6.2 Ranked Long/Short Systems Explained

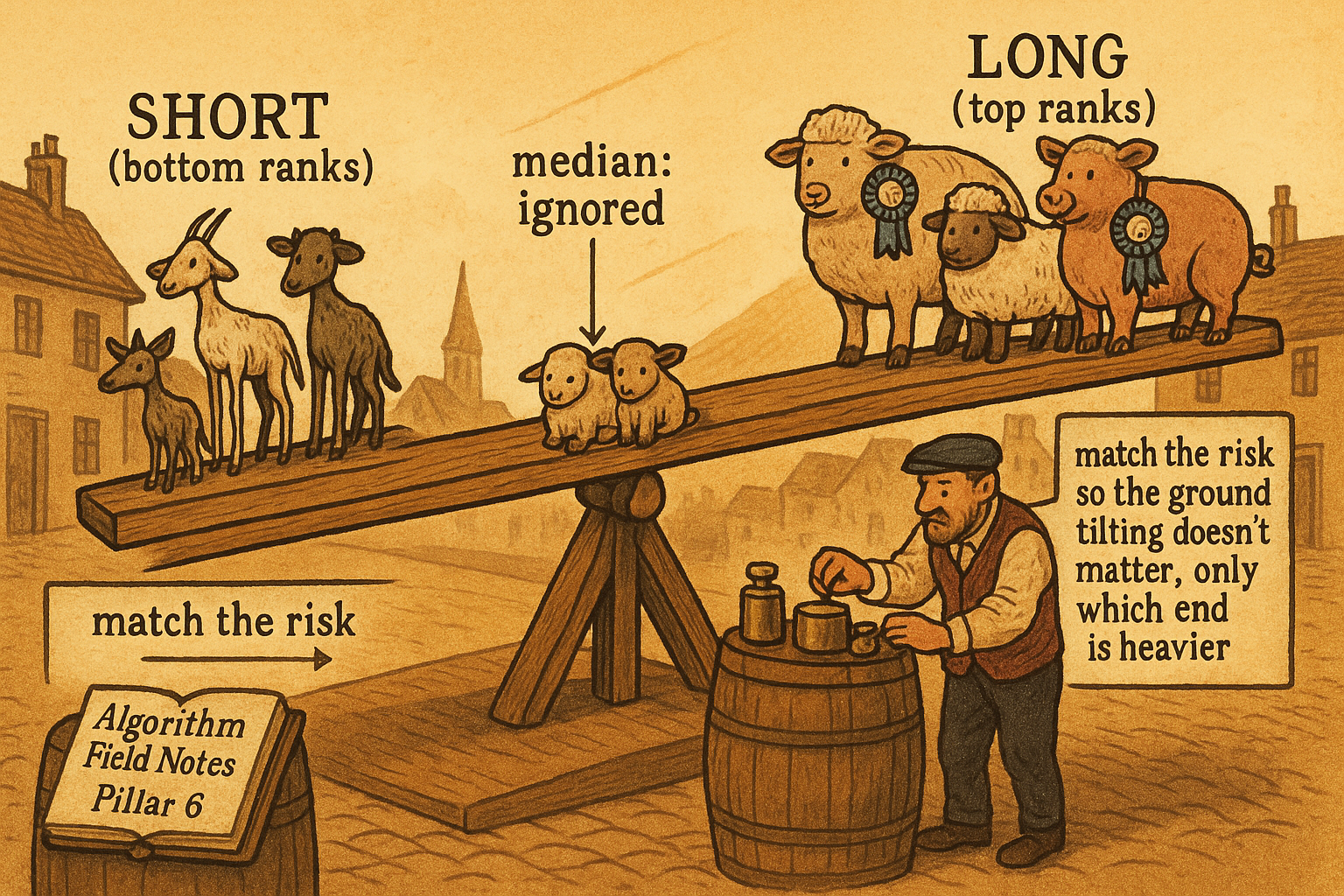

Score the universe, sort it, buy the top slice and short the bottom in equal risk. The broad market cancels and you hold only the spread between winners and losers.

Take a basket of instruments, score each one with a signal, sort them, buy the top slice and short the bottom slice in equal risk. That sentence is the entire architecture of a ranked long/short system, and once you internalize it you stop thinking about individual trades and start thinking about a portfolio that rebalances itself every period. "Ranking Beats Forecasting for Many Trading Problems" argued why the ordering is the robust thing to trade; this is how you turn the ordering into actual positions.

