4.15 Using Bonds to Filter Equity Signals

Stocks and bonds are two prices set by one rate. Gate long equity signals on the bond trend to strip out drawdown-heavy days, but check the rolling correlation first, since the sign inverts.

The single most studied intermarket link is the one between long bonds and stocks, and it produces a filter you can write in one line: take long equity signals only when T-bonds are above their moving average. The mechanism is the discount rate. Both stocks and bonds are valued by discounting future cash flows at the long interest rate, so when the bond market rallies (yields falling), the discount rate on equities drops too, and the present value of every future earnings stream rises. When bonds sell off (yields rising), the same discounting works against stocks. Bonds and stocks are two prices set by one rate, which is why the bond trend is a usable gate on the equity trend.

This article takes the bond-equity pair, the most reliable link in the intermarket web from "Intermarket Analysis for System Traders", and builds the filter step by step with the distribution split from "Why Cross-Asset Signals Beat Isolated Chart Reading". It also flags the regime where the whole thing inverts, because the stock-bond correlation is the textbook case of a relationship that changes sign across decades.

The filter, stated precisely

The rule has three parts: the external market, the state test, and the action.

External market: the long-bond future (or a bond price proxy). State test: is the bond close above its moving average of length n. Action: when the bond is above its average, allow the equity system's long signals; when the bond is below its average, suppress them (sit in cash) or reduce size.

$$ \text{Position}_{\text{equity}} = \begin{cases} \text{equity signal} & \text{if } B_t > \text{MA}_n(B)\\[4pt] 0 & \text{if } B_t \le \text{MA}_n(B) \end{cases} $$

The equity position equals whatever the underlying equity system says, but only when the bond price B at time t sits above its n-period moving average. Below the average, the position is flattened. The moving-average length n is the one free parameter, and it should be chosen for stability, not for the value that maximizes backtest profit, the trap the article "Trading Systems Are Recipes, Not Predictions" called curve-fit stops. A length anywhere from 30 to 80 days that gives similar results is a sign the filter is robust; a length where 50 wins and 45 and 55 both fail is a sign you have fit noise.

Subdividing the days

The clean way to see the filter work is to subdivide the equity sample by the bond state and compare the two sub-distributions to the whole, exactly the procedure that justifies any intermarket gate.

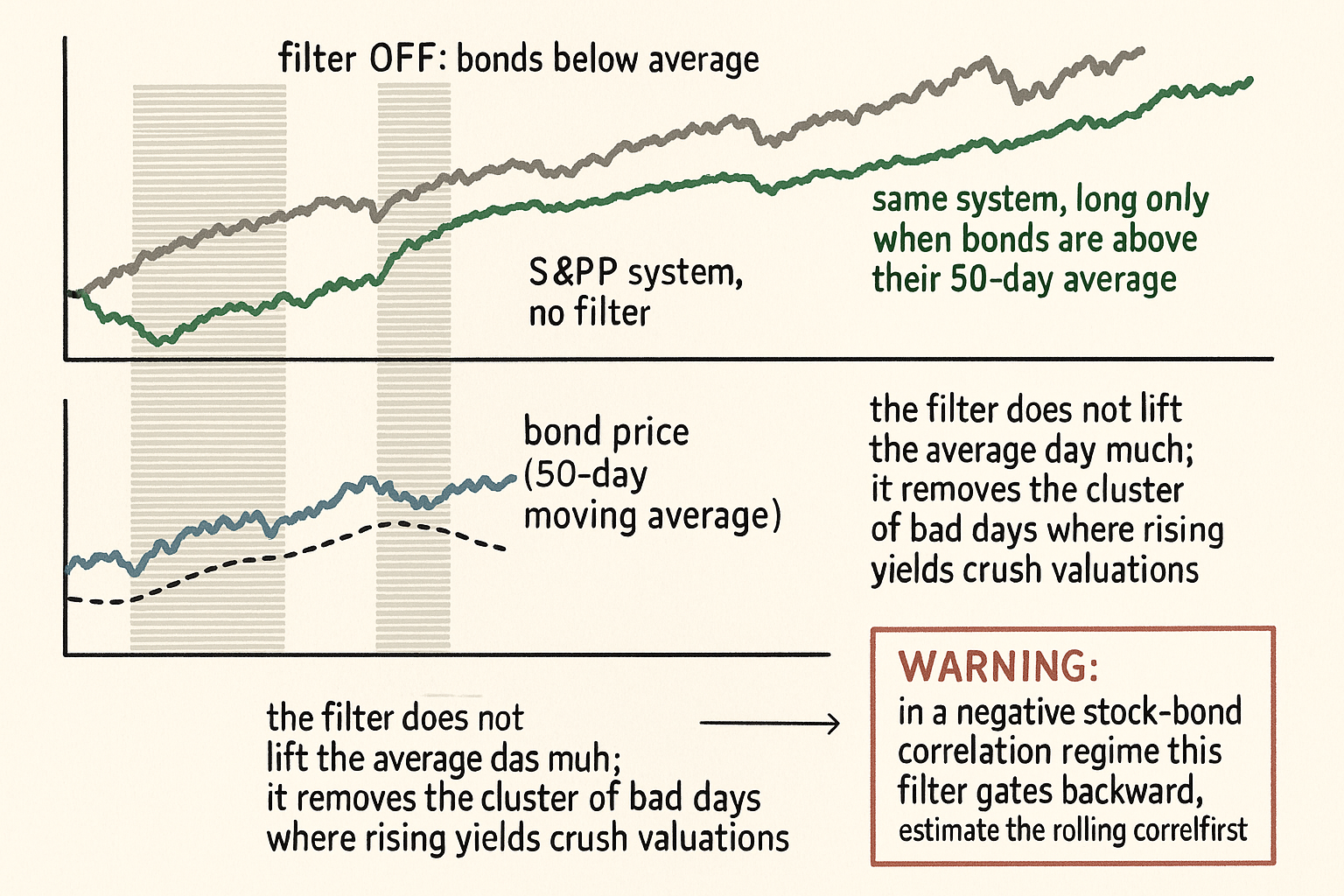

Take the full set of equity trading days and their forward returns. Split into "bond up" days (bond above its average) and "bond down" days. Across long historical samples, the bond-up subset carries a materially higher mean forward return and a lower standard deviation than the full set, while the bond-down subset carries a near-zero or negative mean and a higher standard deviation. The two halves are different markets wearing the same ticker.

