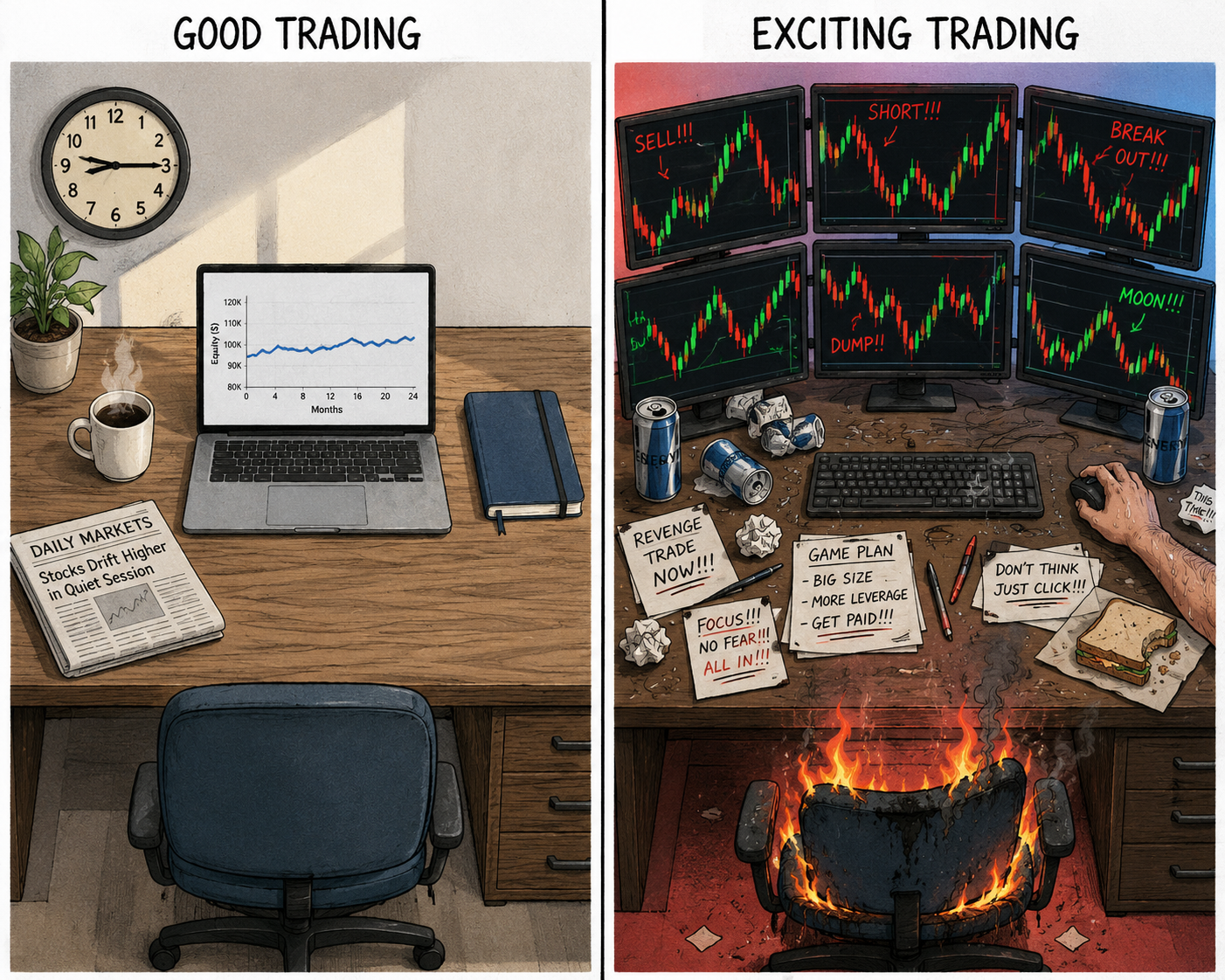

1.10 Why Good Trading Feels Boring

Excitement in trading is a warning sign. If your day produces emotional spikes, your positions are too big, your frequency is too high, or you are overriding the system. Good trading is engineered boredom: pre-computed signals, batched orders, vol-targeted sizing, and a fixed review cadence.

A trader who is excited about their day is doing something wrong. The dopamine is coming from somewhere that is not the edge. The edge is small, the variance per trade is small relative to the account, and the daily change in equity is small enough to forget about. If your trading day produces emotional spikes, the position sizes are too big, the strategy frequency is too high, the discretionary overrides are too frequent, or all three at once.

Good trading is boring by design. The boredom is the signature of a right-sized, automated, low-discretion system. Excitement is the warning sign that the trader is paying for entertainment with risk-adjusted returns.

The three features that make trading addictive

Three properties make any activity behave like a slot machine: the illusion of control, frequent near misses, and rapid continuous stimulation. Each one shows up in trading, and each one produces the wrong incentives.

The illusion of control. Picking your own setup, drawing your own trend line, calling your own entry feels like skill. The feeling is a manufactured byproduct of being the one who clicked the button. The real skill is in the rule, the sizing, and the kill criterion. The click is the smallest part of the chain.

