2.55 The Autocorrelation Periodogram

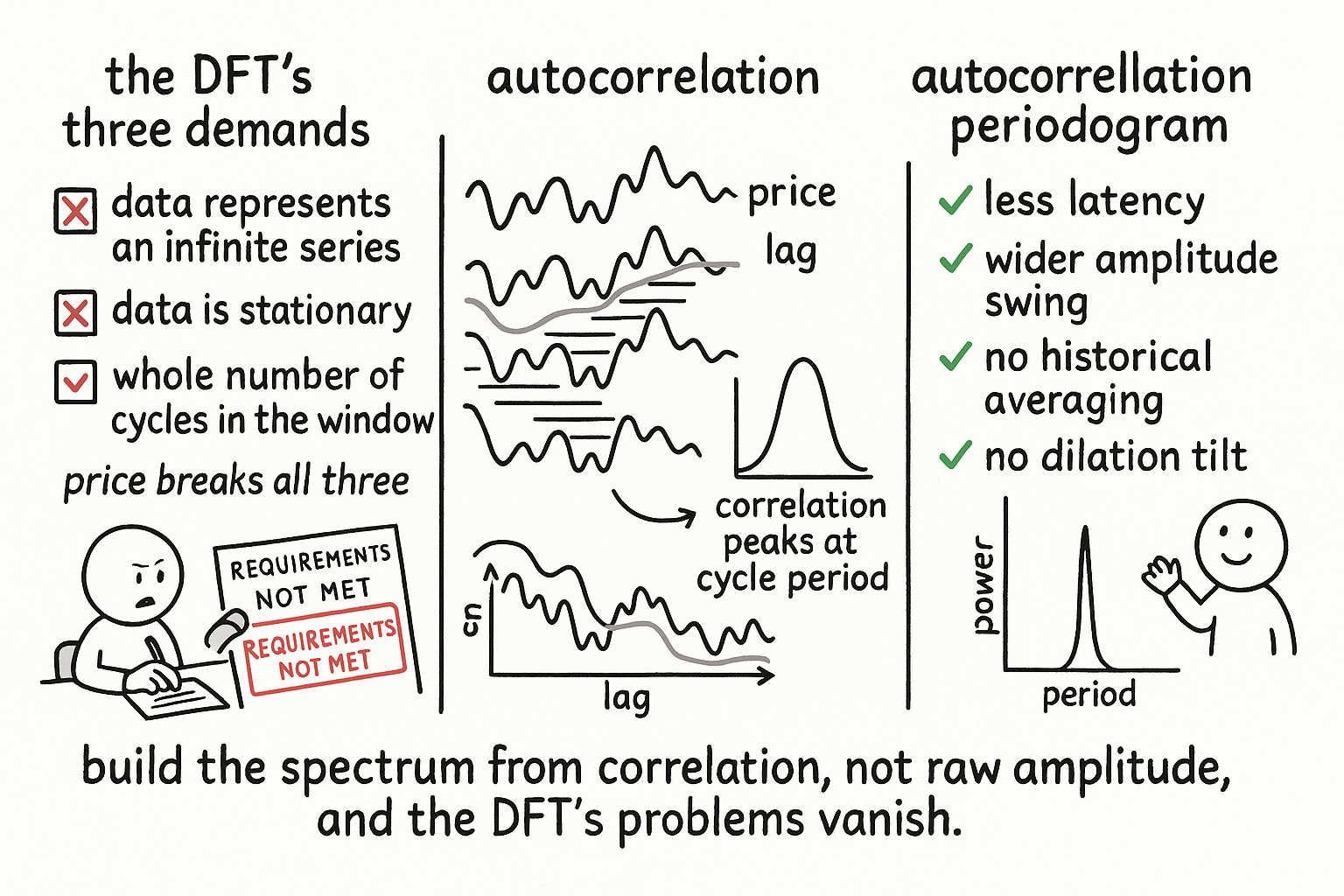

The Fourier transform demands an infinite, stationary, whole-cycle window that price never provides. The autocorrelation periodogram builds the spectrum from correlation instead, with less lag and no amplitude tilt.

The old article "Dominant Cycle Estimation Without Astrology" laid out four ways to measure the dominant cycle and named one the production default: the autocorrelation periodogram, lowest variance, fine resolution, robust. This article is the why. The Fourier transform is the textbook tool for measuring frequency, but applied to price it carries three assumptions price refuses to satisfy, and the autocorrelation periodogram is the workaround that quietly fixes all three at once.

