4.18 Crude Oil, Inflation, and FX

Crude is the price of energy and a leading inflation gauge. It runs inverse to bonds and the dollar and feeds FX through trade and rates. A supply shock fakes the read, so cross-check copper.

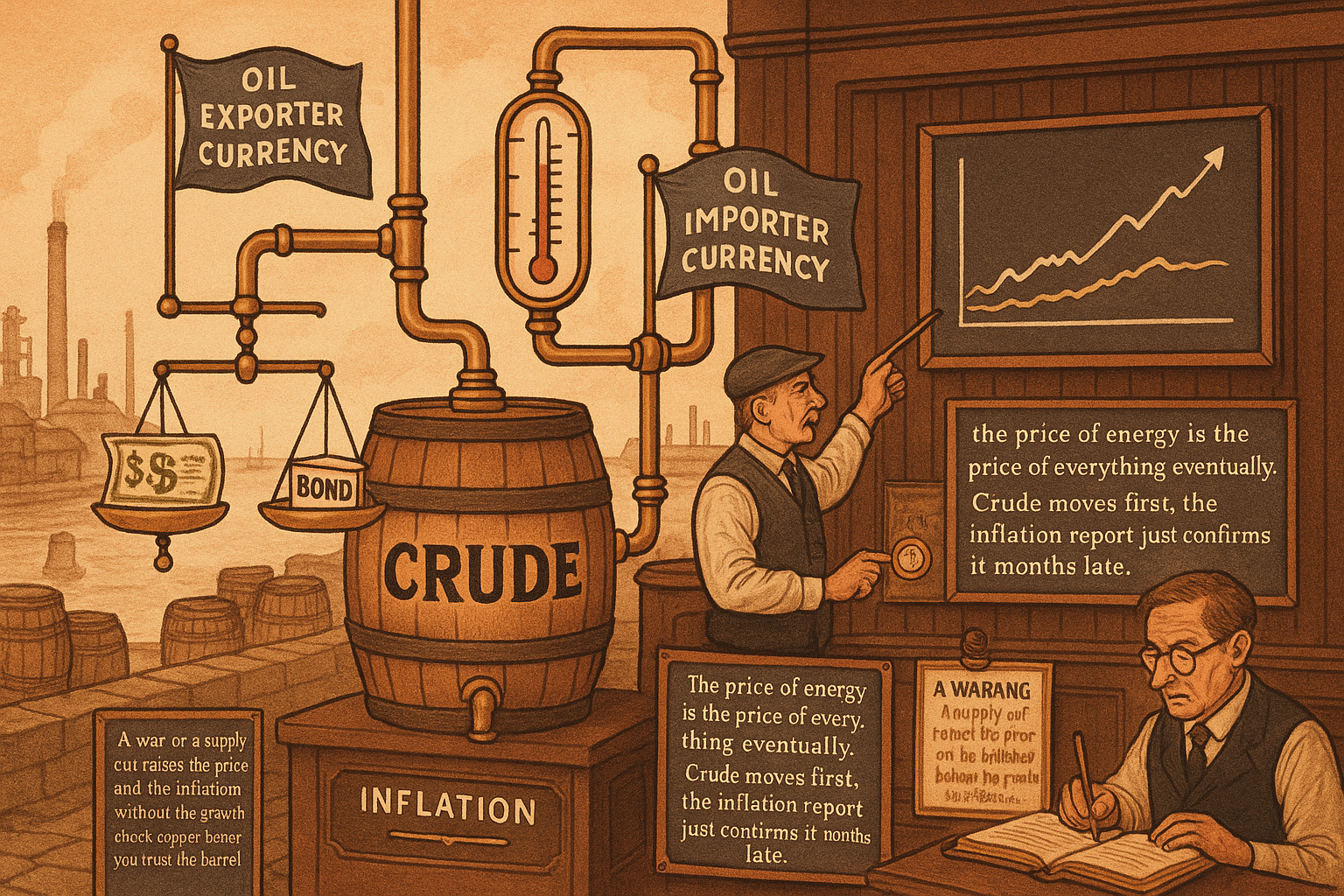

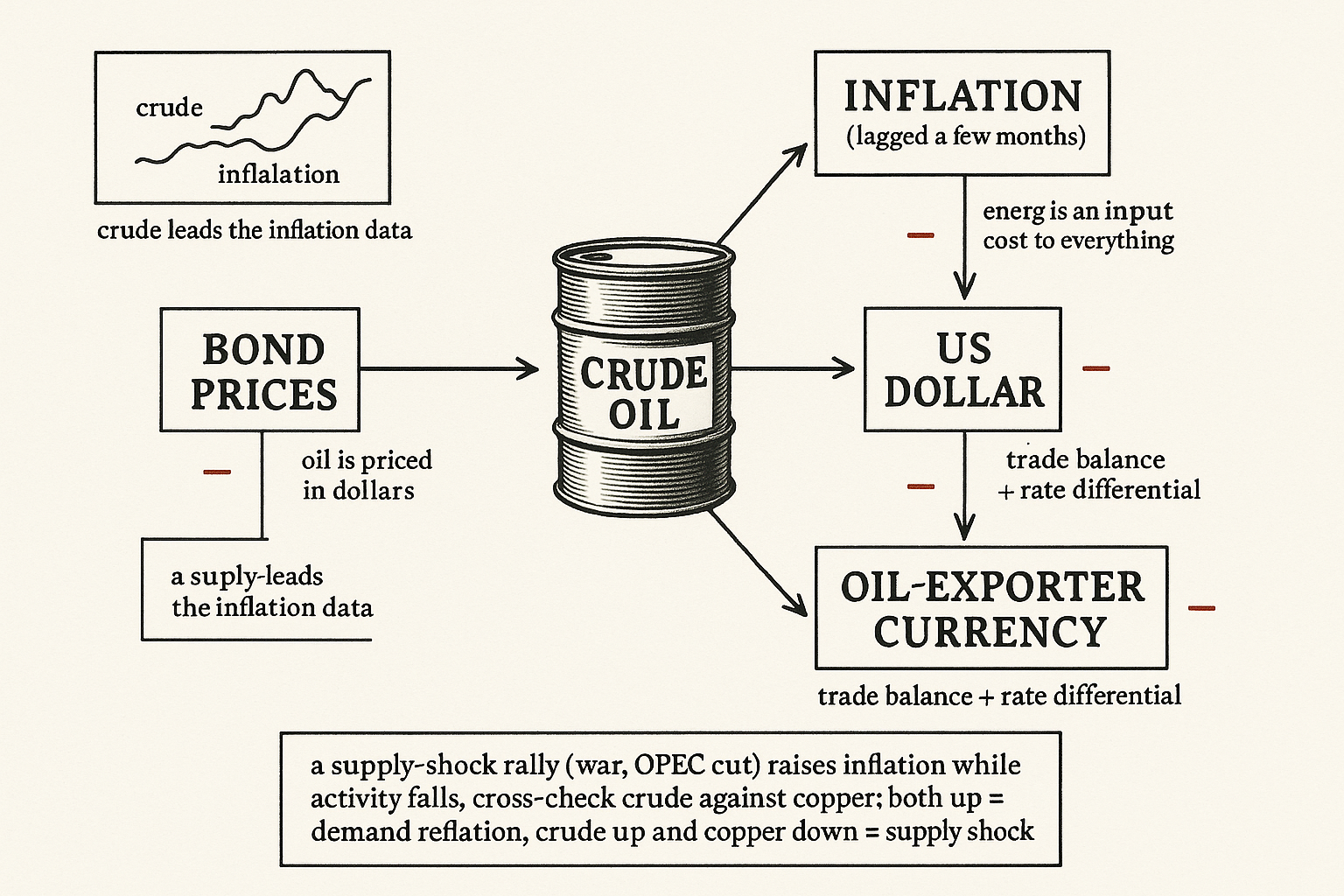

Crude oil is the price of energy, and energy is an input cost to almost everything that gets produced, shipped, or heated. When crude rises, transport costs, manufacturing costs, and headline inflation rise behind it within a few months. That makes crude a leading inflation gauge, which links it to two markets at once: bonds, because inflation erodes a fixed coupon, and the dollar, because the dollar is the currency oil is priced and settled in. Crude runs inverse to both bond prices and the dollar over most samples, and those two inverse links are the spine of every oil-based intermarket system.

This article handles the inflation side of the commodity complex, the complement to "Copper as an Economic Activity Indicator", which handled the growth side. Together they split commodities into a growth signal (copper) and an inflation signal (crude), and this article also extends the map into currencies, feeding the FX articles later in the pillar including "Why FX Traders Must Watch Gold, Rates, and Equities".

Crude as a leading inflation gauge

The transmission from crude to inflation is mechanical and lagged. A jump in crude raises the cost of fuel, freight, plastics, fertilizer, and heating, and those costs pass through to consumer prices over the following months. The official inflation print is therefore a delayed echo of where crude went earlier, which means crude leads the inflation data that bond markets and central banks react to.

