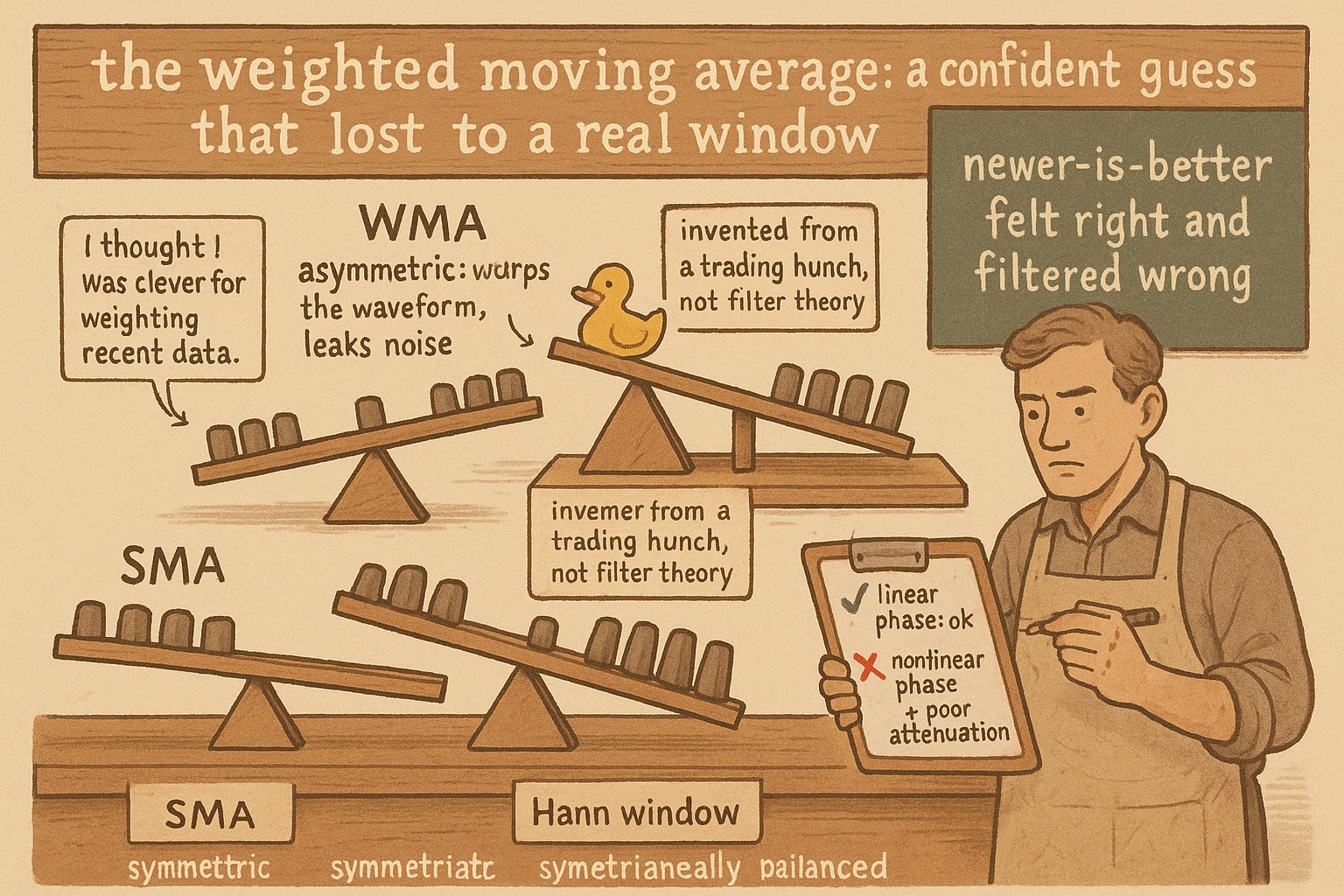

2.48 The Weighted Moving Average Was a Mistake

The WMA ramps weights toward recent bars, so its coefficients are asymmetric, breaking linear phase and warping shape. It lags more than the SMA at equal noise rejection; a real window beats both.

