4.67 Correlation Regimes: Positive Feedback, Breakdowns, and "USDCAD Is the Truth"

FX correlation is a regime that feeds on itself until it snaps without warning. Measure it rolling, watch USD pairs move as a bloc, and use "USDCAD is the truth" only when oil is asleep.

In 2008 the correlation between FX and every other asset class ran to one. Stocks, credit, commodities, the high-beta currencies all sold together, and the safe havens all caught the bid together, and the individual currency stories that fill the rest of this pillar stopped mattering for months. A trader who had spent years learning that the Aussie tracks copper and the loonie tracks crude watched both pairs move on a single variable: are we risk-on or risk-off today. The drivers had not disappeared. They had been swamped by a correlation regime, and the regime was the only thing worth knowing.

Correlation in FX is not a constant you measure once and bolt into a model. It is a regime that builds, reinforces itself, and then snaps. The old article "Intermarket Analysis for System Traders" named non-stationary, sign-flipping correlation as the central trap of the whole discipline, and this article works the specific shape that non-stationarity takes in currencies: correlations rise through positive feedback until a regime shift breaks them, USD pairs move as a bloc, and one pair (USDCAD) gets used as the cleanest read on the bloc.

Correlation feeds on itself until it breaks

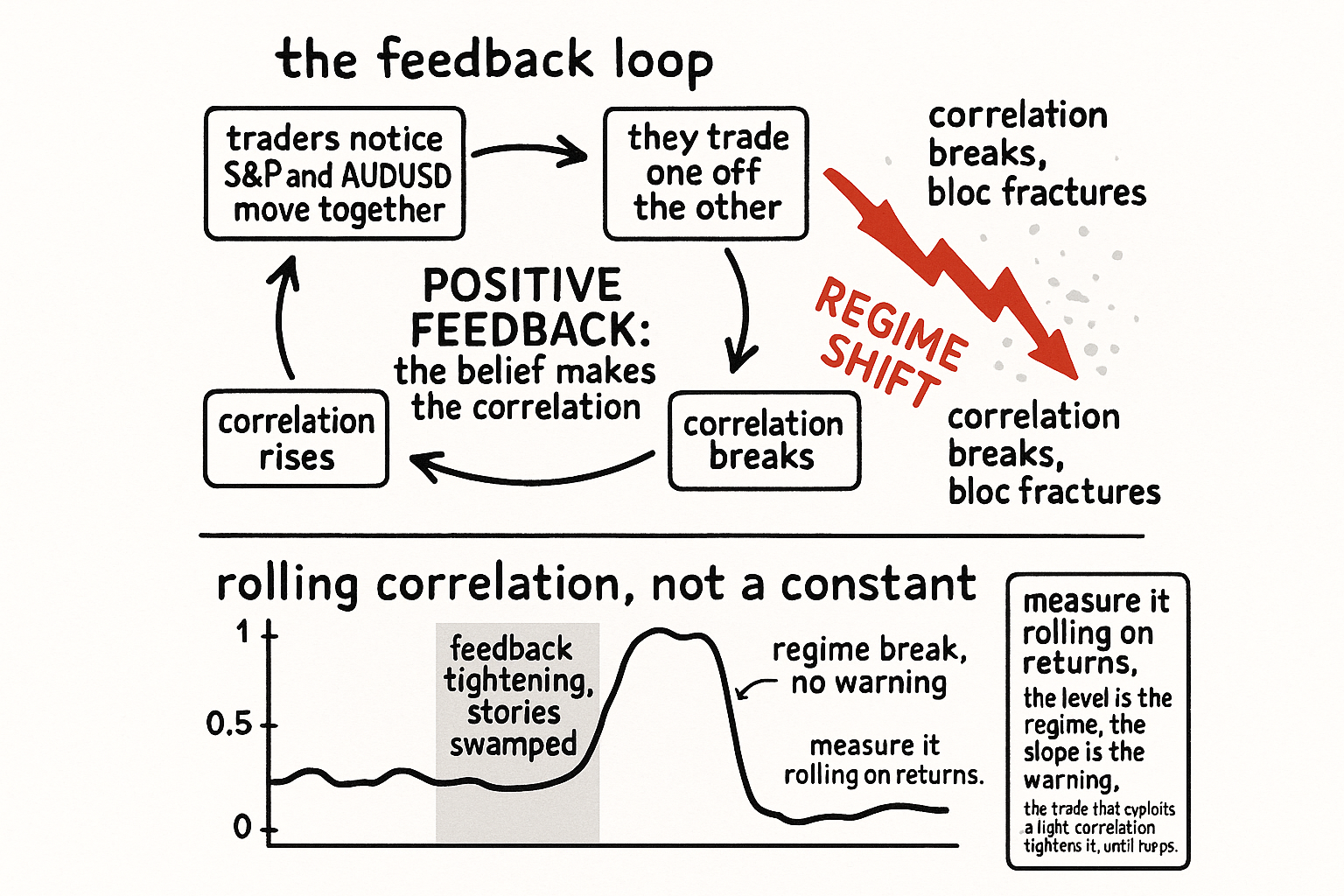

A rising correlation is not a passive measurement. It is a process that reinforces its own cause. When traders notice that the S&P 500 and AUDUSD have been moving together, they start trading one off the other: a down day in stocks becomes a reason to sell the Aussie, which makes the Aussie fall when stocks fall, which tightens the very correlation that prompted the trade. The belief in the correlation manufactures more of it. Picture global capital as one connected organism, where a move in one limb propagates to the others through the traders who arbitrage the links, and the propagation gets faster as more participants act on it.

This positive feedback is why correlations do not drift gently. They ratchet toward one in stress, because stress is when everyone reaches for the same simple variable (risk appetite) and trades every instrument as a proxy for it. The old article "Why FX Traders Must Watch Gold, Rates, and Equities" caught the endpoint of this process in the 2008 jump to one; the mechanism is the feedback loop that gets it there. The trade that exploits a tight correlation is the trade that tightens it further, right up until the regime shifts.

And the regime does shift. A central bank surprise, a change in the dominant macro story, a single currency suddenly trading on its own domestic event, and the bloc fractures. The correlation that was 0.9 for six months is 0.2 for the next three, or flips sign entirely. The danger is structural: the feedback that built the correlation gives no warning before it breaks, because the same crowd that reinforced it unwinds it, and the unwind is faster than the build. A strategy that earned its edge from a tight correlation is short a regime change it cannot see coming, the same acceptance the old article "Why Systems Work Until They Don't" built into every relationship in this project.

