2.41 Momentum Is a High-Pass Filter

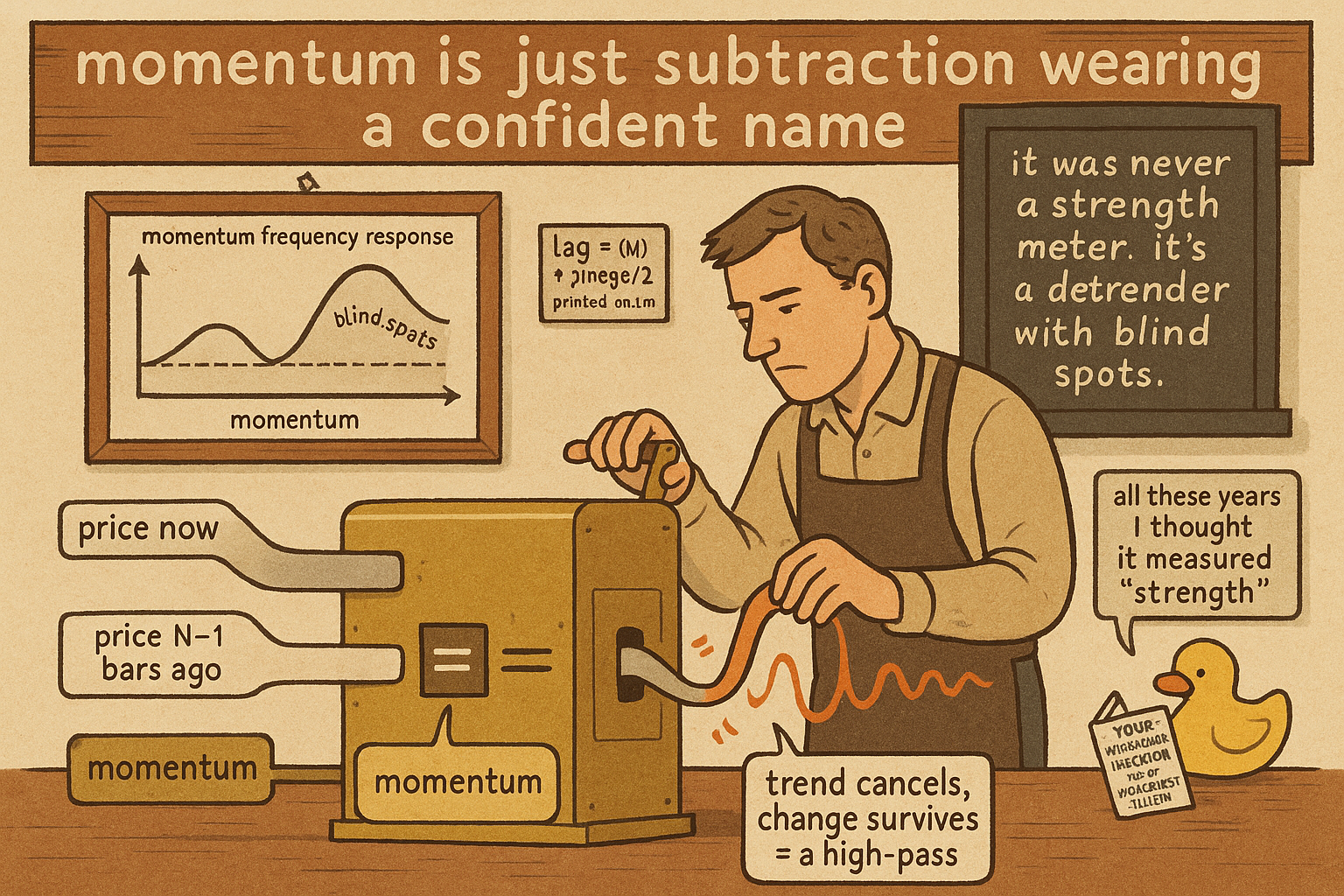

Momentum is price now minus price N-1 bars ago, a high-pass filter: it kills the trend, peaks on a passband set by N, goes blind at nulls, and lags by (N-1)*omega/2. Not a strength gauge.

Traders treat momentum as a strength gauge: price now minus price N bars ago, big when the market is moving, small when it is not. The old article "High-Pass Filters for Traders" built detrenders that keep the fast deviations and throw away the slow trend. This article collapses the distinction, because they are the same thing. Momentum is a high-pass filter, exactly and provably, and writing out its frequency response tells you precisely which cycles it amplifies, which it kills, and how many bars late it reports them. The strength-gauge framing hides all of that. The filter framing exposes it.

