5.33 Positional Market Making and the Thousands-of-Alphas Ensemble

A big maker's PnL isn't the spread, it's positional: skewing thousands of weak alphas into passive quotes. Zero cost makes half-bp signals tradeable, and ensembling them cancels noise into the bulk of the profit.

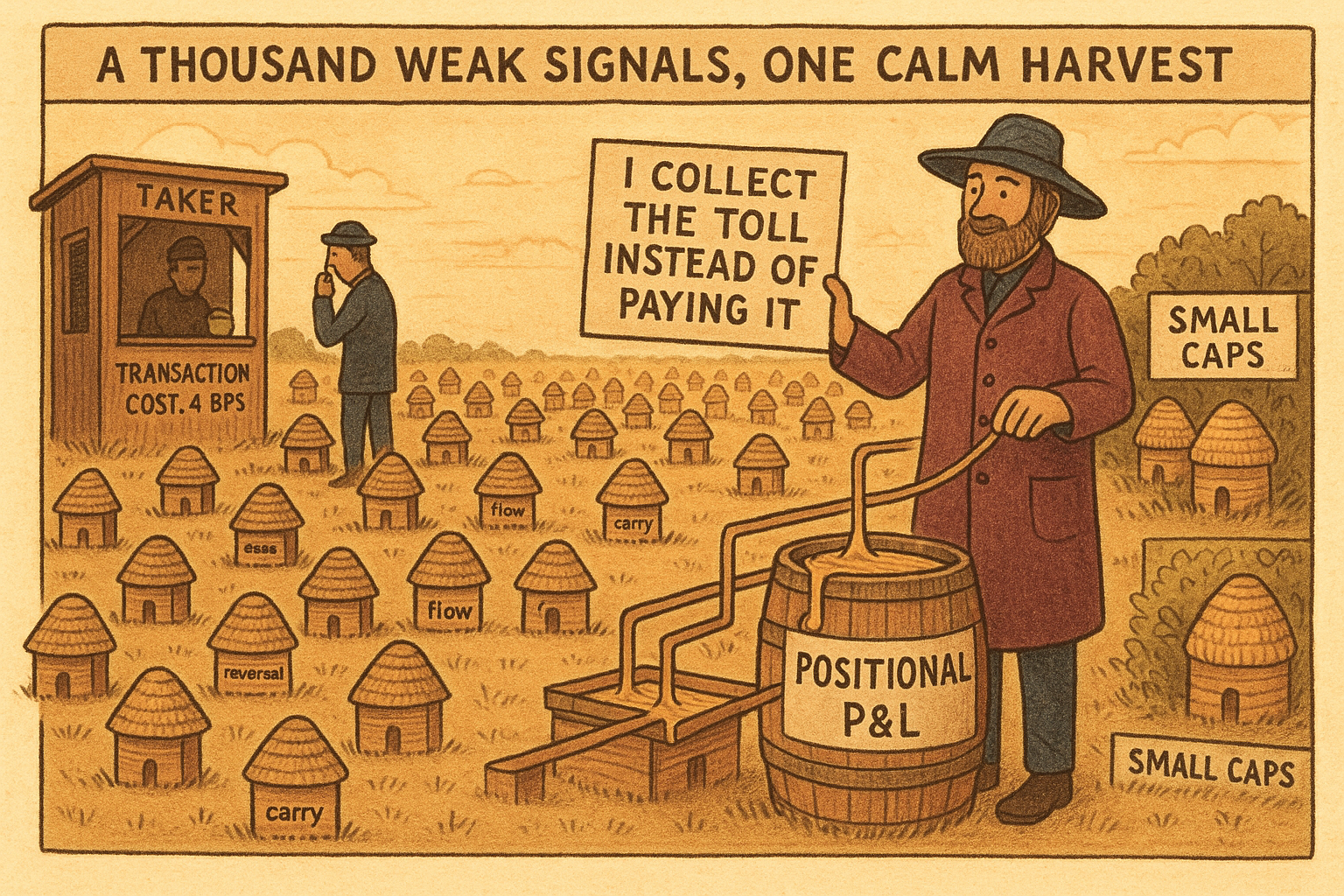

Ask where a large market maker's money comes from and the textbook answer is the spread: post a bid, post an ask, collect the difference, repeat. That answer describes maybe the smallest part of the business. The bulk of the PnL at a serious desk comes from positional market making, using the quoting machine as a delivery mechanism for medium-frequency alpha, and running thousands of small skews at once rather than a handful of clever ones.

This is the synthesis of two threads. The old article "Why Small Alphas Matter More for Makers Than Takers" established that a signal worth half a basis point is garbage to a taker and money to a maker, because the maker collects the spread instead of paying it. The old article "Maker vs Taker Edge: Same Signal, Different Economics" showed the same signal becomes two different businesses depending on which side of the spread you sit. This article is what you build once you accept both: an ensemble of weak alphas skewed into passive quotes across a wide universe.

Market making as a medium-frequency alpha delivery system

Reframe the quote. A maker's fair value is the center, skew leans it toward where you want inventory, and spread sets the width. Skew is usually described as inventory management, but it is also a steering wheel: skewing your quotes toward the long side accumulates a long position passively, by being filled rather than by crossing the spread. So any signal that says "this name should go up" can be expressed as a skew, and you end up long without ever paying to take.

That is positional market making, market making bent into a medium-frequency alpha. You are not scalping the spread in milliseconds; you are using passive fills to build positions a signal wants you to hold for seconds to minutes, collecting spread on the way in instead of paying it. The HFT spread-scalping book still runs, but the positional layer on top is where the size and the PnL live.

Why zero cost changes everything

The hinge is transaction cost, and for a maker it is effectively zero or negative, because you earn the spread rather than pay it. That single fact rewrites which signals are tradeable.