That lead is the whole reason crude is useful in a system. By the time the inflation print confirms a rise, bonds have often already moved. Crude gives a forward read on the inflation impulse, the same forward-looking property that made copper valuable, but pointed at inflation rather than activity. A trader who waits for the inflation release is reacting to old news; a trader watching crude is reading the input that release will eventually report.

The two inverse links

Crude against bonds. Rising crude feeds inflation, inflation erodes the real value of a fixed coupon, so bond yields rise and bond prices fall to compensate. Crude up, inflation up, yields up, bonds down. The chain is the inflation-side mirror of copper's activity chain, and both end at the same place (yields up, bonds down) through different mechanisms.

Crude against the dollar. Oil is priced and settled in dollars worldwide. A stronger dollar means each dollar buys more oil, pushing the dollar price of crude down; a weaker dollar pushes it up. The two trade inverse. The relationship also runs the other way through trade balances and petrodollar flows, but the priced-in-dollars channel is the dominant, most reliable one.

$$ \text{Crude} \;\uparrow \;\Rightarrow\; \text{inflation} \;\uparrow \;\Rightarrow\; \text{bond price} \;\downarrow, \qquad \text{Dollar} \;\uparrow \;\Rightarrow\; \text{Crude (in USD)} \;\downarrow $$

The first chain reads crude up, inflation up, bond price down; the second reads dollar up, crude down. The oil-stock index (a basket of oil producer equities) tends to turn with or slightly ahead of crude itself, so it serves as a confirming or leading read on the crude move, the lead-lag idea applied within the energy complex.

Crude as an FX signal

The inflation and dollar links make crude a usable input for currency systems, especially for commodity-exporting and commodity-importing currencies.

Commodity-exporter currencies. The currencies of major oil exporters tend to strengthen when crude rises, because higher oil revenue improves the country's trade balance and pulls capital in. Rising crude is a tailwind for an exporter currency and a headwind for a heavy importer currency that has to pay more for the same barrels. A crude trend can gate long signals on an exporter currency and short signals on an importer currency, template 1 and template 2 applied to FX.

Inflation-and-rates channel. Rising crude raises inflation, which can force a central bank to tighten, which lifts that country's currency through the rate differential, the carry mechanism from "Gold, Dollar, and Rates: A Practical Intermarket Map". Crude therefore feeds the FX picture twice: directly through the trade balance and indirectly through the inflation-to-rates-to-currency chain. The two channels usually reinforce for exporters and can conflict for importers, which is exactly the kind of cross-current the divergence test in "Intermarket Divergence as a Trading Filter" is built to flag.