Momentum is a first-degree causal high-pass

The momentum indicator is one subtraction: today's price minus the price from N minus one bars ago.

$$ y(n) = x(n) - x\big(n - (N-1)\big), \qquad N > 2 $$

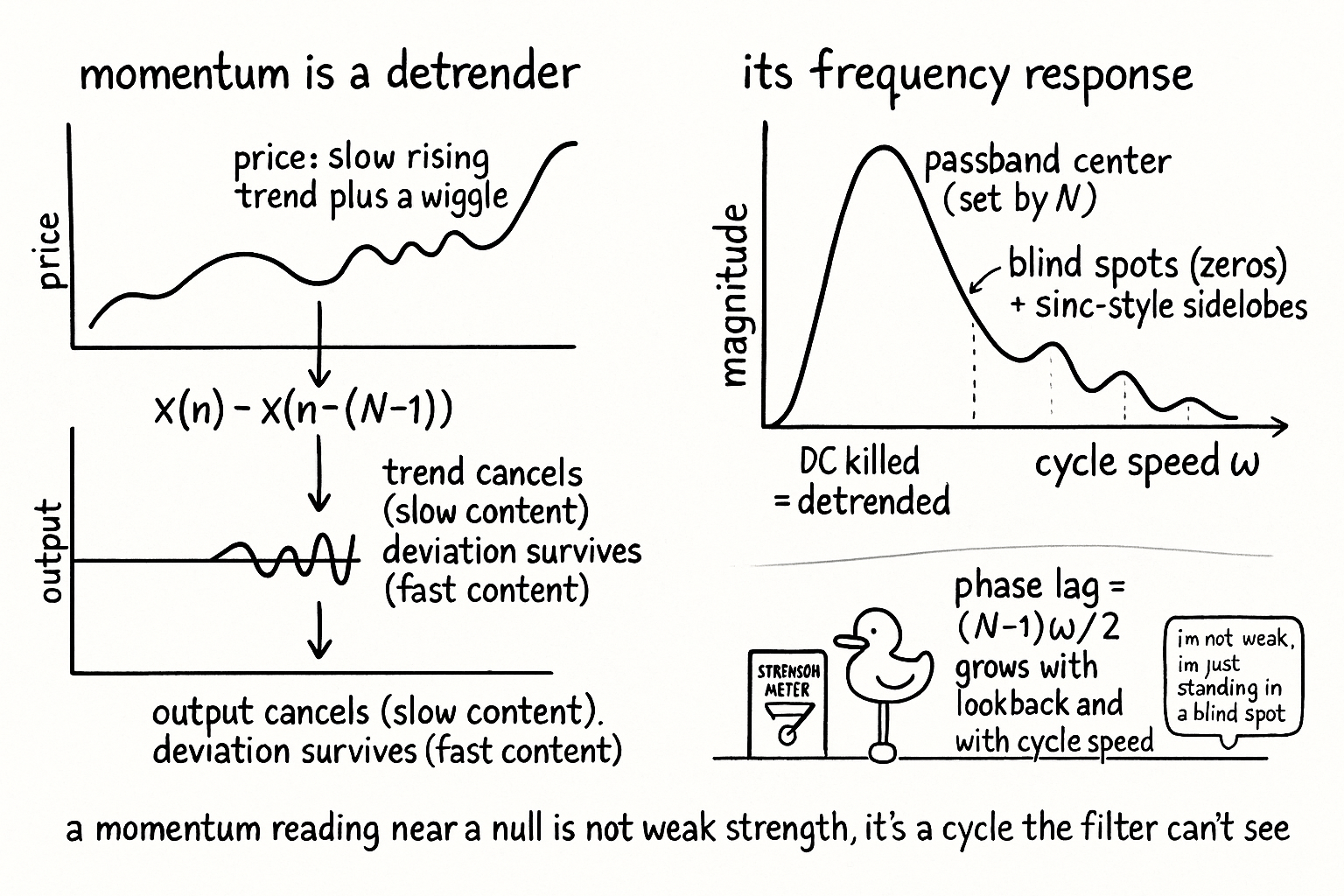

That is a high-pass filter, structurally, the simplest member of the family from the old high-pass article. It subtracts a delayed copy of the price from the present price. Whatever is slow, the trend, is nearly the same value now as N minus one bars ago, so it cancels in the subtraction. Whatever is fast, the recent change, survives. Subtracting a delayed copy is the definition of a first-degree, polynomial-of-degree-one detrender, so momentum kills the trend and keeps the deviation. The strength-gauge intuition is downstream of this: momentum looks big during fast moves because a high-pass passes fast content.