Frequent near misses. A trade that almost worked is more emotionally engaging than a trade that worked outright or that lost outright. The "would have been a big winner if I had held two more bars" feeling is what keeps gamblers at the table. In trading, it is what keeps traders second-guessing their stops and adjusting their parameters in the wrong direction.

Rapid continuous stimulation. Day trading with one-minute charts produces a steady stream of micro-events. Each event is a small dopamine hit. The brain learns to seek the stream. The stream does not produce edge. It produces a behavioral addiction that looks like work.

Systematic trading removes all three. Pre-computed signals remove the illusion of control over each click. Volatility-targeted sizing flattens near misses into normal noise. Daily or longer evaluation removes the rapid stimulation. The trader keeps the edge and loses the entertainment.

Boredom in practice

A correctly run systematic strategy on a retail account, sized for a 10% annual volatility target on $100,000 of capital, produces daily P&L with a standard deviation of:

In plain words: annual volatility (10% in this case, set by the trader) times account capital (the dollar amount at risk) gives the dollar standard deviation per year. Divide by √252 (the number of trading days in a year) to get the standard deviation per day, because variance scales with time and standard deviation scales with the square root of time.

For the numbers above:

σ_daily = (0.10 × $100,000) / √252 ≈ $630.

That is the expected daily move. Most days will see equity change by less than $630. Big days might see $1,200 or $1,500. A bad day might be −$1,200. The numbers are small enough that the daily change does not justify watching the screen.

A trader running the same $100,000 with discretionary overrides, no volatility targeting, and one-minute scalping might see daily P&L with standard deviation of $4,000 to $6,000. The dopamine difference is the source of the appeal. The risk-adjusted return difference, after costs and behavioral errors, is in favor of the boring version.

