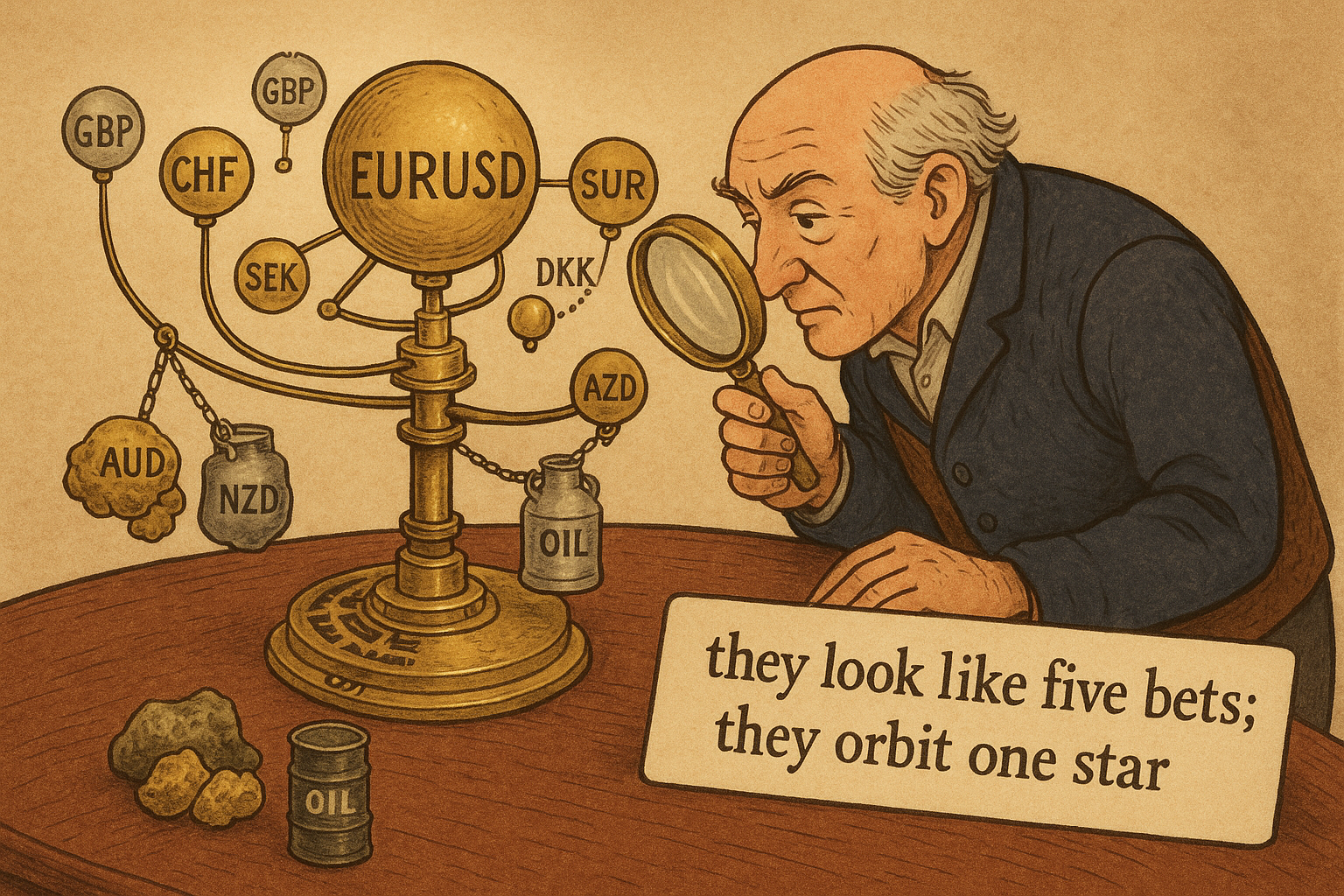

4.57 Currency Personality and Correlation Blocs

Currencies cluster into blocs by their drivers: a European cluster anchored to EURUSD, a commodity cluster wired to specific exports, and a yield axis splitting havens from risk currencies. Trade several members of one bloc and you load one factor, not five bets.

