4.20 Intermarket Divergence as a Trading Filter

When two correlated markets agree they tell you nothing; the signal is the disagreement. Divergence flags when leader and lagger split, but you must know which leads, and the lead shifts.

Two markets are supposed to move together. Bonds and stocks share a discount rate; gold and the dollar trade inverse; copper and yields rise together. Most of the time they honor those relationships, and the relationship is uninformative because everyone already prices it in. The signal lives in the moments they disagree. Bonds rallying hard while stocks keep falling, when the two normally move together, is an intermarket divergence: the traded market is doing the opposite of what its partner says it should. That disagreement is information, because one of the two markets is usually right, and the divergence flags which trades to trust and which to fade.

This article defines intermarket divergence precisely, gives the two standard ways to measure it, and turns it into a filter using the divergence template from "Intermarket Analysis for System Traders". It is the most subtle of the four templates because it fires on disagreement rather than state, and it closes the intermarket arc that "Using Ratios as Trading Signals" and the gold-dollar-rates map opened.

Defining divergence operationally

Divergence is the traded market moving against what its intermarket partner predicts, given their normal correlation. The definition has two parts: the expected relationship, and the observed violation of it.

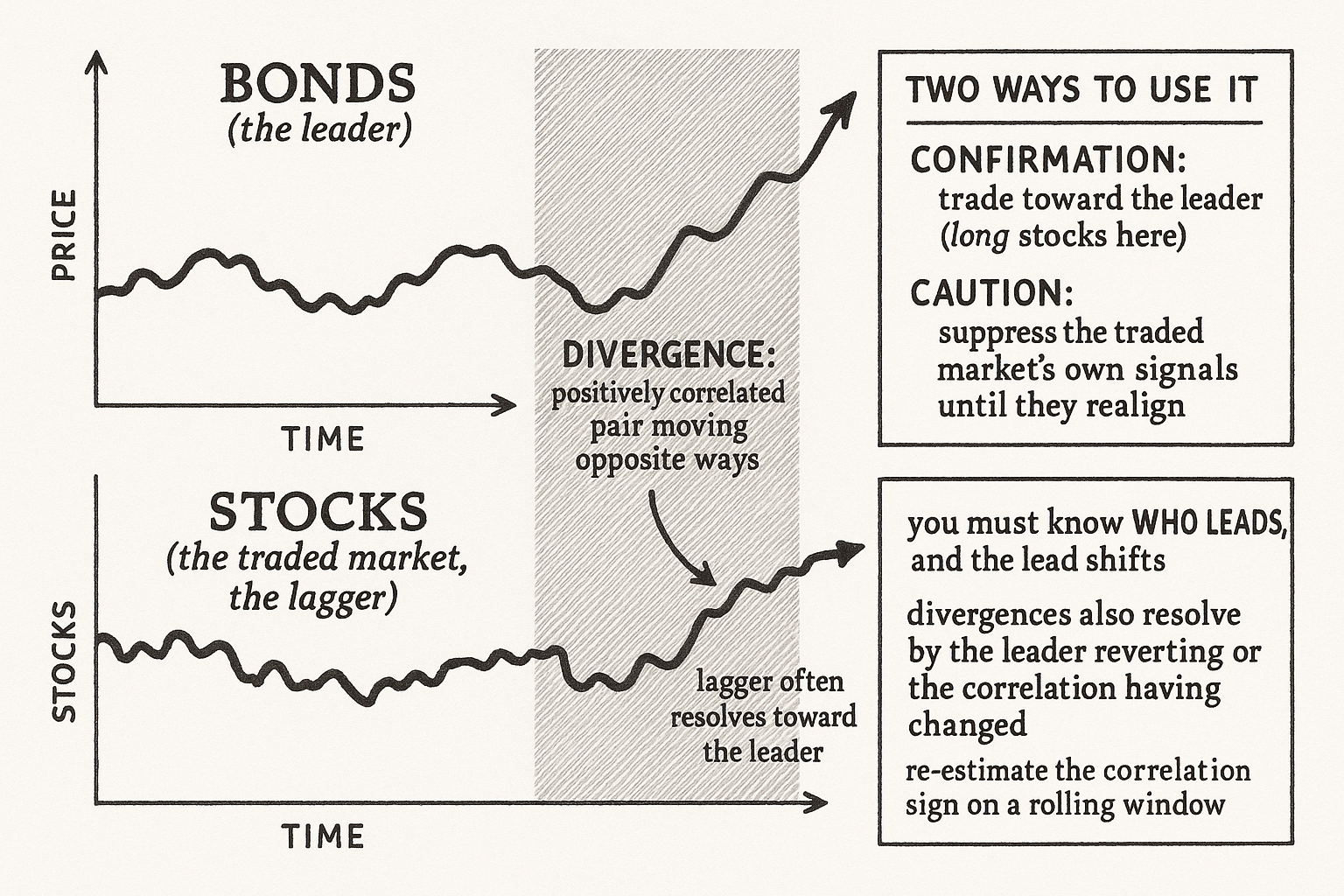

For a positively correlated pair (stocks and bonds), divergence is the two moving in opposite directions: bonds up, stocks down, or bonds down, stocks up. For a negatively correlated pair (gold and the dollar), divergence is the two moving in the same direction: both rising or both falling, when they normally trade inverse. The sign of the expected correlation flips what counts as a divergence, which is why you must know the pair's normal sign before you can detect a violation of it.

The trading interpretation rests on a lead-lag assumption: when the leading market and the lagging market disagree, the leading market tends to win, and the lagging market resolves toward it. Bonds leading stocks means a bond-stock divergence often resolves with stocks following bonds, so the divergence is a signal to position in the direction of the leader, the lead-lag idea the article "Lead-Lag Relationships in Global Markets" treats as a measurement problem rather than an assumption to take on faith.

Two ways to measure it

The two standard measures differ in what they compare, and they often agree, which lets them cross-check each other.