The mechanism: sort, slice, offset

You run one number per instrument, the score, whatever your signal produces, a momentum reading, a carry, a mean-reversion z-score. Sort the universe by that score. The instruments at the top are the ones the signal likes most, the bottom are the ones it likes least. Go long a slice of the top, say the top fifth or top third, and short the matching slice at the bottom. Size the long book and the short book to carry the same risk, so the position is a bet on the spread between the winners and losers, not on the market itself.

That equal-and-offsetting construction is what makes the system market-neutral by design. When the whole universe rallies, your longs and shorts both move and the broad move cancels. What survives is the differential: did the instruments you ranked high outperform the ones you ranked low? The market direction, the thing you have no edge predicting, gets subtracted out, and you are left holding only the part you actually have a view on.

Why the spread, not the level

A ranked book is structurally a relative bet, and that is its strength and its limit at once. The strength: you are immunized against the factor you cannot forecast. You never have to be right about whether commodities go up or down this month; you only have to be right that your top names beat your bottom names. The limit: if your whole universe is junk, ranking the junk still leaves you holding junk on both sides, and the spread can stay flat or bleed costs while you wait for a differential that never shows up.

$$ w_i = \frac{r_i - \bar{r}}{\sum_{j} |r_j - \bar{r}|} $$

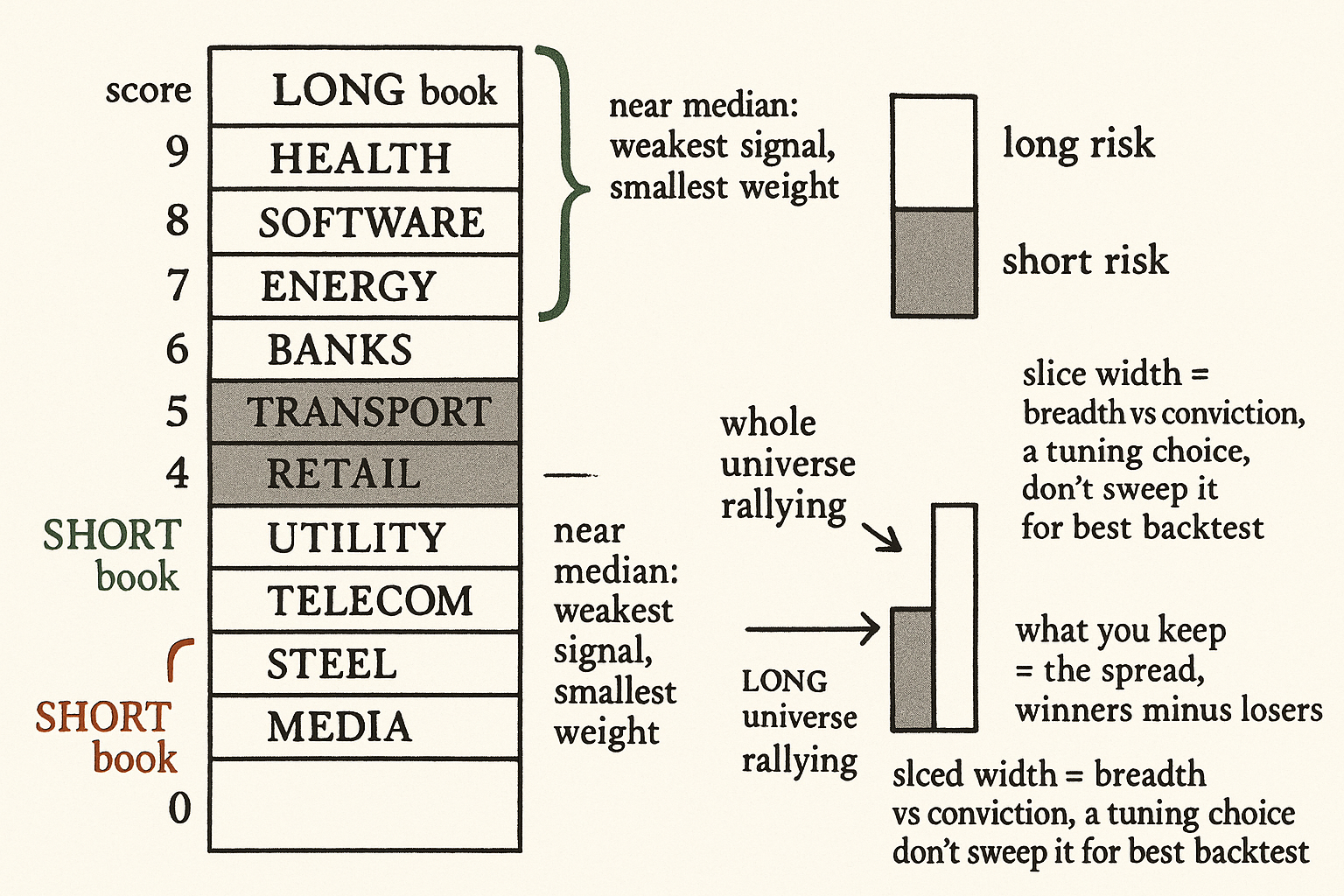

One clean way to turn ranks into weights: center the ranks and normalize. Each instrument's rank, compared against the average rank, gives a centered value, and the denominator sums the absolute deviations so the weights add to a fixed gross exposure. Instruments above the median rank get positive weights (longs), those below get negative (shorts), and the size scales with how far from the middle they sit. The top-ranked and bottom-ranked names carry the biggest weights; the ones near the median carry almost nothing, which is correct, because the middle of a ranking is where the signal is weakest and least worth betting on.

The slice width is a real decision

How wide you cut the slices trades breadth against conviction. Top-and-bottom fifths give you a sharp, concentrated bet on the extremes where the signal is strongest, and more turnover and more idiosyncratic risk per name. Top-and-bottom halves spread the bet across the whole universe, diluting conviction but smoothing the ride and lowering turnover. Neither is right in the abstract. A noisy signal where only the extremes carry information wants narrow slices; a broad, gentle signal that orders the whole universe meaningfully wants wide ones. This is a tuning choice, and like every tuning choice it is a place to overfit, so you decide it on the logic of the signal, not by sweeping it for the best backtest.