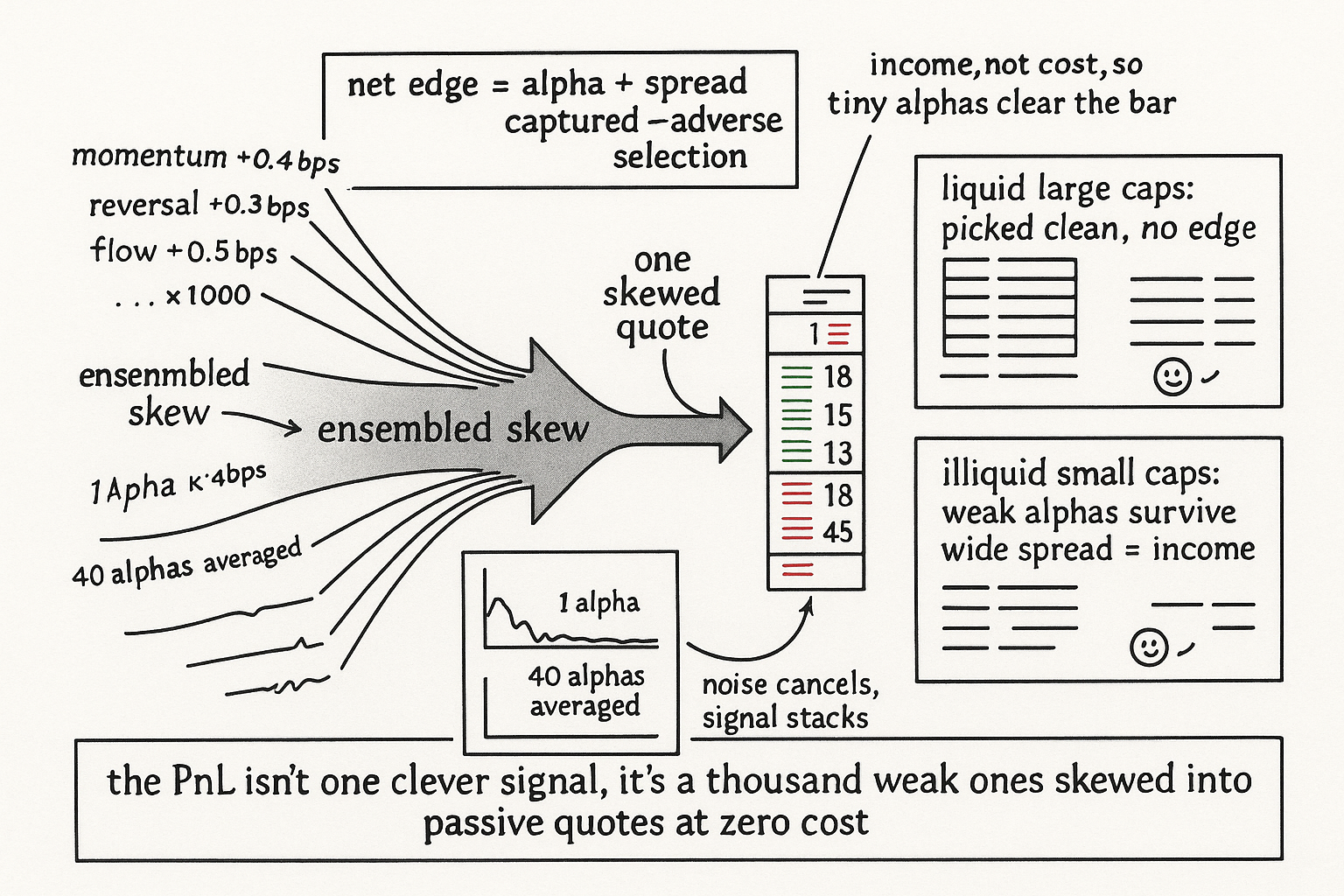

A taker contemplating a half-basis-point signal does the math: 0.5 bps of edge against 4 bps of round-trip cost is a guaranteed loser, so the signal is worthless and gets thrown away. The maker does the same math with the cost flipped to income: the half-bp signal sits on top of captured spread, so the break-even bar drops to the floor and the signal only has to beat the adverse selection it offsets. Signals that are trash to everyone paying costs are tradeable to the one party collecting them.

This is why expanding the universe helps so much. The resource puts it directly: zero cost to trade makes it easy to find edge, and pushing into a larger, less-efficient universe makes the same alphas perform better, because small caps carry more edge. Liquid large caps are picked clean; the thin, awkward, illiquid names are where weak signals survive, and a maker is exactly the participant who can quote them, because the wide spread there is income, not an obstacle. The old maker-vs-taker article made this point: cost pulls the maker toward illiquid wide-spread names while pushing the taker toward liquid tight ones.

The ensemble: thousands of skews

One half-bp alpha is not a business. The move is to find many of them and skew into all of them at once, ensembling the skews into the quote.

The reason this works is the same noise-cancellation logic that powers signal ensembling generally: each weak alpha is true signal plus noise, the true components correlate with future returns while the noise components do not, so summing many of them grows the signal and averages down the noise. None of the individual alphas survives standalone, but stacked into one skewed quote they compound into the bulk of the PnL. A desk running a thousand skews is not running a thousand strategies; it is running one ensembled fair-value lean built from a thousand weak inputs.

