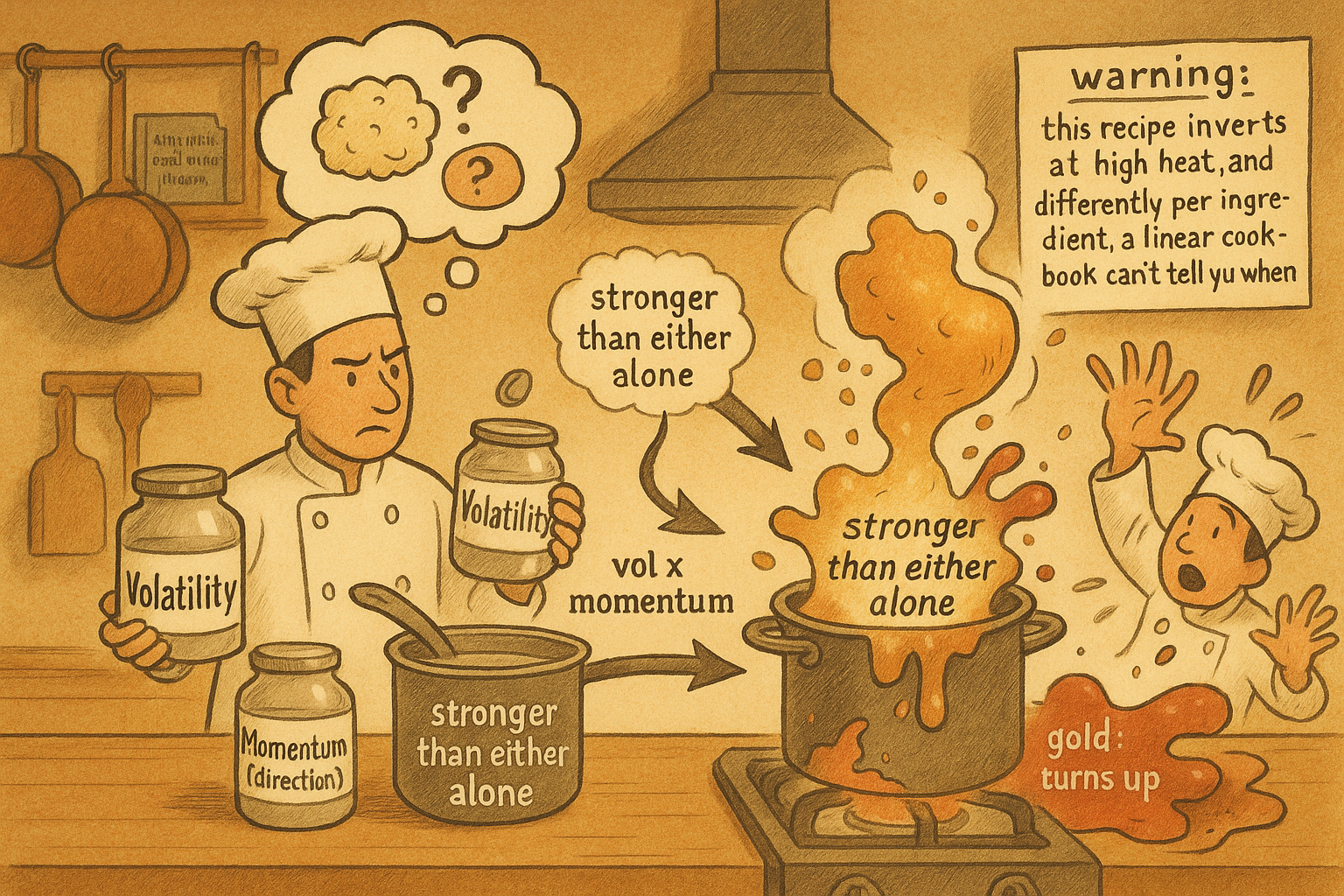

5.43 Predictive but Uncorrelated: Alphas That Only Work as Interactions

Volatility predicts the size of a move, not its direction, so it can't trade alone. Multiply it by momentum and it works, until extreme vol gains its own sign, down for equities and up for gold.

Here is a feature that knows the future and cannot trade. Volatility. When volatility moves from low to medium, the size of the next price move tends to go up. You have genuine information: the move is coming. You still have no idea which way. The correlation between volatility and the signed future return is about zero, so a model that takes volatility as a standalone input does nothing with it. The information is real and the regression coefficient is zero, and both statements are true at once.

This trap catches a lot of careful people. You find a feature with obvious predictive content, drop it into a linear model expecting it to lift the fit, and watch it contribute nothing. The feature predicts the magnitude of the move, written as the absolute future return, not its sign. A linear model fits signed returns. The two never meet.

$$ \text{corr}\big(\text{vol},\; r_{t+1}\big) \approx 0 \qquad\text{while}\qquad \text{corr}\big(\text{vol},\; \lvert r_{t+1}\rvert\big) > 0 $$

Read it as two separate facts. The left correlation, volatility against the signed next return, sits near zero, which is why volatility alone earns no weight in a model of direction. The right correlation, volatility against the absolute next return, is positive, which is the predictive content you can see but cannot directly monetize. A directional model only ever consumes the left one.