2.47 Critical Period and the Half-Power Point: How to Pick Filter Length

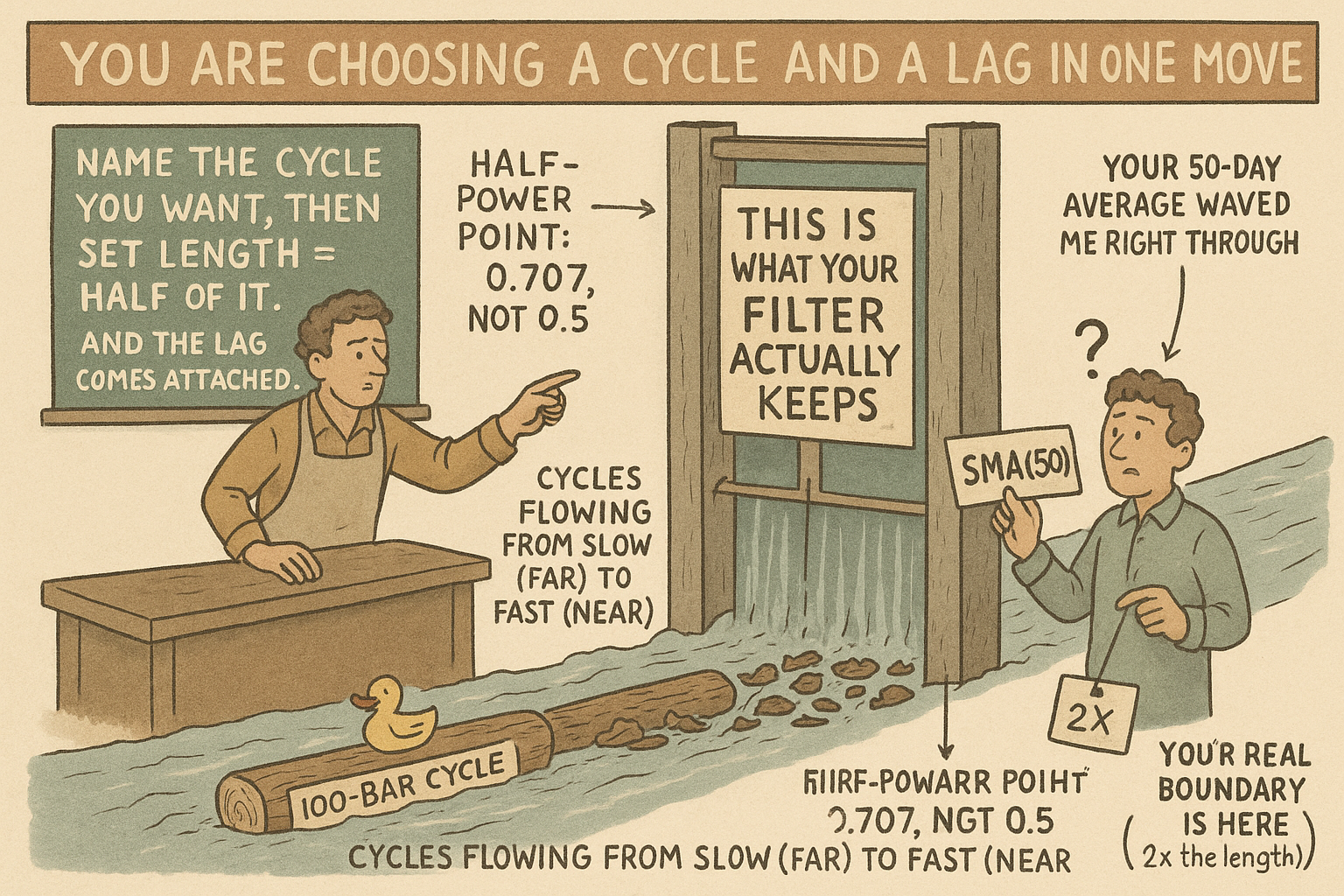

A filter's critical period is its half-power point: amplitude 0.707, not 0.5. For an SMA it's twice the length, so SMA(50) targets a 100-bar cycle. Pick length on purpose; the lag comes attached.