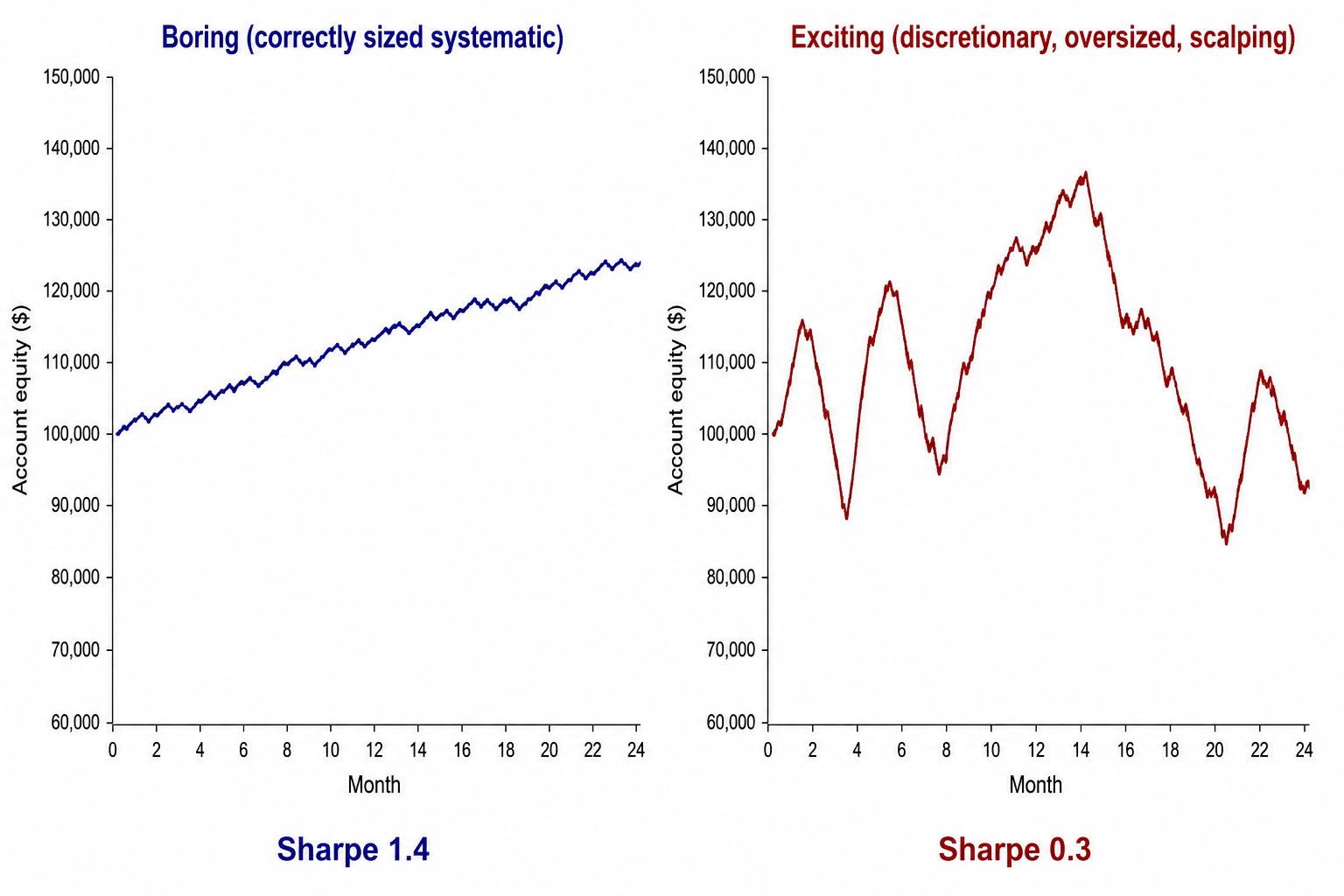

Boring equity curves vs exciting equity curves

The visual makes the asymmetry concrete. The boring curve and the exciting curve can end at similar levels. They are not similar products. The boring curve is reproducible across multiple traders running the same rules. The exciting curve is one path out of many possible paths, most of which end below $100,000.

The dopamine substitution problem

Removing excitement from trading creates a vacuum. The trader who used to get a hit from each click now has nothing to click. The brain looks for the missing stimulation. If the trader does not plan for this, the dopamine seeking returns through the back door.

The standard failure mode is "research" that is entertainment in disguise. The trader who removed discretionary trading from their day spends six hours a week reading market commentary, watching trader podcasts, and tweaking parameters that should not be tweaked. The activity feels productive. It produces no edge. It is the same dopamine search the trader was running before, with a more sophisticated label.

Two ways to handle the substitution.

The first is to channel the energy into research that has a measurable output. Build a new system, test a new instrument, run a permutation test on an existing rule. The research is bounded by an objective (find a signal, validate a hypothesis, retire a dead system) and produces an artifact (a notebook, a test result, a kill decision). The activity scratches the curiosity itch and adds to the trader's pipeline.

The second is to accept that trading does not have to fill the day. The boring trader spends 15 minutes a morning checking that systems ran correctly, batches the day's orders, and walks away. The other 7 hours are for something else. Not every job benefits from being a full-time obsession. Trading is one of the jobs that does not.

The career arc difference

The exciting trader's career arc looks dramatic in screenshots. Quick rise and steeper fall, posts during the rise and silence during the fall, then a return three years later with a new system and the same psychology. The screenshots circulate. The longitudinal P&L does not.

The boring trader's career arc looks tedious in screenshots and good in account statements. Mid-teens annual returns, single-digit drawdowns, same routine for ten years. The compound effect produces real wealth at a pace that does not photograph well.

The difference is psychological architecture, not skill at picking trades. The exciting trader optimized for the experience of trading. The boring trader optimized for the output of trading. The output is what compounds.

Designing for boredom

Boredom is the output of deliberate engineering. The operational moves.

Pre-compute signals before the market opens. The trader executes what the system picked, not what the trader felt like trading.

Batch orders to the broker once per day or once per session. Continuous order flow invites discretionary intervention; batched flow blocks it.

Size every position to a fixed fraction of the account, scaled by the instrument's volatility. Position size is a function of the rule's output and the volatility model, not a per-trade decision.

Remove the live equity feed during the trading session. The dollar value of unrealized P&L is irrelevant to any decision the trader needs to make. Watching it produces emotional engagement without informational gain.

Set a fixed weekly review window. Equity, drawdown, and decay metrics get reviewed once a week, with the trader away from the screen the rest of the week. The review is structured, the rest is not.

The set of moves above looks like restraint. It is also what produces the kind of trading that lasts thirty years instead of three.

KEY POINTS

- Excitement in trading is a warning sign. The dopamine is coming from oversized positions, high frequency, or discretionary overrides, not from the edge.

- Three addictive features (illusion of control, frequent near misses, rapid continuous stimulation) drive the experience of bad trading. Systematic processes remove all three.

- A correctly sized 10% annual volatility target on $100,000 produces daily P&L noise of around $630. The number is too small to be entertaining.

- Boring equity curves and exciting equity curves can end at similar levels. The boring curve is reproducible. The exciting curve is one survivorship-biased path out of many.

- Removing the dopamine from execution creates a vacuum. Channel the freed energy into bounded research that produces artifacts, or into something other than trading.

- The exciting trader optimized for the experience. The boring trader optimized for the output. Output compounds. Experience does not.

- Engineer boredom directly: pre-compute signals, batch orders, fix position size to a volatility model, hide the live equity feed, fix the review cadence.

References

- Evidence-Based Technical Analysis - David Aronson (Amazon)

- Systematic Trading - Robert Carver (Amazon)

- Evidence-Based Technical Analysis: Applying the Scientific Method and Statistical Inference to Trading Signals

- Quantitative Trading, Discretionary Trading, Hedge Funds, Market Efficiency and Price Discovery: A Literature Review

- The Science and Practice of Trend-following Systems

- The Power of Price Action Reading

- Who Profits From Trading Options?

- Retail Option Trading and Expected Announcement Volatility

- Algorithmic Trading Strategies for Superior Growth, Outperformance, and Risk Management

- A Comprehensive Review of Statistical Methods in Quantitative