4.33 Cross-Pair Signals: Can EUR Predict GBP?

EURUSD and GBPUSD move together because they share the dollar, not because EUR predicts GBP. Subtract the pairs (CMMA of one minus the other) to cancel the dollar and trade EUR-versus-GBP strength.

EURUSD and GBPUSD move together. Watch them on the same screen and they look like two copies of one chart, rising and falling almost in lockstep. The obvious trade idea: EUR leads, so a move in EURUSD predicts the next move in GBPUSD, trade GBP off EUR. The idea is mostly wrong, and the reason it is wrong is the most important thing to understand about cross-pair signals. EURUSD and GBPUSD share the dollar. Both are "something divided by USD", so when the dollar moves, both pairs move the same way, and the correlation you see is the shared dollar, not EUR telling you anything about GBP.

This is the third-variable confound in its purest form. Two series correlate because a common factor drives both, not because one causes the other, the ice-cream-and-drowning trap from "Lead-Lag Relationships in Global Markets". To get a real cross-pair signal you have to remove the shared dollar and ask whether what is left in EUR predicts what is left in GBP. Done right, that subtraction is one line, and it turns "can EUR predict GBP" into a clean, tradeable question about EUR-versus-GBP relative strength.

This article builds the cross-pair signal correctly, using the CMMA momentum primitive from "CMMA: A Better Momentum Primitive Than Price-minus-MA Alone" to cancel the dollar. It follows the co-movement facts from "Why FX Traders Must Watch Gold, Rates, and Equities" and sets up the full decomposition in "Currency Strength Models from Pair Decomposition".

Why the pairs move together

Write each pair as what it is: a ratio of two currencies. EURUSD is EUR over USD; GBPUSD is GBP over USD. In log returns that becomes a difference: the return of EURUSD is the strength change of EUR minus the strength change of USD, and the return of GBPUSD is the strength change of GBP minus the strength change of USD.

$$ r_{\text{EURUSD}} = \Delta\text{EUR} - \Delta\text{USD}, \qquad r_{\text{GBPUSD}} = \Delta\text{GBP} - \Delta\text{USD} $$