The old article "How to Think About Indicator Lag Before Backtesting" demanded you compute an indicator's lag before you trust it, and the old article "The Hidden Cost of Every Moving Average: Lag" priced that lag in money and missed entries. Both leave a question dangling: when you set a filter's length, what cycle are you actually choosing to keep? Most traders answer wrong. They think an SMA of length 50 filters out the 50-bar cycle. It does not. The honest answer comes from one number, the critical period, defined at the half-power point, and once you can compute it you set filter length on purpose instead of by superstition.

Half-power means amplitude 0.707, not 0.5

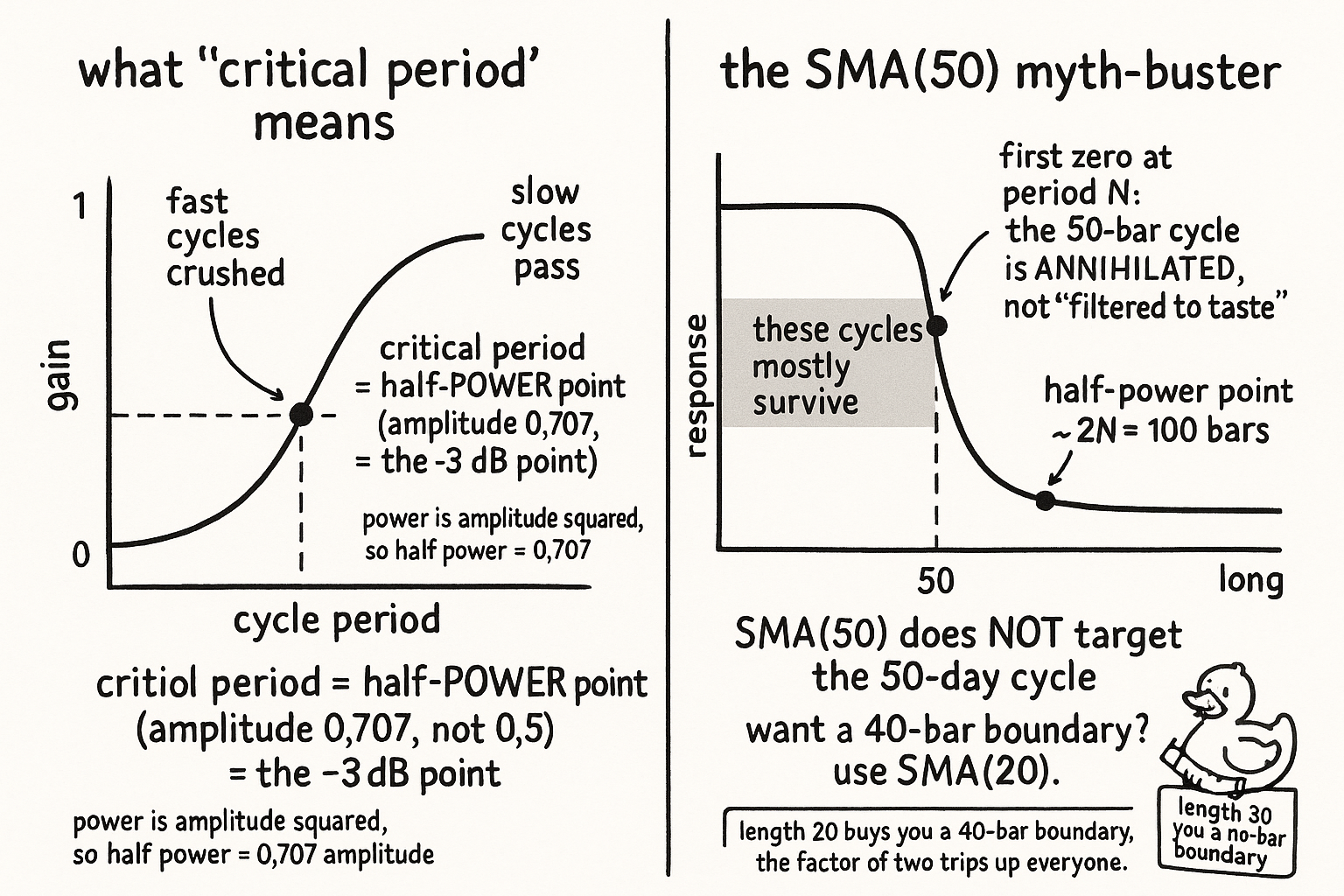

The critical period is the cycle length at which the filter's output power is half the input power at that frequency. The word power is doing real work here. Power is proportional to the square of amplitude, so cutting power in half does not mean cutting amplitude in half.