A worked sketch: gating a long-trade system on an oil-exporter currency to fire only when crude is above its moving average aligns the currency position with its dominant fundamental driver, raising the per-trade quality the same way the bond filter did for equities. The exporter currency fights an uphill battle when crude is falling, and the filter keeps you out of that fight.

The traps with crude

Where crude misleads.

Supply shocks dominate the inflation read. Crude spikes driven by war, OPEC supply cuts, or pipeline disruptions raise the price without any underlying demand strength, and they raise inflation while activity is weakening, the "stagflation" combination. A crude-as-inflation filter behaves differently in a demand-driven oil rally than in a supply-shock rally, and treating the two as identical is a mistake. Cross-checking crude against copper helps: copper and crude rising together points to demand-driven reflation, while crude rising as copper falls points to a supply shock, the cross-asset confirmation logic again.

The dollar link weakens for big oil moves. When crude moves on a large supply shock, it can swamp the dollar relationship entirely, moving far more than the dollar can explain. The inverse link is a normal-regime tendency, not a tight arbitrage.

The FX links are country-specific and drift. Which currencies are "oil currencies" depends on each country's export mix, and that mix changes over years as economies diversify or as production shifts. An FX-crude relationship estimated a decade ago may not hold today, the slow-drift problem that applies to every edge in the web. Re-estimate the currency's sensitivity to crude on a rolling window rather than treating it as a fixed label.

Visualizing the crude links

KEY POINTS

- Crude oil is an input cost to almost everything produced, shipped, or heated, so a rise in crude feeds headline inflation within a few months. Crude is a leading inflation gauge.

- The lead matters: the official inflation print is a delayed echo of where crude already went, so watching crude reads the inflation impulse before the data confirms it and before bonds finish reacting.

- Two inverse links form the spine. Crude up feeds inflation, lifts yields, and lowers bond prices; a stronger dollar lowers the dollar price of crude because oil is priced in dollars. The oil-stock index turns with or slightly ahead of crude.

- Crude's activity-side mirror is copper. Both chains end at yields up and bonds down, but copper runs through real activity and crude runs through inflation.

- Crude is an FX signal through two channels: directly via the trade balance (rising crude helps exporter currencies, hurts importer currencies) and indirectly via inflation forcing rate hikes that lift a currency through carry. The channels reinforce for exporters and can conflict for importers.

- Gating a long-trade system on an exporter currency to fire only when crude is above its average aligns the position with its dominant driver and keeps you out of the uphill fight when crude is falling.

- Trap one: supply-shock rallies (war, OPEC cuts) raise inflation while activity weakens (stagflation), behaving differently from demand-driven rallies. Cross-check against copper to tell them apart.

- Trap two: large oil moves swamp the dollar link, and the FX relationships are country-specific and drift as export mixes change. Re-estimate a currency's crude sensitivity on a rolling window rather than treating it as a fixed label.

References

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Crude Oil Price Changes and Inflation

- Oil Price Shocks and US Business Cycles

- Evaluating the Predictive Content of Divisia M4 for US Crude-Oil Prices: A Bayesian Time-Varying Parameter VAR Analysis

- The Price of Crude Oil as a Factor for USD Volatility

- Extreme Comovements and Downside/Upside Risk Spillovers Between Oil Prices and Exchange Rates

- Lead–Lag Relationships in Market Microstructure

- Market Microstructure Noise and Realized Volatility

- The FX Race to Zero: Electronification and Market Structural Issues in Foreign Exchange Markets

- Study of the Impact of Crude Oil Prices on Economic Output and Inflation in Saudi Arabia

- The Impact of Oil Price Changes on Inflation and Disaggregated Consumer Prices

- Oil Price Dynamics and Market-Based Inflation Expectations

- Movements in International Bond Markets: The Role of Oil Prices

- Monetary Policy Drivers of Bond and Equity Risks

- US Dollar and Oil Market Uncertainty

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.