the time it confirms.

References

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- What Are Market Regimes? Definitional Chaos, Validation Failure

- Identifying Noise Traders: The Head-And-Shoulders Pattern In U.S.

- How Regional Gold Saving Behavior Shapes House Price

- Algorithmic Trading in Financial and Sports (Exchanges)

- Reframing Financial Markets as Complex Systems

- Fundamental Trading Strategies - Wiley Online Library

- Full article: Revisiting Cont's stylized facts for modern stock markets

- How Regional Gold Saving Behavior Shapes House Price

- Cross-asset signals and time series momentum

- Cross-asset time-series momentum strategy: A new perspective

- Cross-asset time-series momentum: Crude oil volatility and global stock markets

- Cross-asset contagion and risk transmission in global financial markets

- Lead-Lag Relationships in Market Microstructure

- Market microstructure during financial crisis: Dynamics of informed and heuristic-driven trading

- The Science and Practice of Trend-following Systems

- Long-Only Multi-Asset Momentum: Searching for Absolute Returns

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.