A trader builds what looks like a diversified short-euro book: short EURUSD, short USDSEK turned into a euro short, a position in the Norwegian krone, a little Swiss franc. Five tickets, one view. When EURUSD moves, all five move together, because the Swedish krona, the Norwegian krone, the Danish krone, and the Swiss franc are not independent currencies in any tradeable sense; they are satellites whose dollar exchange rate is mostly set by EURUSD. The trader thought the book held five bets. It held one bet wearing five tickets, sized as if it were five, which means it carried roughly the risk of a single position five times too large.

Currencies have personalities, and currencies with similar personalities correlate hard enough that treating them as separate names is a sizing error. The personalities are not folklore. They come from what actually drives each currency: a shared regional anchor, an exported commodity, a yield level that makes the currency a haven or a risk asset. Group the currencies by driver and you get a small number of blocs, and inside a bloc the correlation is high enough that the bloc, not the individual currency, is the real unit of risk. This article maps the blocs, explains the driver behind each, and shows why the bloc structure has to enter the risk model before a currency book can call itself diversified.

The European bloc

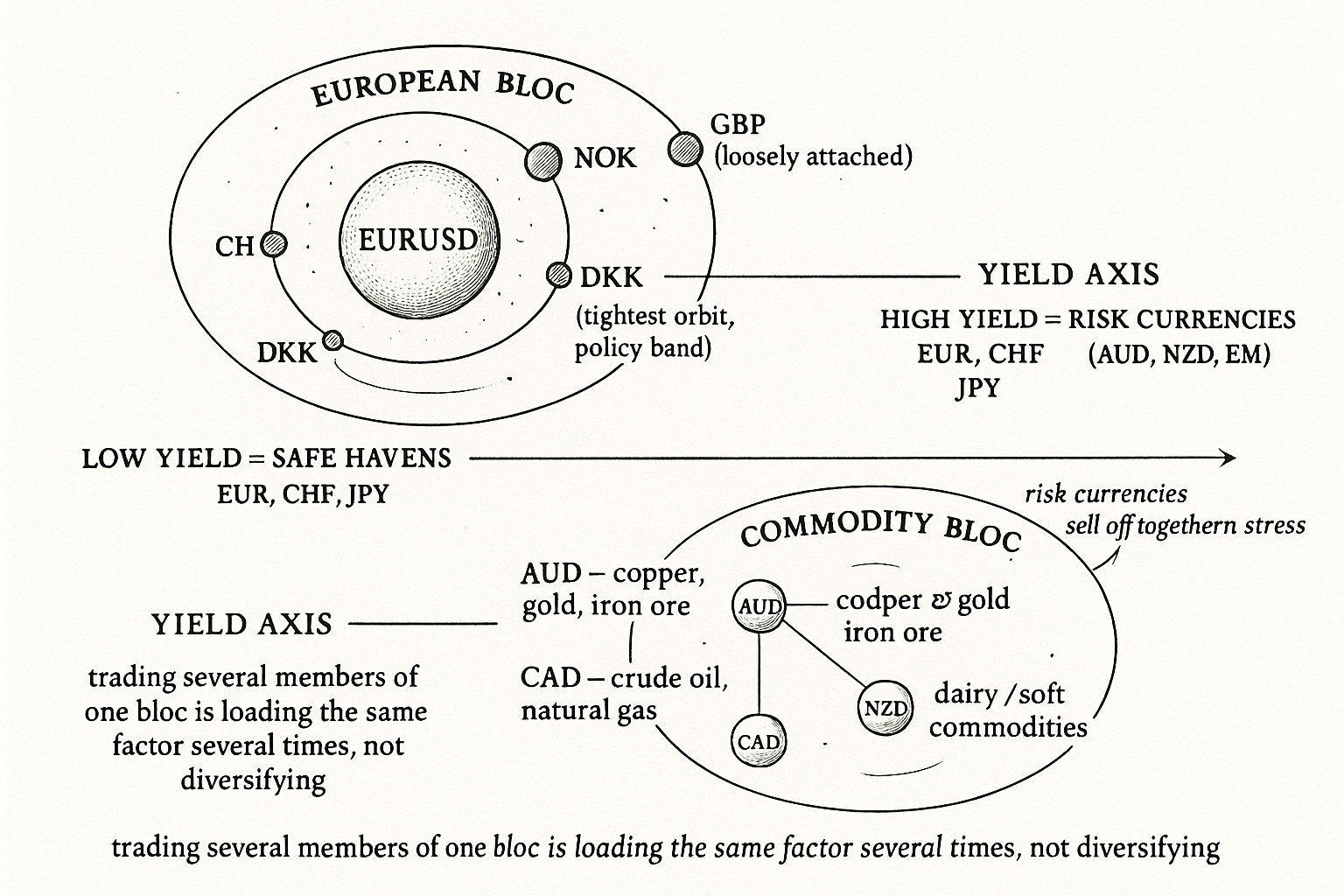

The cleanest bloc is European. The euro, the Swiss franc, the Swedish krona, the Norwegian krone, and the Danish krone trade as a cluster, and their exchange rate against the dollar is mostly determined by EURUSD. Geography and trade integration tie these economies to the euro area, so when EURUSD moves on a dollar story or a euro story, the satellites follow. The Danish krone is the extreme case, held in a tight band against the euro by policy, so DKKUSD is almost a scaled copy of EURUSD. The frank and the Scandinavian currencies have more of their own personality but still take their primary cue from the euro.

The British pound sits at the edge of this bloc. It gets lumped into the European basket because of trade and proximity, but its links are looser than the others, and it carries enough of its own domestic story that treating it as a pure euro satellite is wrong. Sterling is in the room, not in the cluster.

