2.40 Wave Velocity and Acceleration: Reading When the Market Runs Out of Gas

Model price as a local sine and its velocity and acceleration are exact derivatives, with no differencing lag. Acceleration flags a swing running out of gas early, but rides on a fragile sine fit.

The old article "Why Moving Averages Can Lie at Turning Points" showed that a moving average reports the turn late, because its slope flips bars after the price does. The old article "The Hidden Cost of Every Moving Average: Lag" priced that delay. Both leave a question open: is there a way to read the turn early, from the shape of the move itself? If you accept the local sine model from the previous article, the answer is yes. The sine has an exact derivative, so its velocity and acceleration are available with no smoothing and no lag, and the acceleration is the cleanest early read on a market running out of gas. The catch is that all of it inherits the sine model's fragility.

Velocity and acceleration come free from the sine model

Once you model price locally as a sine, you do not estimate its slope numerically; you differentiate the model. The first derivative is the velocity, the rate price is moving.

$$ v = A\,\omega \cos(\omega t + \varphi) $$

The second derivative is the acceleration, the rate the velocity itself is changing.

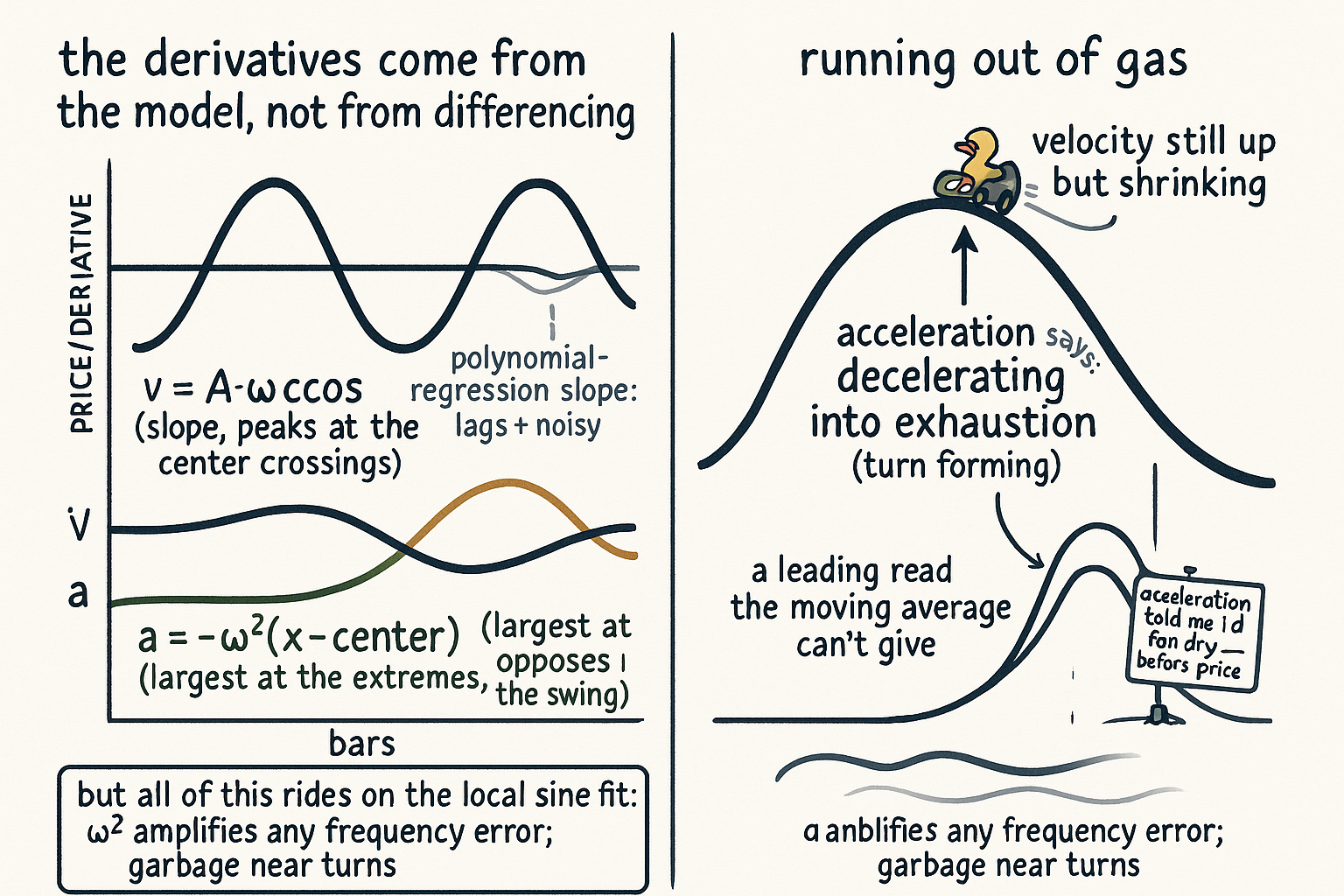

$$ a = -A\,\omega^2 \sin(\omega t + \varphi) = -\omega^2 (x - D) $$

Read what the acceleration says. It is the price swing flipped in sign and scaled by frequency squared. When price is stretched far above its center, acceleration points hard down, pulling back; when price is far below, it points hard up. Acceleration is largest in magnitude at the extremes and zero as price crosses its center at full speed. That is the signature of a market losing momentum at the edges of a swing, which is the early-warning the lagging moving average could never give.

No phase lag, unlike a numerical slope

Here is the property that makes this worth the trouble. Differentiating an analytic model introduces no phase lag. The velocity and acceleration are evaluated at the current bar from the fitted sine, not built by differencing past bars, so they do not trail the price the way a numerical derivative or a polynomial-regression slope does. Don Mak's point is direct: computing velocity and acceleration from the sine model gives a reading with no phase or lag shift, which makes it more accurate than fitting a polynomial and differentiating that.

The contrast matters. A polynomial-regression slope, or any finite-difference derivative, is a weighted sum of past bars, so it carries the same structural lag as every causal filter and it amplifies noise on top. The sine model sidesteps the lag by committing to a functional form and reading its exact derivative at the present bar. You trade a model assumption for the elimination of differencing lag. When the assumption holds, that is a genuinely better derivative. When it does not, you have an exact derivative of the wrong function.

Acceleration as an exhaustion signal, with the model's fine print