What the Fourier transform demands and price denies

The discrete Fourier transform is nearly synonymous with frequency measurement, and it rests on three requirements. The data window must be representative of an infinitely long series, the data must be stationary, and only a whole number of cycles can sit in the window or the edges smear the estimate. Price violates each one. A 60-bar window is not a sample of some eternal stationary process; it is a slice of a market whose statistics drift bar to bar, and the dominant cycle inside it is rarely an exact integer divisor of the window length. The old article "Why Market Cycles Are Evanescent" made the structural version of this point: cycles come and go and change period, so a tool that assumes a stable, infinitely repeating cycle is mismatched to the substrate.

The standard patch is a moving DFT. Instead of one transform over all history, compute a block DFT over a sliding window and repeat it every bar, and dodge the integer-cycle problem by computing in terms of cycle period rather than frequency intervals. A useful trick on its own, the moving DFT, but it still inherits the spectral dilation from the previous article and still needs historical averaging to stabilize, both of which add latency.

Autocorrelation builds the spectrum without the raw amplitude

The autocorrelation periodogram takes a different route to the same destination. Start from autocorrelation: correlate the price series with a lagged copy of itself. At lag zero the correlation is perfect; lag it by one bar and the correlation drops; keep lagging and the correlation rises and falls in step with whatever cycle the data carries.

$$ \text{AutoCorr}(\text{Lag}) \;=\; C \cdot \text{Lag}^{-\alpha} \quad \text{(efficient-market, long-memory case)} $$

For a pure long-memory random series the autocorrelation decays as a clean power law of the lag, the same alpha exponent from the old noise-color article. Real market data refuse to follow that power law, and the deviation is the point: the partial correlation structure that does not fit the efficient-market decay is exactly the cyclic information you want to extract. The autocorrelation periodogram computes the autocorrelation across a span of lags, then for each candidate cycle period measures how strongly the autocorrelation profile resonates at that period, and the period with the strongest resonance is the dominant cycle.

Why it beats the DFT and the comb filter

The advantage is that working from correlation rather than raw amplitude dissolves the problems that plagued the other methods.

$$ \text{less latency} \;+\; \text{wider amplitude swing} \;+\; \text{no historical averaging} \;+\; \text{no dilation compensation} $$

Less latency, because it does not need a long averaging window to stabilize. A wider range of amplitude swings, so the dominant cycle stands out sharply instead of blurring into its neighbors. No historical averaging, so the estimate reacts when the cycle shifts. And no spectral dilation compensation, because correlation is already normalized, so the amplitude tilt from the previous article never appears and there is nothing to undo. Set against the comb-filter approach, a bank of band-pass filters each tuned to a different period with the output amplitudes read as the spectrum, the autocorrelation periodogram wins on every count: the comb filter has more latency, narrower amplitude swings, and needs the dilation correction the autocorrelation method renders unnecessary. That combination is why the old dominant-cycle article ranked it the production default at roughly 12-bar lag with the lowest variance of the four methods.

Keep the honest boundary in view. The autocorrelation periodogram measures the dominant cycle of the recent window cleanly, but it is still a measurement, not a prediction; the evanescent-cycles warning stands, and the number it reports can drift or vanish out of sample. It also still requires a window long enough to contain a few repetitions of the cycle you are chasing, so it is fast relative to the DFT, not instantaneous. Use it as the front end that feeds adaptive indicators their lookback, gate cycle-mode strategies on the sharpness of its peak, and treat a flat, peakless periodogram as the market telling you there is no cycle to trade right now.

KEY POINTS

- The DFT is the standard frequency tool but demands a representative infinite series, stationarity, and a whole number of cycles in the window; price violates all three, echoing the old article "Why Market Cycles Are Evanescent."

- The usual patch is a moving DFT computed every bar in terms of cycle period, but it inherits spectral dilation and needs historical averaging, both of which add latency.

- The autocorrelation periodogram works from autocorrelation: correlate price with lagged copies of itself, find which cycle period the correlation profile resonates at, and call that the dominant cycle.

- A pure long-memory series gives autocorrelation that decays as a power law of lag; real markets deviate from it, and that deviation is the cyclic information worth extracting.

- Because it works from normalized correlation rather than raw amplitude, it has less latency, wider amplitude swings, no need for historical averaging, and no spectral-dilation compensation, beating both the DFT and the comb filter.

- It is still a measurement, not a forecast, and needs a window holding a few cycle repetitions; use it to feed adaptive lookbacks and gate cycle-mode strategies, treating a flat periodogram as no tradeable cycle.