Measure one, momentum divergence. Compute a momentum (rate of change over n bars) for both the traded market and its partner. Divergence is when the two momentums have signs that violate the expected correlation: opposite signs for a positive pair, same signs for a negative pair. This is fast and sensitive, and noisy, because short-window momentum flips easily.

Measure two, moving-average divergence. Compare each market's price to its own moving average. Divergence is when the traded market is below its average while the partner (positive pair) is above its average, or the equivalent sign-flipped condition for a negative pair. This is slower and steadier than momentum divergence, because a price crossing its moving average is a higher bar than a momentum sign flip.

$$ \text{Divergence (positive pair)} = \big[\,\text{sign}(\Delta A) \neq \text{sign}(\Delta B)\,\big], \qquad \Delta X = X_t - X_{t-n} \;\;\text{or}\;\; X_t - \text{MA}_n(X) $$

A divergence on a positively correlated pair fires when the change in market A and the change in market B have opposite signs, where the change is either an n-bar momentum or the gap between price and its moving average. For a negatively correlated pair you flip the condition to fire when the signs match. Using both the momentum and the moving-average versions and requiring them to agree filters out the weakest divergences, the cross-check discipline that runs through this pillar.

The filter

Divergence is used two ways, and they point in opposite directions, so you must decide which you believe for a given pair.

Confirmation use (trade with the leader). When the leading market diverges from the lagging traded market, position the traded market in the direction the leader implies, expecting the lagger to catch up. Bonds rallying while stocks fall, read through a positive correlation, says stocks should turn up to follow bonds, so a divergence becomes a long-stock signal. This treats divergence as an early warning that the traded market is about to reverse toward its partner.

Caution use (suppress signals during divergence). Treat any divergence as a regime where the normal relationship is broken and the traded market's own signals are less reliable, so reduce size or stand aside until the markets realign. This is the conservative reading: divergence means "the macro plumbing and the chart disagree, do not trust the chart until they reconcile."

The two uses are not contradictory once you tie them to the lead-lag structure. If you have evidence the partner leads, use confirmation and trade toward the leader. If you do not know which leads, use caution and stand aside. A worked sketch on an equity trend system: suppressing long-equity entries while bonds are diverging bearishly (bonds falling, signaling rising yields, while the equity chart still says buy) removes a cluster of trades taken into a hostile macro backdrop, the same drawdown-trimming effect the bond filter produced in "Using Bonds to Filter Equity Signals", but triggered by disagreement rather than state.

