6.19 When to Switch Off a Trading System

Traders kill good systems in normal drawdowns and ride dead ones on hope. Write the kill rule before the pain, tie it to the drawdown envelope, and treat it as a dial, not a switch.

Knowing when to kill a system is harder than building one, and most traders are terrible at it in both directions. They switch off a good system in a normal drawdown out of fear, locking in the loss right before the recovery, and they keep a dead system running long past the point its edge vanished, hoping. Both errors come from the same root: deciding in the moment, when fear and hope are loudest, instead of by a rule fixed in advance. "When a Drawdown Means the System Is Broken" gave you the statistical signal; this is the full decision of when to pull the plug and how to avoid pulling it for the wrong reason.

The two ways to get it wrong

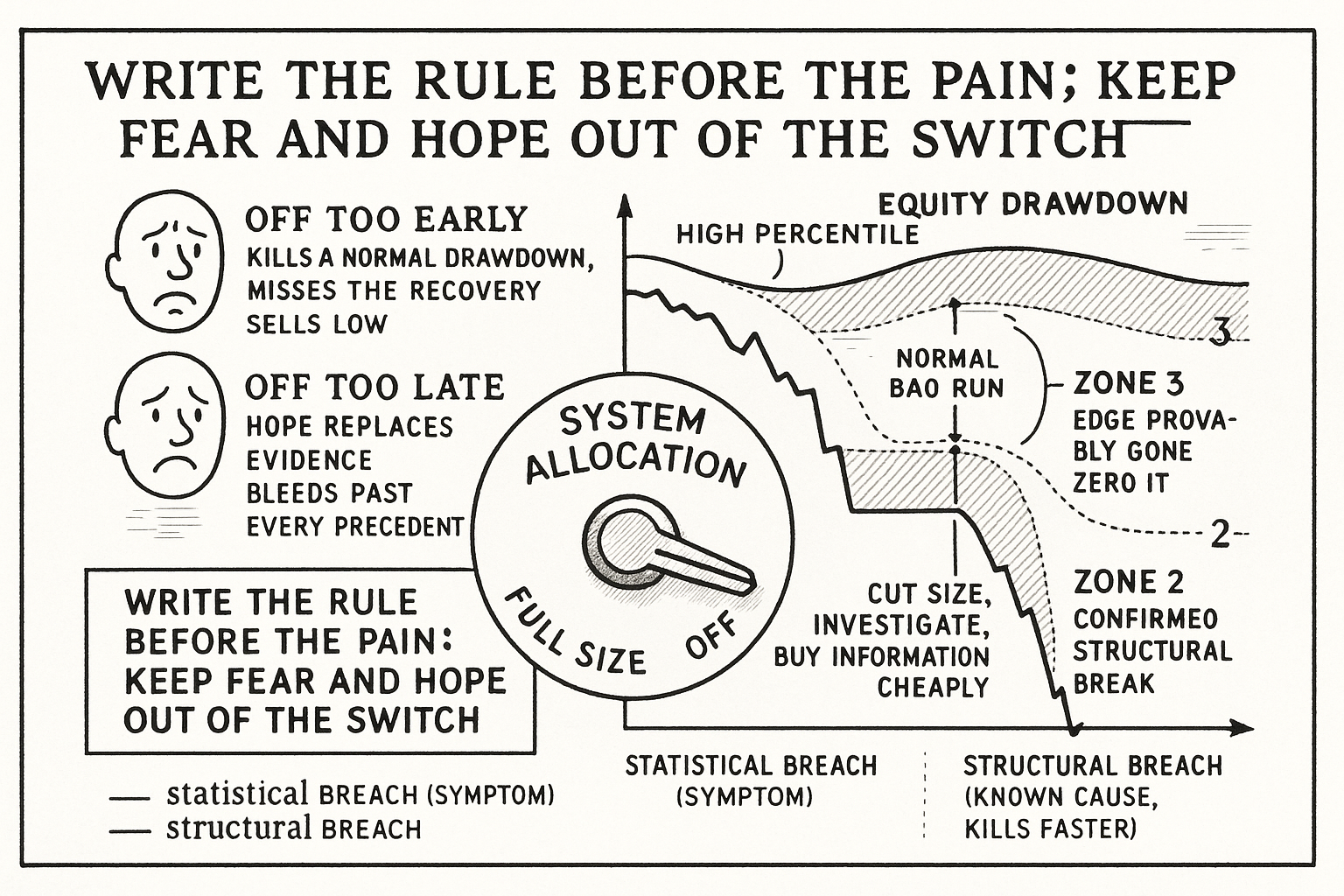

Switching off too early is the more common error and the more expensive one. A system enters a drawdown that sits comfortably inside its historical and Monte Carlo envelope, the trader feels the pain, decides the magic is gone, and turns it off. The drawdown was the cost of doing business, the recovery comes, and the trader either misses it or, worse, switches the system back on at the next peak and catches the next drawdown, doing the exact opposite of what the system needed. This is buying high and selling low applied to your own strategies, and it converts a profitable system into a realized loss through nothing but bad timing of the on-off switch.