$$ \frac{\text{output power}}{\text{input power}} = \frac{1}{2} \;\Longrightarrow\; \frac{\text{output amplitude}}{\text{input amplitude}} = \frac{1}{\sqrt{2}} \approx 0.707 $$

So at the critical period the wave comes out at about 70.7 percent of the size it went in, not 50 percent. This is the same point engineers call the minus-three-decibel point, and it is the universal convention for where a filter's passband ends and its stopband begins. The dividing line is not where the filter kills a cycle; it is where the filter has taken the first real bite out of it, halving its power. Everything slower than the critical period passes mostly intact; everything faster gets progressively crushed.

For an SMA, the critical period is twice the length

Now the number that corrects the common error. For a simple moving average, the critical period is about twice the filter length.

$$ T_{\text{critical}} \approx 2N \quad \text{(for an SMA of length } N\text{)} $$

An SMA of length 50 has its half-power point at a cycle of roughly 100 bars. It only takes the first real bite out of the 100-bar cycle, and it barely touches the 50-bar cycle a trader assumes it targets. Worse, the old article "Why the SMA Is Often a Terrible Smoother" showed the SMA's first response zero sits at the period equal to its length, so the SMA(50) annihilates the 50-bar cycle outright while leaving everything between 50 and 100 bars mostly alive. The "50-day average" is neither a clean filter at 50 days nor at any single period; its honest single-number summary is the half-power point near 100 bars. If you want the boundary between trend and cycle to sit at a 40-bar period, you do not use an SMA(40), you use an SMA(20), because the critical period is twice the length.

Picking length is picking lag, so pick both at once

This is the practical procedure the lag articles were building toward. Decide the cycle period you want at the pass-stop boundary, then back out the length: for an SMA, length equals half the critical period. That single decision is honest in a way that "I use a 50-day average because everyone does" is not, because it ties the filter to a cycle you can name.

But the same choice sets your lag, and you do not get to choose them independently. A longer critical period means more smoothing, which means more bars averaged, which means more lag, the structural delay from the old article "The Hidden Cost of Every Moving Average: Lag." So setting the critical period is setting the lag budget the old article "How to Think About Indicator Lag Before Backtesting" told you to compute, in the same motion. Push the critical period out to keep slower cycles and you pay with more lag; pull it in for responsiveness and you let more cycle and noise through. There is no length that escapes the trade. The discipline: name the boundary cycle you want, convert it to a length, read off the lag that length forces, and check that lag against your holding period before you run anything. If the half-power point you need carries more lag than your strategy can absorb, the SMA is the wrong tool and you reach for a sharper filter, not a different length.

KEY POINTS

- The critical period is the cycle length where the filter's output power is half the input power. Because power is amplitude squared, half power means amplitude 0.707, not 0.5, the same as the engineer's minus-three-decibel point.

- The critical period is the honest single-number summary of what a filter targets: the boundary where it takes the first real bite, with slower cycles mostly passing and faster ones progressively crushed.

- For an SMA the critical period is about twice the length. So SMA(50)'s half-power point is near a 100-bar cycle, and it does not target the 50-day cycle traders assume.

- The SMA's first response zero sits at the period equal to its length, so SMA(50) annihilates the 50-bar cycle outright (the old article "Why the SMA Is Often a Terrible Smoother") while cycles between 50 and 100 bars mostly survive.

- To set length on purpose: name the boundary cycle you want, then use length equals half the critical period for an SMA, instead of copying a default.

- Critical period and lag are one choice, not two: a longer critical period means more smoothing means more lag. Read off the lag the length forces and check it against your holding period before trading, per the old article "How to Think About Indicator Lag Before Backtesting."

References

- Statistically Sound Indicators for Financial Market Prediction - Timothy Masters (Amazon)

- Cycle Analytics for Traders - John Ehlers (Amazon)

- Cutoff frequency and the half-power (-3 dB) point (Wikipedia)

- Decibel and power vs amplitude ratios (Wikipedia)

- The Scientist and Engineer's Guide to Digital Signal Processing: Moving Average Filters

- Bandwidth and the half-power bandwidth definition (Wikipedia)