The systematic point: a position in two or more European-bloc currencies against the dollar is mostly the same EURUSD bet repeated. Decompose the pairs into per-currency strength and the redundancy is obvious, the matrix view from the old article "Currency Strength Models from Pair Decomposition." The bloc is what the strength model recovers as a shared factor, and trading several members of it is loading that one factor several times.

The commodity bloc

The second bloc is the commodity currencies: the Australian dollar, the New Zealand dollar, and the Canadian dollar among the majors, with the Brazilian real, the South African rand, and the Chilean peso extending the idea into emerging markets. These come from commodity-exporting economies, and their currencies move with the prices of what they sell. The links are specific, not generic:

- The Australian dollar tracks copper, gold, and iron ore.

- The Canadian dollar tracks crude oil and natural gas.

- The New Zealand dollar tracks soft commodities, dairy above all.

This is the per-currency driver map from the old article "Why FX Traders Must Watch Gold, Rates, and Equities" read from the currency's side: the right external market for the Canadian dollar is crude, and watching gold for the Canadian dollar adds noise where watching crude adds signal. The commodity link is also why these currencies do not move as one bloc as tightly as the European cluster does. The Australian dollar and the Canadian dollar share the "commodity exporter, risk-sensitive" personality, but iron ore and crude can diverge, so the intra-bloc correlation is real but looser than the EURUSD-anchored cluster.

The yield personality: havens and risk currencies

Cutting across the regional and commodity blocs is a yield axis that sets risk-on and risk-off behavior. Low-yielding currencies behave as safe havens. In recent cycles the euro, the franc, and the yen have carried the lowest yields, and they strengthen when markets are frightened because they are the funding currencies traders buy back when they cut risk. High-yielding currencies, the Australian and New Zealand dollars among the majors and the emerging-market currencies beyond them, are the risk currencies; they pay you to hold them in calm times and sell off hard during stress.