Switching off too late is rarer and more lethal. The edge genuinely decayed, the world changed, the inefficiency got arbitraged away, and the trader keeps running the system because admitting it is dead means admitting the research was wasted and the recent losses were not bad luck. Hope substitutes for evidence, the drawdown grinds past every historical precedent, and the account bleeds while the trader waits for a mean reversion that will not come because the mean itself moved. This is "Get-Even-Itis" from the behavioral articles in this pillar, applied to a strategy instead of a trade.

Decide by rule, before the pain

The only defense against both errors is a kill rule written before the drawdown, when you are calm. Tie it to the statistical envelope: keep running while the drawdown stays inside the permutation distribution, investigate and cut risk when it breaches a high percentile of depth or duration, stop when the breach is confirmed and the edge logic no longer holds. Writing it in advance does two things. It stops you from switching off a system that is merely having a statistically normal bad run, because the rule says hold while you are inside the envelope. And it forces you to switch off a system that has objectively broken, because the rule fires whether or not your hope agrees.

The rule should also separate two distinct kill reasons, because they demand different responses. A statistical breach, a drawdown beyond the envelope, says the system's recent behavior no longer matches its history, which might be a dead edge or a rare tail. A structural breach is different and more decisive: the specific market inefficiency the system exploited has provably changed, a rule change, a new participant, a spread that closed, an instrument that stopped trading the way it did. A structural breach kills a system even before the drawdown confirms it, because you know the edge is gone for a reason, not just because the equity fell. Watch for both, and weight the structural reason more heavily, because it is evidence about the cause rather than the symptom.

Switching off is not all-or-nothing

The decision is not a binary switch, and treating it as one drives the panic. The graduated version is to cut size as confidence in the edge falls and restore it as confidence returns, so a breach of the first envelope threshold halves the allocation rather than zeroing it, and a confirmed structural break zeroes it. Sizing down buys you information cheaply: you keep the system live enough to see whether it recovers, while limiting the damage if it does not, which is the right posture under genuine uncertainty about whether an edge is dead or merely dormant. The trader who can only fully on or fully off is forced into a high-stakes guess at the worst moment; the trader who sizes down turns the kill decision into a dial and lets the evidence accumulate. The discipline is the same as the rest of this pillar: pre-commit the rule, act on the statistics, and keep your in-the-moment judgment, the part most corrupted by fear and hope, out of the decision.

Visualizing the kill decision

KEY POINTS

- Knowing when to kill a system is harder than building one. Traders switch off good systems in normal drawdowns out of fear and keep dead systems running out of hope, both from deciding in the moment.

- Switching off too early is common and expensive: a drawdown inside the normal envelope feels fatal, the trader quits, and misses the recovery or re-enters at the next peak, buying high and selling low on their own strategy.

- Switching off too late is rarer and lethal: the edge genuinely decayed but admitting it means admitting wasted research, so hope replaces evidence and the account bleeds past every precedent.

- Defend against both with a kill rule written before the drawdown: hold inside the permutation envelope, cut risk on a high-percentile breach of depth or duration, stop when the breach is confirmed and the edge logic fails.

- Separate a statistical breach (recent behavior no longer matches history, could be a dead edge or a tail) from a structural breach (the exploited inefficiency provably changed). A structural break kills a system even before the drawdown confirms it.

- The decision is a dial, not a switch. Cut size as confidence falls and restore it as confidence returns, so a breach halves the allocation and a confirmed structural break zeroes it, letting evidence accumulate cheaply.

References

- Systematic Trading - Robert Carver (Amazon)

- Trading Systems - Urban Jaekle Emilio Tomasini (Amazon)

- Trade Sizing Techniques for Drawdown and Tail Risk Control

- Measuring Strategy-Decay Risk: Minimum Regime Performance and the Risk of Alpha Decay

- Spurious Predictability in Financial Machine Learning

- Factor Investing and Asset Allocation

- FinEvo: From Isolated Backtests to Ecological Market Games for Adaptive Strategy Evaluation

- A Scalable Behavioral and Social Simulation for Financial Markets

- Hidden Group Time Profiles: Heterogeneous Drawdown Behaviours in Phased Withdrawal Products

- AlphaCrafter: A Full-Stack Multi-Agent Framework for Cross-Sectional Trading

- Volatility Managed Portfolios

- The Impact of Volatility Targeting

- Volatility Scaling in Multi-Asset Portfolios

- Tail Risk Targeting: Target VaR and CVaR Strategies

- Futuretesting Quantitative Strategies

- Sustainable investing and the cross-section of returns and maximum drawdown

- Adaptive Supervised Learning for Volatility Targeting Models

- Agentic Trading: When LLM Agents Meet Financial Markets - arXiv

A note on AI. The ideas, research, analysis, and conclusions in this article are my own. I use AI tools to help with editing and wordsmithing, because English is not my first language, and I am not shy about that. AI-generated ideas and AI-assisted writing are not the same thing: the first is empty slop from a generic prompt, the second is a tool for communicating years of real research more clearly. Judge the work by its substance, not by whether software helped polish the prose.