Measuring the regime instead of assuming it

Read the correlation as a rolling, time-varying number, never a single historical figure. Compute it over a trailing window of returns and watch the path, not the point.

$$ \rho_t = \frac{\sum_{i=t-N+1}^{t} (x_i - \bar{x})(y_i - \bar{y})}{\sqrt{\sum (x_i - \bar{x})^2}\,\sqrt{\sum (y_i - \bar{y})^2}} $$

This is the ordinary correlation between two return series x and y, computed only over the last N bars and recomputed every bar, with the bars sliding the window forward. Use returns, not prices, or you measure a shared trend and call it correlation. A worked feel: with N = 60 daily bars, the S&P-AUDUSD correlation might read 0.35 in a calm spring, climb to 0.80 through a summer growth scare, and sit near 0.85 in an autumn panic. The level is the regime, and the slope is the warning; a correlation marching toward one is telling you the individual stories are being swamped, and a correlation rolling over from a high level is telling you the bloc is starting to fracture.

The window length is the usual arbitrary dial. Short windows react fast and jump around on noise; long windows are stable and blind to the regime change you most want to catch. There is no correct N, only a trade between reactivity and stability, and the honest move is to watch two windows (a fast one for the warning, a slow one for the state) rather than pretend one number is the truth.

USD pairs move as a bloc, and EURUSD speaks for it

Most of what looks like a hundred separate currency markets is one variable wearing different clothes. Every USD-based pair shares the dollar leg, so when the dollar moves, EURUSD, AUDUSD, GBPUSD, and the rest move together by construction, the same shared-USD mechanism the old article "Cross-Pair Signals: Can EUR Predict GBP?" used to cancel the dollar out of a cross. The bloc behavior is not a discovered correlation; it is arithmetic. A dollar move is common to all of them.

EURUSD is the loudest voice in the bloc because it is the most liquid and the pair most speculators use to express a dollar view. A large EURUSD move is the cleanest signal that the dollar itself is moving, and that move drags the other USD pairs with it. Watching EURUSD is watching the common factor, which is why a trader holding AUDUSD or GBPUSD ignores EURUSD at their peril: a sharp EURUSD move says the thing your pair shares with every other USD pair just changed.

"USDCAD is the truth"

Some traders trust USDCAD above every other pair as the read on the dollar, to the point it has earned the nickname "the truth." The logic is that the Canadian dollar is the G10 currency closest to the United States in economy, trade, and time zone, so USDCAD strips out a lot of the foreign-side noise that muddies the other pairs and leaves a comparatively clean dollar signal. EURUSD carries European politics, Italian yields, and ECB policy on its non-dollar leg; USDJPY carries the entire risk-haven and carry complex on the yen leg; USDCAD's loonie leg is the quietest of the majors when oil is not the story, so the pair moves on the dollar more purely.