The frequency response: what it really keeps and kills

Take the transfer-function view and the behavior is no longer a story, it is a curve. Put the delay operator on the unit circle and the frequency response of momentum is a complex number you can split into magnitude and phase.

$$ H(\omega) = 1 - e^{-i(N-1)\omega} = 2\sin\!\left[\tfrac{(N-1)\omega}{2}\right] e^{\,i\left(\frac{\pi}{2} - \frac{(N-1)\omega}{2}\right)} $$

The magnitude is twice the sine of (N minus one) times omega over two. Read it at the ends. At zero frequency, the trend, the magnitude is zero: momentum annihilates the DC level, which is what makes it a detrender. As frequency rises the magnitude climbs, so momentum amplifies faster cycles, up to a peak. Past that peak the sine turns over and the response develops nulls and lobes, the same sinc-shaped sidelobe structure the old article "Why the SMA Is Often a Terrible Smoother" warned about, because momentum is an N-tap difference, not a clean filter. So momentum is not a uniform strength gauge. It has zeros at specific cycle periods, where it is blind, and a passband centered on a particular speed set by N. A momentum reading near a null is not weak strength; it is a cycle the filter cannot see.

The phase lag is structural and computable

The exponential factor carries the timing, and it splits into two parts. There is a constant phase lead of pi over two, the quarter-cycle advance a differencer gives, and a frequency-dependent phase lag.

$$ \text{phase lag} = \frac{(N-1)\,\omega}{2} $$

That lag grows with the lookback N and with the cycle speed omega, so a longer momentum reports turns later, and it reports fast cycles later than slow ones. This is not an accident of implementation, it is in the transfer function, computable before you ever run it, which is exactly what the old article "How to Think About Indicator Lag Before Backtesting" demanded: know each indicator's lag from the formula and add it into the budget. Momentum's contribution is (N minus one) times omega over two at the cycle you care about.

Two practical consequences fall out. First, choosing the momentum lookback N is not choosing a sensitivity, it is choosing a passband center and a lag together, and you cannot move one without the other. A short N passes fast cycles with little lag but rejects the slow swings you may want; a long N reaches slower cycles but lags them more and plants its blind nulls at periods that may matter. Second, stacking momentum with another high-pass detrender is not confirmation; if they share a band they are one filter counted twice, the redundancy the frequency-response article kept flagging. Pick the momentum lookback by the cycle band you want to isolate and the lag you can afford, both of which the frequency response hands you in closed form, not by which number looked good on a chart.

KEY POINTS

- Momentum, price now minus price N minus one bars ago, is a first-degree causal high-pass filter: it subtracts a delayed copy of price, so the slow trend cancels and the fast deviation survives. It is the same object as the detrenders in the old article "High-Pass Filters for Traders."

- Its frequency-response magnitude is 2sin[(N-1)omega/2]: zero at DC (it kills the trend), rising to a passband peak, then nulls and sidelobes, the sinc-style leakage of any N-tap difference.

- So momentum is not a uniform strength gauge. It has blind spots (zeros) at specific cycle periods; a reading near a null is a cycle the filter cannot see, not weakness.

- The phase lag is (N-1)*omega/2, computable from the formula, growing with the lookback N and the cycle speed. This is the lag-before-backtest discipline of the old article "How to Think About Indicator Lag Before Backtesting" applied to momentum.

- Choosing N is choosing a passband center and a lag together; you cannot tune sensitivity without moving both, and you plant blind nulls at periods set by N.

- Stacking momentum with another high-pass that shares its band is one filter counted twice, not confirmation. Pick N by the target cycle band and affordable lag, both given in closed form.

References

- Statistically Sound Indicators for Financial Market Prediction - Timothy Masters (Amazon)

- Cycle Analytics for Traders - John Ehlers (Amazon)

- Finite impulse response filters and the comb/difference response (Wikipedia)

- The Scientist and Engineer's Guide to Digital Signal Processing: difference and derivative filters

- Momentum, rate of change, and detrending in technical analysis (Wikipedia: Momentum)

- Group delay and phase delay of FIR filters (Wikipedia)