A concrete demonstration the resource suggests: backtest a plain ranking strategy on the log of past return times minus one, the one-hour reversal, with no fees. With costs it dies; without costs it works. Now imagine stacking dozens of effects like it, each individually marginal, all expressed as passive skews. That picture is how the positional PnL is generated, and the maker's zero-cost seat is the only one from which the picture is profitable.

$$ \text{skew}_{\text{total}} = \sum_{k=1}^{N} \alpha_k, \qquad \text{net edge}_k = \underbrace{\alpha_k}_{\text{signal}} + \underbrace{s}_{\text{spread captured}} - \underbrace{a_k}_{\text{adverse selection}} $$

Read the first sum as the total inventory lean being the sum of many small alpha skews. Read the second as a maker's per-alpha economics: the edge is the raw signal plus the spread you collect minus the adverse selection you pay, and because the spread term is positive income rather than negative cost, even a tiny alpha clears the bar. Stack N of them and the signal grows while the noise in the skews cancels.

A worked number

Say you have one momentum alpha worth 0.5 bps of edge per fill. Standalone, against a taker's 4 bps cost, it loses 3.5 bps a round trip, dead on arrival. As a maker capturing a 3 bps half-spread, that same alpha nets 0.5 + 3 − (some adverse selection); if adverse selection runs 2 bps, you net 1.5 bps per fill on a signal a taker had to discard. Now find forty more uncorrelated half-bp alphas. The signal in the combined skew grows roughly with the number of alphas while the noise grows with its square root, so forty alphas give you something like a six-to-seven-fold improvement in signal-to-noise over one, turning a pile of individually-marginal effects into a robust positional lean. The catch the small-alpha article flagged: you swapped explicit spread and fee cost for implicit adverse-selection cost, so if your defense, fair value and skew against toxic loading, is wrong, the adverse-selection term blows up and eats all forty alphas at once.

Where it sits

Positional market making is the bridge between the microstructure pillar and portfolio construction, which is why this article straddles Pillar 5 and 6. Each alpha is a microstructure or cross-sectional signal; the ensembling and universe expansion are portfolio decisions. The practical build order: get fair value right first because everything skews around it, get the toxic-flow defense right because it caps the adverse-selection term, then start bolting on weak alphas one at a time and let the ensemble do the work. Do not chase one brilliant signal. Collect many mediocre ones and let zero cost and the law of large numbers turn them into a business.

Visualizing the ensemble

KEY POINTS

- Most of a large maker's PnL is positional, not spread-scalping: using passive fills to build positions a medium-frequency signal wants to hold, collecting spread on the way in instead of paying it.

- Skew is a steering wheel, not just inventory management. Any "this should go up" signal becomes a skew toward the long side, accumulating the position passively.

- Zero (or negative) transaction cost rewrites which signals are tradeable. A half-bp alpha is a guaranteed loser to a taker paying 4 bps and a winner to a maker collecting spread, so the break-even bar drops to the floor.

- Expand the universe into illiquid small caps, where weak alphas survive and the wide spread is income. The maker is the only participant who can profitably quote those names.

- Ensemble thousands of weak skews: each is signal plus noise, the signals stack and the noise averages down, so individually-marginal alphas compound into the bulk of PnL. Signal grows with N, noise with root N.

- You traded explicit cost for implicit adverse-selection cost, so get fair value and toxic-flow defense right first, a broken defense blows up the adverse-selection term and eats every alpha at once.

References

- The Theory of Edge and Positional Market Making (practitioner writing)

- Cross-Sectional and Time-Series Reversal in Cryptocurrency Markets

- The Cross-Section of Expected Returns and Many Weak Predictors

- Ensemble Methods and Signal Combination in Quantitative Trading

- The Art of Currency Trading - Brent Donnelly (Amazon)

- A Position-Aware Trading Agent System for Real Financial Markets

- AlphaCrafter: A Full-Stack Multi-Agent Framework for Cross ... - arXiv

- Optimal Quoting under Adverse Selection and Price Reading - arXiv

- An Impulse Control Approach to Market Making in a Hawkes LOB

- Increase Alpha: Performance and Risk of an AI-Driven Trading

- An Impulse Control Approach to Market Making in a Hawkes LOB

- Resolving Latency and Inventory Risk in Market Making with ... - arXiv

- A Hybrid AI-Driven Trading System Integrating Technical Analysis