This yield personality is what makes the commodity bloc and the risk axis overlap. The same Australian dollar that tracks iron ore is also a high-yielder that dumps in a panic, so it carries two correlated reasons to fall together with other risk assets when fear hits. That overlap is the carry behavior worked separately in the article on the carry trade, and it is the reason a "diversified" basket of high-yielders is really one concentrated risk-appetite bet, the correlation-to-one problem the macro article flagged for 2008.

Why the bloc structure has to enter the risk model

Treating correlated currencies as independent names breaks the sizing arithmetic. The risk of a basket is not the sum of the individual risks; it depends on the correlations, and inside a bloc those correlations are high.

$$ \sigma_{\text{book}}^2 = \sum_{i} w_i^2 \sigma_i^2 \;+\; \sum_{i \neq j} w_i w_j \,\rho_{ij}\, \sigma_i \sigma_j $$

The variance of the book is the sum of each position's own variance (the first term) plus a cross term for every pair of positions, scaled by their correlation. When the correlations between members of a bloc are near one, the cross terms are almost as large as the variance terms, and a five-position European book has a variance close to that of one position five times the size. The naive calculation, which assumes the correlations are zero and keeps only the first term, reports a fifth of the true risk. The book is concentrated and the risk number says it is diversified.

The fix is to size at the bloc level. Estimate the correlation structure, recognize that several European-bloc shorts are one factor exposure, and budget risk to the factor rather than to the ticket count. This is the same currency-strength decomposition turned into a risk control: solve for the shared drivers, size against the drivers, and stop counting correlated tickets as independent bets. The honest caveat is that the correlations are not stable; the European bloc holds tighter than the commodity bloc, and every bloc tightens toward one in a crisis, so the structure you measured in calm markets understates the concentration in the panic where it matters most.

Visualizing the blocs

KEY POINTS

- Currencies have personalities set by their drivers, and currencies with similar drivers correlate hard enough that the bloc, not the individual currency, is the real unit of risk.

- The European bloc (euro, franc, Swedish krona, Norwegian krone, Danish krone) takes its dollar exchange rate mostly from EURUSD. The Danish krone is held in a band and is almost a scaled EURUSD; sterling is loosely attached, not in the cluster.

- The commodity bloc tracks specific exports: the Australian dollar on copper, gold, and iron ore; the Canadian dollar on crude and natural gas; the New Zealand dollar on dairy. Watch the right commodity per currency, not a generic one.

- A yield axis cuts across both blocs. Low-yielders (euro, franc, yen) act as safe havens and strengthen in fear; high-yielders (Australian, New Zealand, emerging-market currencies) are risk currencies that sell off in stress.

- The commodity and yield personalities overlap: the Australian dollar is both an iron-ore proxy and a high-yielder, so it carries two correlated reasons to fall together with risk assets in a panic.

- Correlated currencies break the sizing arithmetic. Book variance includes cross terms scaled by correlation; when intra-bloc correlation is near one, a five-position bloc book carries the risk of one position five times the size while a naive calculation reports a fifth of it.

- Size at the bloc level using a currency-strength decomposition, budget risk to the shared factor, and remember the correlations tighten toward one in a crisis, so the calm-market structure understates the concentration when it matters.

References

- Trading Systems and Methods - Perry Kaufman (Amazon)

- Cybernetic Trading Strategies - Murray Ruggiero (Amazon)

- The Art of Currency Trading - Brent Donnelly (Amazon)

- The Global Factor Structure of Exchange Rates

- Currency Factors

- Common Factors in Currency Characteristics

- The Relationship between Commodity Prices and Currency Exchange Rates

- A global perspective on exchange rate dynamics via currency factors

- Systematic exchange rate variation: Where does the dollar factor come from?

- Systematic variations in exchange rate returns

- Currency co-movement and network correlation structure of foreign exchange markets

- International correlation risk

- Exchange rate anchoring – Is there still a de facto US dollar standard?

- European Financial Markets After EMU: A First Assessment