The traps with divergence

Divergence is the trickiest template, and it fails in specific ways.

You need to know who leads, and the lead is unstable. The confirmation use depends on the partner leading the traded market, and leadership shifts over time and even reverses. Betting that bonds lead stocks when in the current regime stocks are leading bonds means you fade the right market. Without a measured, current lead-lag estimate, the confirmation use is a guess, and the article "Induction in Trading: Why Past Patterns Are Always Uncertain" applies directly to the lead assumption.

Divergences resolve both ways. A divergence can resolve by the lagger catching up to the leader (the assumption), or by the leader reverting to the lagger, or by the correlation simply having changed so the "divergence" is the new normal. Only the first resolution pays the confirmation trade. The honest expectation is a modest edge from the cases that resolve as assumed, diluted by the cases that do not, not a clean reversal signal.

It is noisy and easy to over-detect. Short-window momentum divergences fire constantly, most of them meaningless. Requiring agreement between the momentum and moving-average measures, and restricting to economically linked pairs, cuts the false positives, but a divergence filter that fires too often is mostly trading noise, the over-detection problem the article "Why Works on All Markets Is Usually a Red Flag" warned about generalized to disagreement signals.

The correlation sign can have flipped. A "divergence" detected against an assumed positive correlation is meaningless if the pair has quietly gone negatively correlated. The divergence detector must use the current measured correlation sign, re-estimated on a rolling window, or it will label normal behavior as a divergence and vice versa.

Visualizing a divergence

KEY POINTS

- Markets that normally move together are uninformative when they honor the relationship, because it is already priced. The signal lives in the moments they disagree, which is an intermarket divergence.

- Divergence is the traded market moving against what its partner predicts given their normal correlation: opposite directions for a positively correlated pair, the same direction for a negatively correlated pair. You must know the pair's normal sign before you can detect a violation.

- The trading interpretation rests on lead-lag: when the leader and the lagger disagree, the leader tends to win and the lagger resolves toward it.

- Two measures: momentum divergence (the two markets' rate-of-change signs violate the expected correlation, fast and noisy) and moving-average divergence (each price versus its own average, slower and steadier). Requiring both to agree filters the weakest signals.

- Confirmation use: trade the traded market toward the direction the leader implies, expecting the lagger to catch up. Caution use: treat divergence as a broken-relationship regime and suppress the traded market's own signals until realignment.

- The two uses tie to lead-lag: trade toward the leader if you have evidence the partner leads, stand aside if you do not know which leads.

- Worked effect: suppressing long-equity entries while bonds diverge bearishly removes trades taken into a hostile macro backdrop, trimming drawdowns the way the bond filter did, but triggered by disagreement rather than state.

- The traps: leadership is unstable and must be measured currently; divergences resolve both ways so the edge is modest and diluted; the signal is noisy and easy to over-detect; and the correlation sign can have flipped, so re-estimate it on a rolling window before labeling anything a divergence.

References

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Intermarket Analysis: The Study of Relationships

- Lead-Lag Relationships in Market Microstructure

- Market Microstructure Noise and Efficient Price Discovery

- Market Macrostructure: Institutions and Asset Prices

- Anatomy of Alpha Illusion in Daily FX Markets

- Do Momentum-Based Strategies Still Work in Foreign Currency Markets?

- Short-Term Trading Strategy on G10 Currencies

- Market Microstructure Across Centralised and Decentralised Trading Venues

- Lead–lag relationships in foreign exchange markets

- An investigation of the lead–lag relationship in returns and volatility between the stock index futures and cash index in the Greek stock market

- The time difference effect of a measurement unit in the lead–lag relationship analysis of Korean financial market

- Global Realignment in Financial Market Dynamics

- The linear and nonlinear lead–lag relationship among three SSE 50 Index markets: The index futures, 50ETF spot and options markets

- A stock market trading system based on foreign and domestic information

- Gold's market volatility and the fading safe haven effect

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.