The old article "Why the SMA Is Often a Terrible Smoother" showed the simple moving average leaks noise through its sidelobes, and the old article "EMA vs SMA: Why Simplicity Still Matters" defended the EMA for its recursive efficiency. The weighted moving average sits between them in popularity and below both in merit. It weights recent bars more and older bars less, in a straight linear ramp, on the theory that newer data deserves more say. That theory came from someone reasoning about trading, not about filters, and the filter view shows the WMA loses on the axes that matter. It is a window function chosen by intuition, and intuition picked a bad window.

What the WMA is, structurally

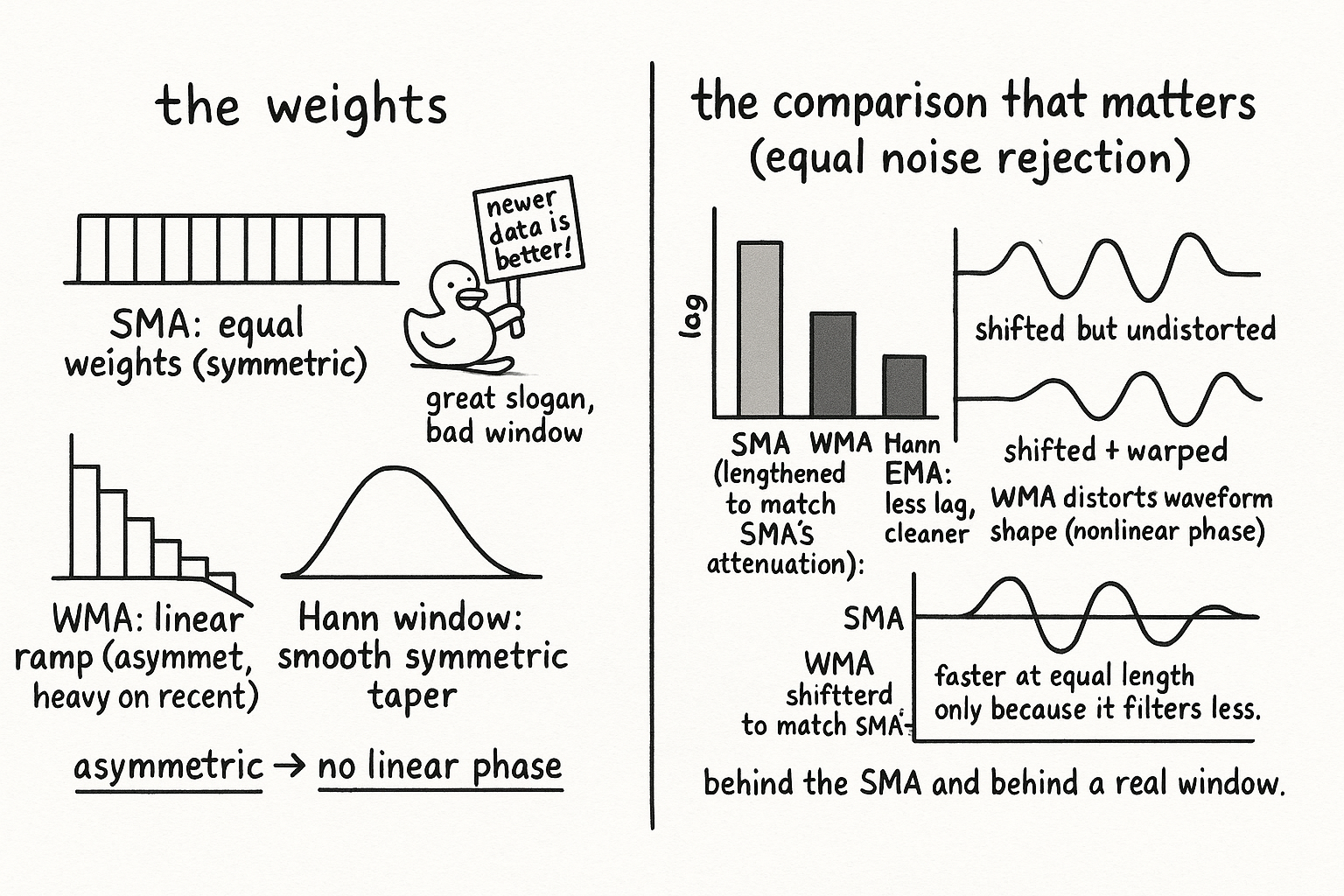

The WMA is a non-recursive filter, a finite impulse response, like the SMA. The difference is the shape of its weights. The SMA weights every bar in the window equally; the WMA ramps the weights down linearly from the most recent bar to the oldest, so the newest close gets the largest coefficient and the weight decays to near zero at the far end of the window. The coefficients are asymmetric about the center of the window, heavy on the recent side and light on the old side. That asymmetry is the whole story, because two of a filter's most important properties depend on whether its coefficients are symmetric, and the WMA throws symmetry away.