A representative split on a few thousand equity days: the full sample annualizes to roughly 7% with a given drawdown profile; the bond-up subset annualizes closer to 11% with shallower drawdowns; the bond-down subset annualizes near 1% to 2% with deeper, faster drawdowns. The bond-down days are where most of the equity market's pain concentrates, because rising yields compress valuations and rising yields are exactly what "bond below its average" detects.

The practical read: the filter does not improve the average day by a lot. It removes a slice of bad days that are disproportionately responsible for drawdowns, which improves the risk-adjusted return more than the raw return. That is the right way to judge it, the lesson from "Why Profit Factor Can Lie" about looking at the shape of the distribution rather than one summary number.

What the filter costs you

No filter is free, and this one has two clear costs.

It sits out good days. Equities sometimes rally hard while bonds are below their average (a "good growth, rising rates" regime), and the filter has you in cash for those. You give up real upside to avoid the bad days. Whether that trade is worth it depends on whether your objective is return or risk-adjusted return, and for most leveraged or drawdown-sensitive books it is the latter.

It adds turnover. The bond crossing its average flips the filter on and off, generating entries and exits that the unfiltered equity system would not make. Each flip is a round-trip cost. If the bond oscillates around its average for a stretch, the filter whipsaws, and the article "Why Transaction Costs Should Be Added Before You Fall in Love" applies directly: a filter that improves gross returns can destroy net returns through whipsaw if the cross-asset series is choppy near the threshold. Smoothing the bond series or adding a band around the average reduces this, at the cost of slower reaction.

The regime that inverts the sign

The dangerous part, and the reason a hard-coded bond-equity filter is not safe to set and forget.

The stock-bond correlation is not stable across decades. Through long inflationary stretches, stocks and bonds have moved together (both hurt by rising yields), and the filter as written works. Through other stretches, the correlation goes negative: bonds rally as a safe haven precisely when stocks crash, so "bonds above their average" coincides with equity stress rather than equity strength, and the filter's sign is backward. A filter built on the positive-correlation assumption and run through a negative-correlation regime will gate exactly wrong.

The defense is to make the filter conditional on the measured correlation, not to assume it. Estimate the rolling correlation between stock and bond returns over a trailing window. When it is reliably positive, apply the filter as written. When it is negative or unstable, disable the filter or flip its sign. This turns a brittle hard-coded rule into a regime-aware one, the slow-drift discipline the article "Slow Wandering: The Most Dangerous Type of Market Change" argued every structural relationship needs. A trader who skips this step is not running an intermarket system; he is betting that one historical correlation regime lasts forever.

Visualizing the filtered equity curve

KEY POINTS

- Stocks and long bonds are two prices set by one rate. Falling yields (bonds rallying) lift equity valuations through a lower discount rate; rising yields compress them. That shared mechanism makes the bond trend a usable gate on the equity trend.

- The filter in one line: take long equity signals only when bonds are above their moving average; flatten or reduce size when bonds are below. The moving-average length is the only free parameter and should be chosen for stability, not maximum backtest profit.

- Subdividing equity days by bond state splits one market into two. The bond-up subset shows higher mean forward return and lower dispersion; the bond-down subset concentrates the drawdowns, because rising yields and falling equity valuations are the same event.

- The filter's main value is risk-adjusted, not raw. It removes a slice of disproportionately bad days, improving drawdown more than average return. Judge it by the shape of the distribution, not one summary number.

- It costs you the good days that occur while bonds are below their average (strong growth, rising rates), and it adds turnover. A bond series chopping around its average whipsaws the filter and can destroy net returns through round-trip costs.

- The correlation inverts across regimes. In long inflationary stretches stocks and bonds fall together and the filter works; in safe-haven regimes bonds rally as stocks crash and the filter gates backward.

- The fix is to condition the filter on the rolling stock-bond correlation: apply it when the correlation is reliably positive, disable or flip it when negative or unstable. A hard-coded filter bets one correlation regime lasts forever.

- Smooth the bond series or add a band around the average to cut whipsaw, accepting slower reaction in exchange for fewer false flips.

References

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Factor Investing and the Integration of Corporate Bond and Equity Markets

- Lead-Lag Relationships in Market Microstructure⋆

- NBER WORKING PAPER SERIES NOISE TRADING AND

- A Simple Model of Intertemporal Capital Asset Pricing and Its

- Overreaction as an indicator for momentum in algorithmic trading

- High-Frequency Trading, Asset Pricing, and Market Microstructure

- The Microstructure of Foreign Exchange Markets | NBER

- The Effects of Mandatory Transparency in Financial Market Design

- Macroeconomic Drivers of Stocks and Bonds

- US Stock–Bond Correlation: What Are the Macroeconomic Drivers?

- Empirical Evidence on the Stock–Bond Correlation

- Interest Rate Changes and the Cross-Section of Global Equity Returns

- Cross-Asset Signals and Time Series Momentum

- Carry and Trend Following Returns in the Foreign Exchange Market

- A Theory of Technical Trading Using Moving Averages

- It Takes Two to Tango: Fundamental Timing in Stock Market

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.