The practical payoff is an exhaustion read. The market can turn down, catch a second wind, and charge back up, and price alone or a lagging average will not tell you which is happening until it is over. Acceleration can, because it measures whether the move is still gaining or already fighting itself. Acceleration opposing velocity, growing in magnitude while price extends, says the swing is decelerating into exhaustion, a turn forming before the price confirms it. Acceleration aligned with velocity says the move still has fuel. This is a leading read on the turn, the thing the old turning-point article said moving averages structurally cannot deliver.

The fine print is the whole sine model, and it does not get smaller because we took derivatives. Every value here depends on omega, A, and phi estimated locally, and the previous article showed that local frequency estimate is high-variance and explodes near turns, which is exactly where you want to read acceleration. So the exhaustion signal is sharpest in theory at the moment it is least reliable in practice. Differentiating twice multiplies the sensitivity: acceleration carries the factor omega squared, so any error in the frequency estimate is amplified hard. The discipline is the same as before. Gate the signal on a real, persistent cycle with adequate amplitude, smooth the inputs enough to survive the noise without giving back all the lead, and treat a clean acceleration reversal in a trending or choppy regime as an artifact of a model that does not fit, not as a signal. Used inside its assumptions it is a rare leading indicator. Used outside them it is confident nonsense.

KEY POINTS

- If you accept the local sine model, velocity and acceleration are exact derivatives of the model, not numerical differences of past bars, so they come with no smoothing and no differencing lag.

- Velocity is Aomegacos: largest as price crosses its center at full speed. Acceleration is minus omega-squared times the swing (price minus center): largest at the extremes, opposing the move.

- Differentiating an analytic model adds no phase lag, unlike a polynomial-regression slope or any finite-difference derivative, which lag and amplify noise. You trade a model assumption for the removal of differencing lag.

- Acceleration is an exhaustion read: opposing and growing while price extends means the swing is decelerating into a turn, a leading signal the old article "Why Moving Averages Can Lie at Turning Points" said averages cannot give.

- The whole thing rides on the sine fit's local frequency estimate, which the previous article showed is high-variance and worst near turns, the exact place you want acceleration. The omega-squared factor amplifies any frequency error.

- Use it gated on a persistent cycle with real amplitude, smoothed enough to survive noise; treat a clean acceleration reversal in a trend or chop as a model artifact, not a signal.

References

- Statistically Sound Indicators for Financial Market Prediction - Timothy Masters (Amazon)

- Cycle Analytics for Traders - John Ehlers (Amazon)

- Instantaneous phase and frequency (Wikipedia)

- Savitzky-Golay filter: derivatives from a local polynomial fit (Wikipedia)

- Numerical differentiation and noise amplification (Wikipedia)

- Trend Without Hiccups: A Kalman Filter Approach (velocity and acceleration states, arXiv)