Asymmetry breaks linear phase

The old article "Recursive vs Non-Recursive: The Two Families of Every Indicator" stated the rule: a non-recursive filter whose coefficients are symmetric about the center has a lag equal to its degree over two, and that lag is the same at every frequency. Constant lag across frequency is linear phase, and it is precious, because it means the filter delays every cycle by the same number of bars and does not distort the shape of a waveform passing through. The SMA has it. The WMA does not.

Because the WMA's coefficients are asymmetric, its phase response is nonlinear: different cycles get delayed by different amounts. A slow swing and a fast wiggle come out shifted by unequal lags, so the filter does not just delay the waveform, it warps its shape. Peaks and troughs land in the wrong relative positions. This is the same defect that makes recursive filters tricky, except the WMA pays it without buying the recursive family's efficiency, since it still needs all N taps. You get phase distortion and you still store the whole window.

It loses the comparison that matters

The WMA's marketing rests on lag. At equal length it does react faster than the SMA, its weight sits closer to the present, so the naive comparison favors it. But equal length is the wrong comparison. The honest comparison holds noise rejection constant and asks which filter lags less while attenuating the same amount of high-frequency junk, and there the WMA falls apart. Its stopband attenuation is poor, worse than the SMA's, so to match the SMA's actual noise rejection you must lengthen the WMA, and the lengthened WMA lags more than the SMA you were comparing against. The faster response was bought by doing less filtering, which is not a free lunch, it is no lunch.

Set the WMA against a properly designed window and the verdict gets blunter. A tapered window like the Hann or Blackman, covered in the old article "Why the SMA Is Often a Terrible Smoother," gives an order of magnitude better stopband attenuation at the same lag as the SMA, and it keeps symmetric coefficients, so it preserves linear phase. The WMA delivers worse attenuation than the SMA and worse phase behavior than a tapered window, landing behind both on the two axes that decide a smoother's quality. The linear ramp was a guess at what good weighting looks like, and it guessed wrong: real window design tapers smoothly toward zero at both ends, symmetrically, which is precisely what the WMA's one-sided ramp refuses to do. The practical conclusion is unsentimental. If you want lower lag than the SMA, use an EMA for its recursive cheapness or a tapered window for its clean stopband, both of which beat the WMA. The WMA survives on familiarity and a plausible-sounding story, not on performance, and there is no filtering job where it is the right answer.

KEY POINTS

- The WMA is a non-recursive (FIR) filter like the SMA, but it ramps weights down linearly from the newest bar to the oldest, so its coefficients are asymmetric about the center.

- Asymmetric coefficients break linear phase. By the rule from the old article "Recursive vs Non-Recursive: The Two Families of Every Indicator," only symmetric FIR filters have constant lag across frequency.

- Nonlinear phase means different cycles are delayed by different amounts, so the WMA warps waveform shape, not just delays it, putting peaks and troughs in the wrong relative places.

- At equal length the WMA reacts faster than the SMA, but that is the wrong comparison. Its stopband attenuation is worse, so to match the SMA's noise rejection you must lengthen it, and then it lags more.

- Against a tapered window (Hann, Blackman) from the old article "Why the SMA Is Often a Terrible Smoother," the WMA loses twice: worse attenuation than the SMA and worse phase than the symmetric window.

- For lower lag than the SMA, use an EMA (recursive, cheap) or a tapered window (clean stopband, linear phase). The WMA is the right answer to no filtering job.

References

- Statistically Sound Indicators for Financial Market Prediction - Timothy Masters (Amazon)

- Cycle Analytics for Traders - John Ehlers (Amazon)

- Moving average: simple, weighted, and exponential (Wikipedia)

- Window function: tapered windows and stopband attenuation (Wikipedia)

- Linear phase and why symmetric FIR coefficients matter (Wikipedia)

- The Scientist and Engineer's Guide to Digital Signal Processing: Windowed-Sinc Filters