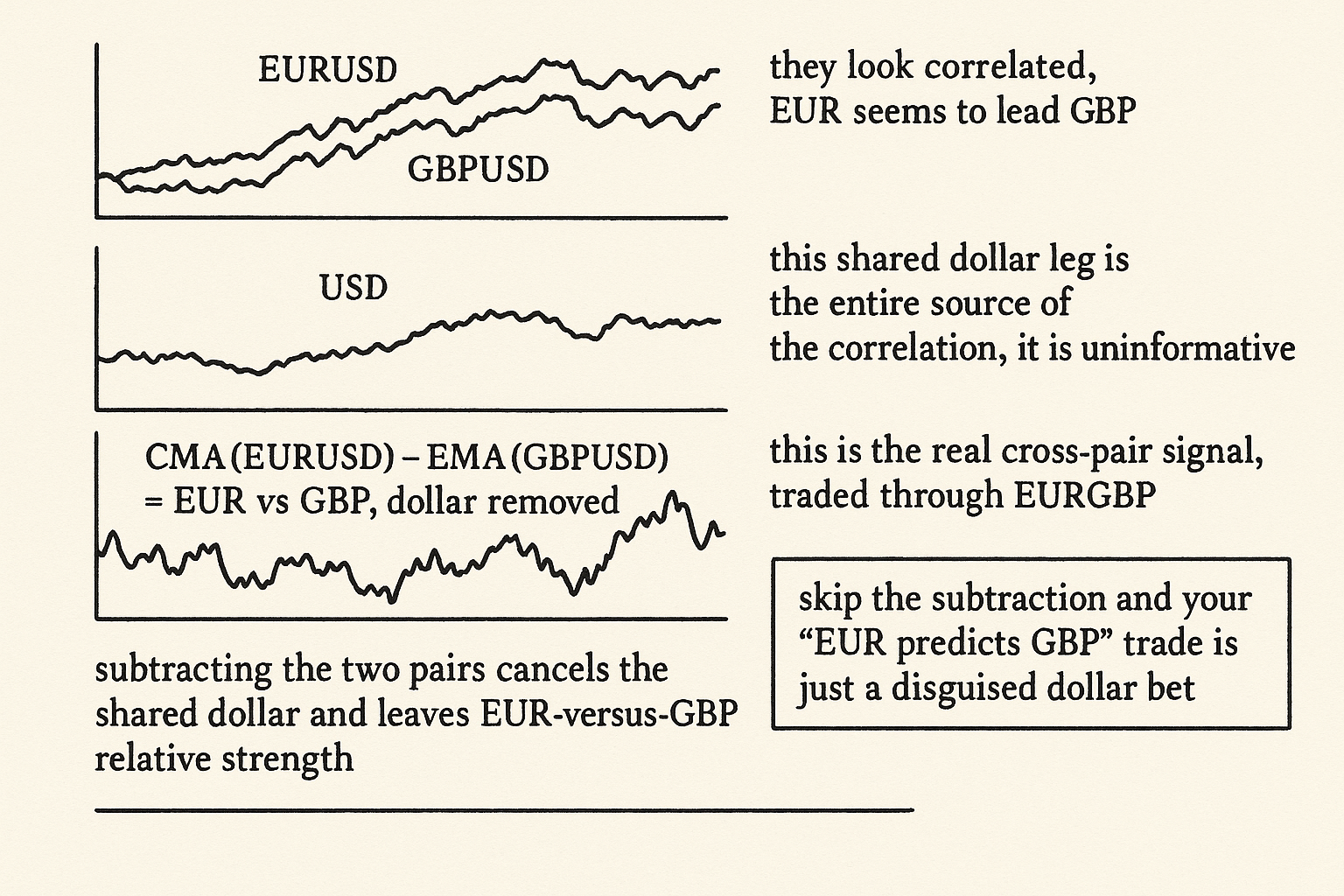

The EURUSD return is the change in EUR strength minus the change in USD strength; the GBPUSD return is the change in GBP strength minus the change in USD strength. Both contain the same minus-USD term. When the dollar moves, that shared term moves both pairs together, which is the entire source of their correlation. A dollar rally drags EURUSD and GBPUSD down together while telling you nothing about whether EUR is stronger or weaker than GBP. The co-movement is real and it is uninformative, because it is the dollar talking, not EUR.

Subtracting the dollar

The fix falls straight out of the algebra. Subtract the two pair returns and the shared minus-USD term cancels, leaving the EUR-versus-GBP relative move with no dollar in it.

$$ r_{\text{EURUSD}} - r_{\text{GBPUSD}} = \big(\Delta\text{EUR} - \Delta\text{USD}\big) - \big(\Delta\text{GBP} - \Delta\text{USD}\big) = \Delta\text{EUR} - \Delta\text{GBP} $$

Subtracting the GBPUSD return from the EURUSD return cancels the USD term exactly, leaving the change in EUR strength minus the change in GBP strength. That difference is the EUR-versus-GBP signal, and it is precisely what EURGBP measures, because EURGBP is EUR over GBP with no dollar in it at all. The whole "can EUR predict GBP" question reduces to: is there a tradeable relative-strength relationship between EUR and GBP, which you read off EURGBP or off the difference of the two USD pairs.

The practical version uses a normalized momentum so the two legs are comparable. Compute CMMA (close minus moving average, divided by ATR times the square root of the lookback) on each pair, then take the difference: CMMA of EURUSD minus CMMA of GBPUSD. CMMA is volatility-normalized and lookback-invariant, so the subtraction is between two comparable, unitless momentum readings, and the result is a clean relative-strength signal with the dollar removed.

$$ \text{Signal}_{\text{EUR vs GBP}} = \text{CMMA}_{\text{EURUSD}} - \text{CMMA}_{\text{GBPUSD}} \;\approx\; \text{momentum}(\text{EUR}) - \text{momentum}(\text{GBP}) $$

The cross-pair signal is the CMMA of EURUSD minus the CMMA of GBPUSD, which approximates the momentum of EUR minus the momentum of GBP. A positive value says EUR is gaining on GBP regardless of the dollar; a negative value says GBP is gaining on EUR. You trade it through EURGBP, going long EURGBP when EUR's normalized momentum leads and short when GBP's does.

What the signal is and is not

The honest read on what you have built and what it can do.