Visualizing the ranked book

KEY POINTS

- A ranked long/short system scores each instrument, sorts the universe, and goes long the top slice while shorting the bottom slice in matched risk. The position is a bet on the spread between winners and losers.

- Matching long and short risk makes the system market-neutral by construction. The broad move cancels, and what survives is the differential between the high-ranked and low-ranked names.

- The strength is immunity to the factor you cannot forecast; you never bet on market direction. The limit is that ranking a junk universe leaves you holding junk on both sides while costs bleed.

- Turn ranks into weights by centering and normalizing, so weight scales with distance from the median. Extreme names carry the most; names near the middle carry almost nothing, which is correct because the signal is weakest there.

- Slice width trades breadth against conviction. Narrow extremes suit a noisy signal that only informs at the tails; wide slices suit a gentle signal that orders the whole universe.

- Slice width is a tuning choice and a place to overfit. Decide it from the logic of the signal, not by sweeping for the best backtest.

References

- Systematic Trading - Robert Carver (Amazon)

- Trading Systems - Urban Jaekle Emilio Tomasini (Amazon)

- Building Cross-Sectional Systematic Strategies by Learning to Rank

- Optimal Characteristic Portfolios

- TrendFolios®: A Portfolio Construction Framework for Utilizing Momentum and Trend-Following Signals Across Multiple Asset Classes

- The Impact of Volatility Targeting

- Measuring Strategy-Decay Risk: Minimum Regime Performance and Other Tail-Risk Metrics for Quantitative Strategies

- Dynamic Inclusion and Bounded Multi-Factor Tilts for Robust Portfolio Construction

- A Market-State Momentum Signal that Reverses Roles for Robust Performance Over Momentum Crashes

- Pairwise Dissimilarity and Risk-Seeking Portfolio Construction

- LambdaRankIC: Directly Optimizing Rank IC for Financial Prediction

- A note on market-neutral portfolio selection

- Betas and the Myth of Market Neutrality

- Conditional Volatility Targeting

- Dynamic Trading with Predictable Returns and Transaction Costs

- A Two-Stage Decision Support System for Sustainability-Aware

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.