Treat the nickname as a heuristic, not a law. USDCAD is a clean dollar read only when crude is dormant, because the old article "Crude Oil, Inflation, and FX" showed the loonie is an oil currency, and a sharp move in crude makes USDCAD a Canada story rather than a dollar story. The honest use of "the truth" is conditional: when the USD pairs disagree and you need a tiebreak on whether the dollar is really moving, USDCAD is a good arbiter as long as oil is not the thing that moved. When oil is moving, USDCAD is lying to you about the dollar, and EURUSD is the better common-factor read.

Trading the regime, and the honest limits

The operational use has two sides. First, defense: do not run an intermarket or cross-pair strategy as if its correlations are fixed. Gate it on the rolling correlation the way the old article "Using Bonds to Filter Equity Signals" gated on the rolling stock-bond correlation, suspending or resizing the strategy when the regime moves against its assumptions. A pairs trade or a relative-value cross built in a 0.3-correlation regime behaves like a different instrument at 0.9, and a market-neutral book stops being neutral when everything correlates to one.

Second, offense, with heavy caveats. A divergence inside a tight bloc is a candidate signal: if USD pairs are moving together and one lags the move EURUSD or USDCAD just made, that laggard is a catch-up candidate, the bloc version of the divergence logic from the old article "Intermarket Divergence as a Trading Filter." The edge is thin and the catch comes with the usual lead-lag fragility from "Lead-Lag Relationships in Global Markets": the lag may be the laggard pricing in a genuine domestic difference rather than waiting to catch up, in which case fading the divergence is fighting real information.

The limits are the same ones that run through every correlation in this pillar, sharpened by the feedback mechanism. Correlations are non-stationary and the breakdown comes without warning because the crowd that built it unwinds it. A high correlation is not three independent confirmations; when the bloc moves to one, your "diversified" FX book is one position. The rolling window is an arbitrary choice trading reactivity against stability. And the regime that makes correlation-based filters most attractive (everything tightly linked, signals clean) is exactly the regime sitting closest to the break, so the filter works beautifully right up to the moment it costs you the most.

KEY POINTS

- Correlation in FX is a regime, not a constant. It rises through positive feedback (traders trade one market off another, which tightens the link that prompted the trade) until a regime shift snaps it, and the snap comes without warning because the crowd that built it unwinds it.

- In 2008 FX-asset correlations ran to one and individual currency stories stopped mattering for months. Stress drives every instrument toward a single variable (risk appetite).

- Measure correlation rolling on returns over a trailing window, never as one historical number. The level is the regime, the slope toward one is the warning. The window length is an arbitrary reactivity-versus-stability dial; watch a fast and a slow window.

- USD pairs move as a bloc by arithmetic, because they share the dollar leg. EURUSD is the loudest voice and the cleanest read that the dollar itself is moving, so a sharp EURUSD move warns every other USD pair.

- "USDCAD is the truth" because the loonie leg is the quietest major when oil is dormant, leaving a comparatively pure dollar signal. The nickname is conditional: when crude moves, USDCAD becomes a Canada story and lies about the dollar, so use EURUSD instead.

- Defense: gate intermarket and cross strategies on the rolling correlation, since a market-neutral book stops being neutral when everything correlates to one. Offense: a laggard inside a tight bloc is a thin catch-up candidate, with the usual lead-lag fragility.

- The regime that makes correlation filters most attractive (clean, tightly linked) sits closest to the break, so the filter works best right before it hurts most.

References

- Pearson correlation coefficient (Wikipedia)

- Correlation does not imply causation (Wikipedia)

- On the Network Topology of Variance Decompositions (Diebold & Yilmaz, connectedness in crises)

- Asymmetric Correlations of Equity Portfolios (Ang & Chen)

- Rolling-window correlation (pandas docs)

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- International Asset Allocation with Time-Varying Correlations

- Regime Switching for Dynamic Correlations

- Correlation Regimes in International Equity and Bond Returns

- Stock Market Volatility and Exchange Rates in Emerging Countries: A Markov-State Switching Approach

- Dynamic Linkage Between Real Exchange Rates and Stock Prices: Evidence from Developed and Emerging Asian Markets

- Dynamic Correlation Analysis of Financial Contagion: Evidence from the Central and Eastern European Markets

- Exchange Rate Regimes and Market Integration: Evidence from the Dynamic Relations Between Renminbi Onshore and Offshore Markets

- Liquidity in the Global Currency Market