It is a relative-strength rotation between two correlated currencies, the FX analogue of the ratio signal from "Using Ratios as Trading Signals". It is not a prediction that EUR causes GBP; it is a measurement of which of the two is stronger right now with the common dollar driver stripped out. The edge, if any, comes from EUR and GBP responding at slightly different speeds or magnitudes to their own drivers (UK-specific rates and politics for GBP, euro-area rates and politics for EUR), so the relative-strength line trends when one currency's story is running ahead of the other's.

The naive version (trade GBPUSD off EURUSD without subtracting the dollar) fails because it is mostly a dollar bet wearing a cross-pair costume. When it appears to work, it works because the dollar trended, and you would have done as well or better trading the dollar directly. The subtraction is what separates a genuine EUR-versus-GBP signal from a disguised dollar position, and skipping it is the single most common cross-pair mistake.

The traps

Where the clean signal still bites.

EURGBP is less liquid and wider-spread than the two majors, so the relative-strength edge, which is small to begin with, faces a larger cost hurdle, the cost-versus-edge constraint from "Why Transaction Costs Should Be Added Before You Fall in Love". A signal that looks profitable on mid-price differences can die on the EURGBP spread.

The cancellation is exact only if the two pairs share the same dollar move over the same window, which holds for synchronous data but breaks across illiquid hours or asynchronous closes, leaving a residual dollar contamination in the difference. Use synchronous, liquid-hour data or the residual reintroduces the very thing you subtracted out.

The relationship drifts. EUR and GBP are correlated because of overlapping European exposure, and that overlap changes with events (a UK-specific shock decouples GBP for a while). The relative-strength signal is non-stationary like every relationship in this pillar, so it needs the rolling re-estimation the article "Slow Wandering: The Most Dangerous Type of Market Change" demanded. Two currencies that decoupled this year may not give the same signal next year.

Visualizing the dollar cancellation

KEY POINTS

- EURUSD and GBPUSD move together because they share the dollar: both are something-over-USD, so a dollar move drags both the same way. The correlation is the dollar talking, not EUR predicting GBP.

- This is the third-variable confound: two series correlate because a common factor drives both, not because one causes the other. A naive "trade GBP off EUR" signal is mostly a disguised dollar bet.

- In log returns each pair is a difference: EURUSD is EUR strength minus USD strength, GBPUSD is GBP strength minus USD strength. Both carry the same minus-USD term.

- Subtracting the two pair returns cancels the shared USD term exactly, leaving EUR strength minus GBP strength, which is what EURGBP measures with no dollar in it.

- The practical signal: CMMA of EURUSD minus CMMA of GBPUSD. CMMA is volatility-normalized and lookback-invariant, so the difference is between two comparable momentum readings and yields a clean relative-strength signal.

- Positive means EUR is gaining on GBP regardless of the dollar; negative means GBP is gaining. Trade it through EURGBP, long when EUR's normalized momentum leads and short when GBP's does.

- It is a relative-strength rotation, not a causal prediction. The edge comes from EUR and GBP responding at different speeds to their own drivers, so the relative line trends when one story runs ahead of the other.

- Traps: EURGBP is less liquid and wider-spread, raising the cost hurdle on a small edge; the cancellation needs synchronous liquid-hour data or residual dollar contamination returns; and the EUR-GBP overlap drifts, so the signal needs rolling re-estimation.

References

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- Triangular Arbitrage, Market Microstructure, and Correlation in Foreign Exchange Markets

- The Microstructure of Foreign Exchange Markets

- FX Market Metrics: New Findings Based on CLS Bank Settlement Data

- Lead-Lag Relationships in Market Microstructure

- Dissecting Investment Strategies in the Cross Section and Time Series

- Preprint: Comparing the Forecasting Ability of Correlation Forecasts in the CEE FX Market

- High-Frequency Trading, Asset Pricing, and Market Microstructure

- Deep Limit Order Book Forecasting: A Microstructural Guide

- Currency Factors

- A global perspective on exchange rate dynamics via currency factors

- Return Spillovers Between Currency Factors

- Currency Centrality in Global Equity Markets

- Crisis-dependent linkages in major exchange rates

- Liquidity in the global currency market

- What Makes the Missing Risk Premium in Exchange Rates Stationary

- Short-term Trading Strategy on G10 Currencies

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.